The apartment pre-sale outlook index has been declining for three consecutive months. Recently, due to the impact of high interest rates, apartment sales volume has decreased and the price increase rate has slowed, leading to a diminished expectation for the pre-sale market.

According to the Korea Research Institute for Human Settlements (KRHIS) on the 7th, the apartment pre-sale outlook index for November was recorded at 70.4, down 13.4 points from the previous month. This marks the third consecutive month of decline since September.

The apartment pre-sale outlook index is a comprehensive indicator from the supplier's perspective, assessing the conditions of complexes that are about to be pre-sold or are currently being pre-sold. A value above 100 means that more member companies view the market outlook positively, while a value below 100 indicates the opposite.

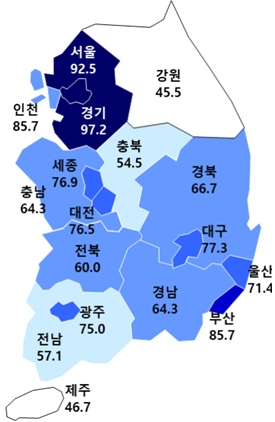

By region, Seoul dropped 7.5 points from the baseline of 100.0 last month to 92.5 this month. Incheon (103.6→85.7) and Gyeonggi (102.6→97.2) also fell below the baseline, resulting in the metropolitan area’s average index declining by 10.2 points to 91.8.

A KRHIS official explained, "Recently, apartment sales volume in the metropolitan area has decreased and the price increase rate has slowed, causing even the expectations for the metropolitan pre-sale market to waver."

In provincial metropolitan cities, the index dropped 18.8 points from 95.9 last month to 77.1 this month. Daegu experienced a particularly large drop of 30.1 points, falling from 107.4 to 77.3. Other cities such as Gwangju (90.0→75.0), Daejeon (89.5→76.5), Busan (96.3→85.7), and Ulsan (80.0→71.4) also declined.

Additionally, regions such as Sejong (112.5→76.9), Jeonnam (81.3→57.1), and Gangwon (66.7→45.5) showed consecutive weaknesses, with the nationwide indices showing a downward trend except for Chungnam (56.3→64.3).

A KRHIS official stated, "Due to the rapid rise in interest rates and increased market volatility, along with heightened sensitivity of buyers to apartment prices, the burden on housing developers has expanded, making pre-sale projects difficult to maintain for the time being." They added, "This year, permits, groundbreaking, and pre-sale volumes have all shown a declining trend, so close monitoring of the apartment pre-sale market is necessary for smooth future supply and demand adjustment."

The November pre-sale price outlook index recorded 106.7, down 1.9 points from the previous month, but it has consistently remained above the baseline since May.

KRHIS forecasted, "Due to the large-scale deregulation of regulated areas following the easing of real estate policies at the beginning of the year and the increase in basic construction costs, the upward trend in pre-sale prices is expected to continue for the time being."

The pre-sale volume outlook index was 96.6, down 0.5 points from the previous month. The unsold inventory outlook index rose 11.0 points to 96.7 but has remained below the baseline since May.

KRHIS pointed out, "This month, there are no planned pre-sale volumes in Daegu, Sejong, Gyeongnam, Jeonnam, and Jeju, and most of the pre-sale volumes are concentrated in the metropolitan area, showing a polarization phenomenon." They added, "Although unsold inventory is decreasing, post-completion unsold inventory has slightly increased, and the accumulation of unsold inventory in provincial areas continues, so it is necessary to monitor the regional distribution and supply trends of unsold inventory."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}