From 3% Insurance Premium Rate in 1954

Stabilized Through 50 Years of Continuous Increases

Japanese pension experts have suggested raising the pension eligibility age for the success of pension reform in Korea. While an increase in insurance premiums is inevitable to prevent the depletion of pension funds, it is difficult to reach a national consensus, so the idea is to delay the age at which pensions are received.

According to the “Overseas Business Trip Report for Research on Trends in Japan’s Pension System Reform and Legislation” by the Ministry of Government Legislation on the 5th, last November, the Ministry visited Japan’s Ministry of Health, Labour and Welfare, the Pension Bureau, and Keio University. This was to understand the trends in Japan’s pension system reform, which succeeded in promoting public pension system reforms while facing serious low birthrates and aging issues earlier than Korea. The Ministry of Government Legislation believed that this could provide insights during the legislative process if pension reforms are undertaken in the future.

"Cooperation on Raising Insurance Premium Rates Is Difficult... Pension Eligibility Age Should Be Raised First"

Kohei Komamura, a professor in the Faculty of Economics at Keio University, stated, “To secure pension financial stability, methods such as raising insurance premium rates, increasing the pension eligibility age, or reducing insurance benefits can be considered,” but emphasized, “Since national cooperation on raising insurance premiums is difficult and the political sphere is not proactive, the only option is to first raise the pension eligibility age.”

In Japan’s case, political consensus was achieved during the reform process to secure pension finances. The Social Democratic Party, realizing the pension finances were quite vulnerable, supported raising the pension eligibility age when it came to power. This stance was maintained even after the government changed.

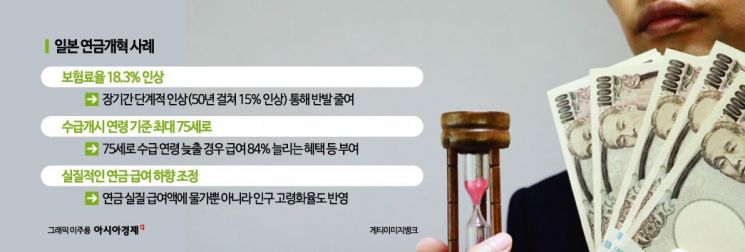

Currently, Japan’s pension finances are evaluated as stable. This is thanks to the continuous, gradual increase in insurance premium rates regardless of changes in economic conditions. Through the 2004 pension reform, Japan succeeded in gradually raising the insurance premium rate to 18.3% by 2017. Although Japan faced domestic opposition, since the insurance premium rate started at 3% in 1954 and increased by about 15% over roughly 50 years, it was able to steadily raise the rate even during poor economic years.

Japan’s Pension Finances Secured Stability... Insurance Premium Rate at 18.3%, Eligibility Age Up to 75

Japan also succeeded in implementing a reform plan to delay the pension eligibility age up to a maximum of 75. In 2019, the Japanese government set the pension eligibility age at 65 but allowed recipients to voluntarily start receiving pensions between ages 60 and 75. Starting at 60 reduces benefits by 24%, while delaying to 75 increases them by 84%. The retirement age was mandated at 65, creating an environment where citizens could postpone pension receipt.

The actual benefit level was also lowered. Typically, pension amounts are calculated linked to inflation to maintain real value. When inflation rises significantly, pension amounts also increase, accelerating fund depletion. Japan introduced the “pension slide” system in 2004, which deducts the increase in population aging rate. If inflation rises by 2% but the aging rate also increases, the pension increase rate slows down. At the same time, to guarantee minimum income, the income replacement rate floor was set at 50%.

The Ministry of Government Legislation analyzed, “A sharp increase in insurance premium rates is realistically difficult,” and added, “Extending the retirement age or reemployment after retirement to increase the number of pension contributors and extending the pension eligibility age can also be means to secure finances.” Currently, Korea’s pension eligibility age is 63 but is scheduled to rise to 65 by 2033. However, a Ministry official noted, “We wanted to understand related trends because Japan has already dealt with low birthrates and aging, so the level of concern is similar,” but added, “It should be kept in mind that the situations in Japan and Korea are not exactly the same.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}