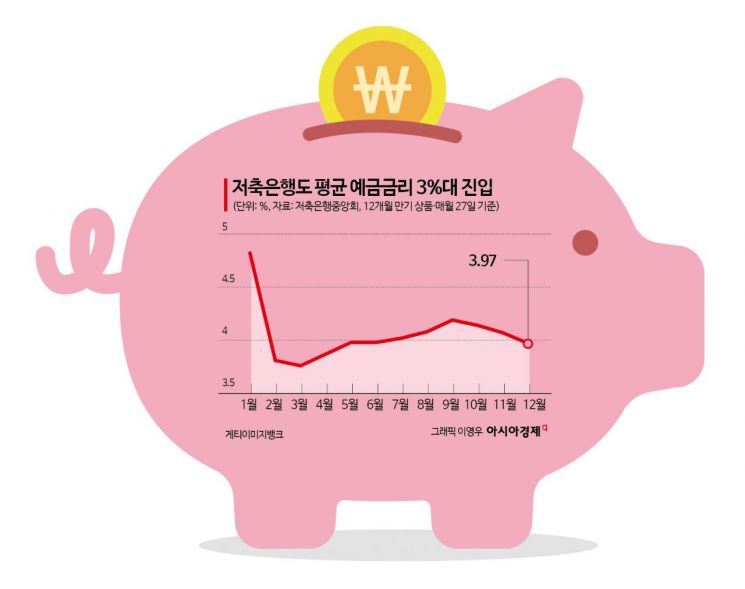

12-Month Maturity Average Interest Rate 3.97%

Gap with Commercial Banks at '3.5~3.9%' Narrowing

"Sufficient Surplus Funds, Less Effort to Attract New Deposits"

Interest Expenses Increased by Special Promotion Product Sales ↓

The average interest rate on savings banks' fixed deposits recorded in the 3% range. As high-interest products matured at the end of this year, savings banks, which competed to increase deposit rates and re-deposit funds, are analyzed to have no incentive to raise rates as they have secured sufficient funds.

According to the Savings Banks Association Consumer Portal product disclosure as of the 28th, the nationwide average interest rates for savings banks' fixed deposits as of the previous day were 3.41% for 6 months, 3.97% for 12 months, 3.33% for 24 months, and 3.29% for 36 months, all in the 3% range. Major savings banks such as SBI Savings Bank (3.9%), which is the industry leader, OK (3.51%), Pepper (3.4%), and Korea Investment (3.9%) offer 'fixed deposit' interest rates in the 3% range. As of this day, the highest interest rate (based on 12-month maturity) is 4.3%, offered by eight savings banks including Sangsangin.

The average interest rate for 12-month maturity products has been steadily declining. This figure dropped about 1 percentage point from 4.82% as of January 27 this year. The rate was in the high 3% range until June. From July to last month, it was in the 4% range but dropped back to the 3% range on this day.

The interest rate gap with commercial banks has also narrowed. As of this day, the 12-month fixed deposit interest rates of the five major commercial banks (KB Kookmin, Shinhan, Hana, Woori, NH Nonghyup) range from 3.5% to 3.9% annually. NH Nonghyup Bank's 'NH Hometown Love Donation Deposit' offers a top rate of 3.9%, which is 0.07% lower than the average savings bank rate (3.97%). Savings banks often offer interest rates about 0.8 to 1 percentage point higher than commercial banks. If the interest rate difference is small, consumers are more likely to entrust their money to stable and large commercial banks.

The reason savings banks are rushing to lower deposit interest rates is that they have sufficient surplus funds. As the maturity of high-interest special products attracted at the end of last year approaches, savings banks competed to attract customers. This was a measure to secure liquidity such as cash. However, after passing the first half of the year, savings banks that have secured sufficient funds are lowering rates again and reducing new deposit attraction. According to the Bank of Korea Economic Statistics System, the interest rate on savings banks' fixed deposits (1-year maturity) rose from 3.62% in March this year to 4.31% in October. However, it showed a downward trend again to 4.19% last month. Accordingly, the deposit balance of savings banks also continuously increased from the lowest 114.526 trillion won (May) this year to 117.8504 trillion won in September. After that, it slightly decreased to 115.2311 trillion won in October.

An official from a savings bank said, "We have enough funds to the extent that there is no risk related to surplus funds until January next year, so we are lowering interest rates because there is no particular intention to attract new deposits."

The rapid increase in interest expenses due to the sale of high-interest special products attracted last year is also cited as a reason for savings banks lowering interest rates. They intend to reduce interest expenses by lowering deposit interest rates. From January to September this year, the interest expenses paid by savings banks amounted to 4.048 trillion won, which is 2.1 times the 1.9674 trillion won for the same period last year.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}