Ministry of Economy and Finance Announces Legislative Notice on 'Liquor Tax Act Enforcement Decree' Amendment

Tax Burden Expected to Decrease According to Standard Sales Ratio

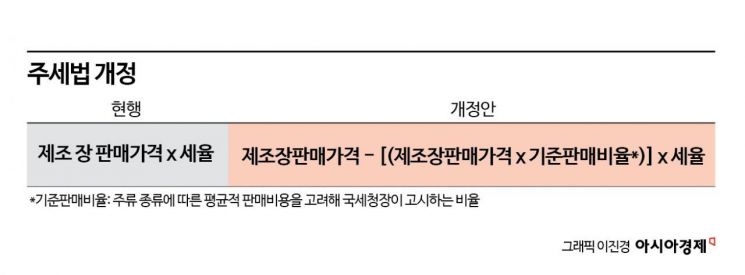

From January next year, a 'standard sales ratio' will be applied when taxing domestically produced distilled liquors such as soju and whiskey. The purpose is to lower the taxes on domestic distilled liquors and stabilize prices.

On the 1st, the Ministry of Economy and Finance announced the legislative notice for the amendment of the Enforcement Decree and Enforcement Rules of the Liquor Tax Act containing this content. The main point is to introduce the standard sales ratio as the tax base for domestic distilled liquors like soju, thereby reducing the tax burden on companies.

The standard sales ratio is the ratio applied when determining the tax base (the amount on which tax is levied). Since the tax base is set as the remaining amount after subtracting the amount corresponding to the standard sales ratio from the shipment price, the degree of price reduction depends on the set standard sales ratio. The government plans to analyze the proportion of domestic distribution-related selling and administrative expenses by considering the cost and distribution structure of each type of domestically produced liquor, and decide the ratio through deliberation by the Standard Sales Ratio Deliberation Committee established at the National Tax Service based on this analysis.

The Ministry of Economy and Finance explained that this is intended to enhance tax fairness in a situation where domestically produced liquors have had a relatively higher tax burden compared to imported liquors. Currently, domestically produced liquors subject to the specific tax and imported liquors are taxed at different points in time, resulting in a relatively higher tax burden on domestic liquors and concerns about reverse discrimination. At present, for domestically produced liquors, the manufacturer's selling and administrative expenses are included in the tax base and taxed accordingly. In contrast, imported liquors are taxed upon domestic import customs clearance, so the importer's selling and administrative expenses are not included in the tax base.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}