As high interest rates persist, causing a rapid cooling of the housing market, the nationwide housing business outlook has further deteriorated, particularly in the Seoul metropolitan area and major cities.

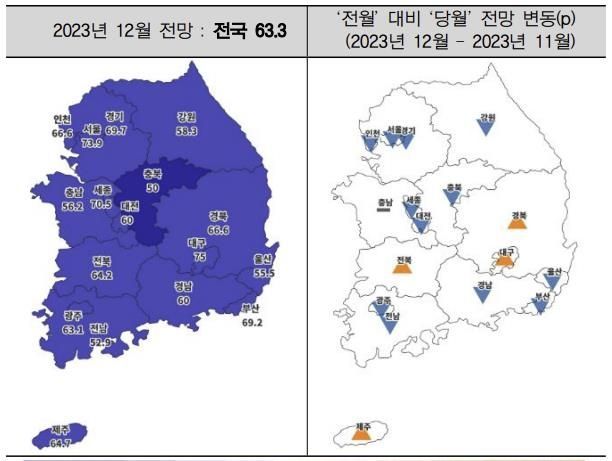

The Korea Housing Institute (hereinafter KHI) announced on the 14th that the nationwide housing business outlook index for December recorded 63.3, down 5.5 points from the previous month. This index is calculated based on a survey of members of the Korea Housing Association and the Korea Housing Builders Association, and a value above the baseline of 100 indicates that a higher proportion of companies expect the market to improve.

The index, which had slightly risen in October, plunged 18.9 points last month to 68.8, falling into the 60s for the first time in nine months since February this year.

By region, the Seoul metropolitan area dropped 13.4 points from 83.5 last month to 70.1 this month. Incheon saw the largest decline, falling 16.7 points from 83.3 to 66.6, while Seoul (86.3→73.9) and Gyeonggi (81.0→69.7) also fell by more than 10 points each.

The Seoul metropolitan area index showed an upward trend from January to August this year but entered a downward phase thereafter, falling below the baseline since last month.

Non-metropolitan areas declined by 3.7 points from 65.6 last month to 61.9 this month, remaining in the 60s for the second consecutive month. Among the major cities, all except Daegu, which rose from 72.7 to 75, recorded declines. Notably, Gwangju dropped 21.1 points from 84.2 to 63.1, marking the largest decrease nationwide, followed by Daejeon (71.4→60.0), Busan (70.8→69.2), and Ulsan (56.2→55.5). Sejong (81.2→70.5) also experienced a steep decline.

The indices for local regions excluding major cities showed varied patterns. Chungbuk fell from 69.2 to 50.0, recording the lowest index nationwide and the largest decline among other local areas this month. Since dropping below the baseline in July this year, Chungbuk has steadily declined, hitting a yearly low this month. Gangwon (66.6→58.3), Gyeongnam (66.6→60.0), and Jeonnam (56.2→52.9) also showed downward trends.

Regions where the index rose included Jeonbuk (50.0→64.2), Jeju (52.9→64.7), and Gyeongbuk (64.7→66.6), while Chungnam remained steady at 56.2 for both last month and this month. These areas appear to reflect expectations for a housing market recovery due to supply shortages, as housing supply had previously decreased.

KHI explained, "The rapid rise in interest rates over recent months has quickly cooled the housing market, and the overlapping negative factors in project financing (PF) have led to a pessimistic outlook among housing developers." It added, "If the upward trend in interest rates eases and PF financing issues are somewhat resolved, negative perceptions are expected to improve."

Meanwhile, the material supply index rose from 82.4 last month to 91.9 this month, and the financing index also increased from 65.5 to 71.6. The rise in these indices is interpreted as influenced by the drop in oil prices, some improvement in supply chain issues, and a 57.4% decrease in this year’s construction starts compared to last year, which reduced demand.

KHI noted, "Although the financing index has been rising since November (37.3), it has not surpassed the baseline and remains in a sideways range. The increase this month is attributed to responses indicating that, despite overall financing difficulties, funding challenges are gradually easing for large construction companies with high credit ratings."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}