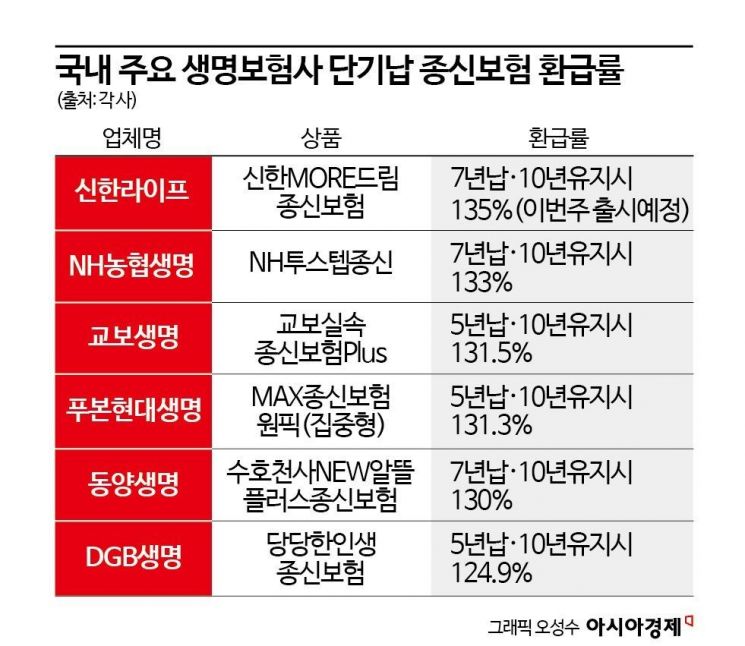

Shinhan Life Launches 135% Refund Rate This Week

Life Insurers' New IFRS17 Tool to Expand CSM Short-Term

Post Office Insurance and Other Mutual Aid Operators Also Eyeing Opportunity

Since the beginning of the year, fierce competition has erupted in the life insurance industry over raising the refund rates of 'short-term payment whole life insurance.' Following the introduction of the new accounting standard (IFRS17), the contract service margin (CSM), a future profitability indicator, has become important, leading to a surge in sales of short-term payment whole life insurance that can quickly boost the CSM.

Shinhan Life plans to increase the 7-year payment and 10-year retention refund rate of its short-term payment whole life insurance product, 'Shinhan MORE Dream Whole Life Insurance,' launched earlier this year, from the current 130% to 135% within this week. This is the highest refund rate level in the industry. Short-term payment whole life insurance reduces the payment period from the conventional 10 to 30 years to 5 to 7 years. A Shinhan Life official explained, "Our goal is to apply the adjusted refund rate starting as early as the 15th."

Shinhan Life's decision to adjust the refund rate about two weeks after launching the new product came after NH Nonghyup Life recently raised the 7-year payment and 10-year retention refund rate of its short-term payment whole life insurance to an industry-high 133%. Kyobo Life also increased its 5-year payment and 10-year retention refund rate to 131.5% earlier this year. Fubon Hyundai Life (131.3%) and Dongyang Life (130%) have also set refund rates above 130% for 5- and 7-year payment whole life insurance with 10-year retention. A 130% refund rate for 5-year payment and 10-year retention means that if the total premiums paid over 5 years amount to 30 million KRW, the policyholder will receive 39 million KRW after maintaining the contract for the next 5 years without paying premiums. From the consumer's perspective, products with even 1% higher refund rates naturally attract more attention.

The competition to raise refund rates for short-term payment whole life insurance began last year. As the competition intensified, the Financial Supervisory Service restricted the refund rates at the 5- and 7-year points to not exceed 100% in September last year. This was to prevent cases where short-term payment whole life insurance, a protection product, might be sold as a savings product due to overheated competition. However, life insurers have circumvented this by adjusting the refund timing from 5 or 7 years to 10 years, selling products with refund rates exceeding 130%.

Insurance agents have become even more aggressive in marketing this year. Many promote these products as useful for 'gifting' and 'financial planning.' In the case of gifting, this method leverages the tax deferral effect. Suppose a parent wants to pass on 100 million KRW to their child without gift tax. The parent gifts 50 million KRW (the gift tax exemption amount) in cash to the child and enrolls the remainder in a short-term payment whole life insurance policy with a 10-year retention period. Since the gift tax exemption resets at the insurance event date (maturity), no gift tax is incurred during this process. Agents also emphasize other benefits such as exemption from interest income tax after 10 years and mileage accumulation from premium payments by card, actively recruiting subscribers. One insurance agent said, "Short-term payment whole life insurance offers high incentives (additional commissions beyond product sales fees), so it is the first product we recommend to customers," adding, "Recently, the silver generation frequently seeks it for gifting purposes."

When life insurers raise refund rates and incentives, company profits inevitably decrease. Nevertheless, they persist with aggressive sales because it allows them to rapidly increase the CSM. The CSM is a key indicator introduced by IFRS17, representing the estimated future profits an insurer expects to earn from insurance contracts. A higher CSM results in better accounting performance and favorable evaluations of the performance of employees during the relevant period.

Even mutual aid providers such as Korea Post Insurance are showing signs of joining the competition to sell short-term payment whole life insurance. The Korea Post Finance Development Institute, a subsidiary of the Korea Post Headquarters overseeing Korea Post Insurance, recently prepared a 'Research Report on the Introduction of Short-Term Payment Whole Life Insurance.' The insurance contracts of the four major mutual aid organizations (Korea Post Insurance, Fisheries Cooperative, Credit Union, and Saemaul Geumgo) are exempt from the Insurance Business Act regulations and financial supervisory oversight that apply to private insurers. This raises concerns that consumers may be more vulnerable to incomplete sales. A Korea Post Finance Development Institute official stated, "The internal report was prepared purely for market research purposes," adding, "There are no concrete plans regarding product launch yet."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}