It Should Expand as Group Insurance Like Traveler's Insurance

Domestic cybercrime, especially financial crimes targeting individuals, continues to increase, but the subscription rate for related insurance remains low. There are calls for activating cyber risk coverage plans for individuals by utilizing group insurance and other methods.

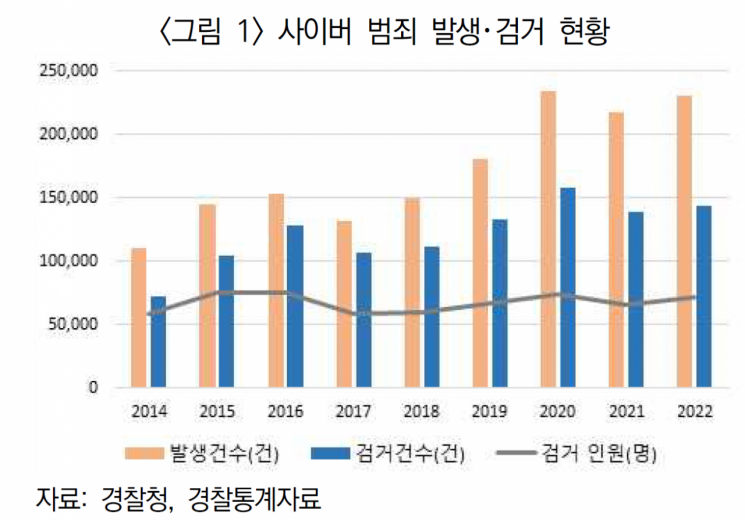

On the 10th, the Korea Insurance Research Institute released a report titled "Exposure of Individuals to Cybercrime and Measures to Expand Coverage" containing these findings. According to the report, domestic cybercrime is steadily increasing. Based on statistics from the National Police Agency, there were about 110,000 cases in 2014, but this number more than doubled to approximately 230,000 cases in 2022 over eight years. Especially at the beginning of the COVID-19 pandemic, as non-face-to-face activities increased, cybercrime reached about 234,000 cases in 2020, an increase of approximately 54,000 cases compared to the previous year. In 2021, the number slightly decreased to about 218,000 cases but exceeded 220,000 cases again the following year.

In particular, crimes targeting individuals rather than companies have been continuously increasing, spreading the damage. Cyber fraud (67.6%), cyber defamation and insult (12.7%), and cyber financial crimes (12.4%), which constitute the largest portions of cybercrime, mostly target individuals. According to the Korea Information and Communication Security Ethics Association, the estimated scale of domestic cyber damage is 695.6 billion KRW for companies and 983.4 billion KRW for individuals.

Although the scale of individual damage is larger, individuals do not subscribe to related insurance, resulting in inadequate risk management. Currently, insurance companies selling personal cyber insurance are identified as about five companies offering standalone products and five companies offering optional riders. Most products or riders include coverage for internet shopping mall and direct transaction fraud, as well as cyber financial fraud (such as voice phishing). Some insurers also compensate for liability due to cyber defamation and copyright infringement, legal insurance, or damages from personal information leaks.

However, sales performance of standalone products is very minimal, ranging from several hundred to a few thousand cases annually. Coverage limits per guarantee are mostly between 1 million and 5 million KRW, excluding deductibles of 10-30%. Kim Gyudong, a research fellow at the Korea Insurance Research Institute, explained, "Individuals do not have a high awareness of cyber risks and therefore do not feel the need to subscribe to insurance, and insurance companies are not actively promoting or selling due to profitability concerns."

Therefore, there are calls to activate the market through insurance recruitment centered on some form of group contracts. It is suggested to emulate methods such as travel agencies enrolling group customers in travel insurance or offering accident insurance at a discount to customers purchasing ski season passes. In other words, the report emphasizes that companies providing online transactions or financial services should subscribe to insurance in the form of group insurance or promote insurance products.

Research fellow Kim said, "Cyber fraud and financial crimes mostly occur in relation to used goods trading sites, shopping malls, telecommunications companies, and financial services, so these entities should take the lead in consumer damage relief," adding, "From the insurer's perspective, it would be advantageous as it can reduce costs compared to individual contracts and make management easier."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}