'Insurance Policy Loans' at the People's Quick Cash Window Increase by 3 Trillion

Delinquency Rate and Non-Performing Loan Ratio Also Rise

Last year, the outstanding balance of household loans from insurance companies increased by nearly 3 trillion won within a year. Most of these were 'insurance policy loans,' which are typically sought when urgent funds are needed. The delinquency rate also nearly doubled, and with ongoing domestic and international economic uncertainties, there are calls to strengthen soundness management.

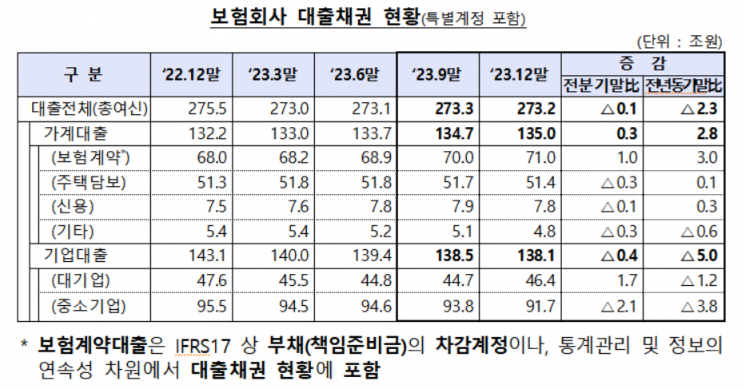

According to the Financial Supervisory Service on the 26th, as of the fourth quarter of last year, the outstanding balance of insurance company loan receivables was 273.2 trillion won, down 2.3 trillion won from the same period the previous year (275.5 trillion won). Since the beginning of this year, it has increased by about 200 billion won.

The issue lies with household loans. The scale of household loans reached 135 trillion won, an increase of 2.8 trillion won compared to the same period last year. Insurance policy loans, regarded as a quick cash source for ordinary people and a recession-type loan, increased by 3 trillion won alone. Insurance policy loans are loan products where borrowers do not cancel their subscribed insurance but borrow 79-95% of the surrender value. There are no screening procedures such as credit rating checks or early repayment fees. Typically, those with low credit scores who find it difficult to use bank loans or have unstable cash flow use these loans. During the same period, mortgage loans (100 billion won) and credit loans (300 billion won) also increased, but other loans (-600 billion won) decreased.

Corporate loans stood at 138.1 trillion won, down 5 trillion won compared to the same period last year. Both large corporations (-1.2 trillion won) and small and medium-sized enterprises (-3.8 trillion won) saw decreases.

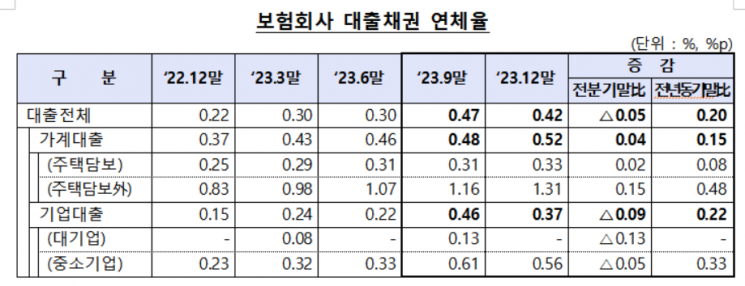

The delinquency rate is also a concern. In the fourth quarter of last year, the delinquency rate for insurance companies was 0.42%, nearly double (an increase of 0.2 percentage points) compared to 0.22% in the same period the previous year. During the same period, the delinquency rate for household loans rose from 0.37% to 0.52%, an increase of 0.15 percentage points. Corporate loans increased from 0.15% to 0.37%, up 0.22 percentage points.

The non-performing loan ratio also surged. In the fourth quarter of last year, the non-performing loan ratio for insurance companies was 0.74%, more than triple (an increase of 0.51 percentage points) compared to 0.23% in the same period the previous year. During the same period, the non-performing loan ratio for household loans rose from 0.29% to 0.37%, and for corporate loans, it increased more than fourfold from 0.2% to 0.91%. Among corporate loans, the non-performing loan ratio for small and medium-sized enterprise loans sharply rose 4.5 times to 1.33% compared to 0.29% in the same period last year.

A Financial Supervisory Service official stated, "We plan to continuously monitor the soundness indicators of insurance company loans, such as delinquency rates," adding, "We will also encourage early normalization of non-performing assets and enhance loss absorption capacity through sufficient provisioning for loan losses."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}