Life insurers also turn to profit

Ratio of insurance payouts to premiums down 12%p

Linked to over-treatment prevention and premium hikes

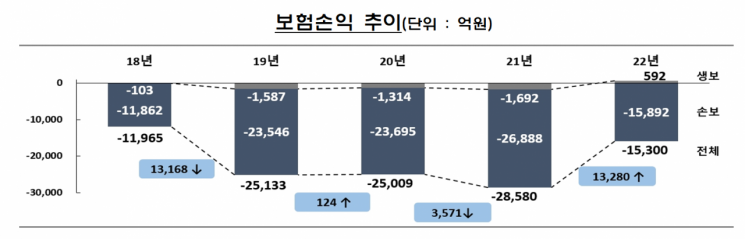

Last year, insurance companies recorded a deficit of around 1.5 trillion KRW in indemnity medical insurance. The deficit narrowed by more than 1.3 trillion KRW compared to the previous year, and the loss ratio gradually decreased, showing signs of improvement. This is attributed to the operation of institutional measures to prevent excessive medical treatment, coupled with premium increases.

Deficit Halved... Loss Ratio Also Declines

According to the '2022 Indemnity Medical Insurance Business Performance (provisional, based on 16 companies, excluding group indemnity)' announced by the Financial Supervisory Service on the 18th, indemnity insurance posted a loss of 1.53 trillion KRW last year. This is nearly half the deficit of 2.858 trillion KRW recorded the previous year. Specifically, life insurance companies turned from a deficit of 169.2 billion KRW in 2021 to a surplus of 59.2 billion KRW last year. Non-life insurance companies recorded a deficit of 1.5892 trillion KRW last year, reducing their deficit by about 1.1004 trillion KRW compared to the previous year.

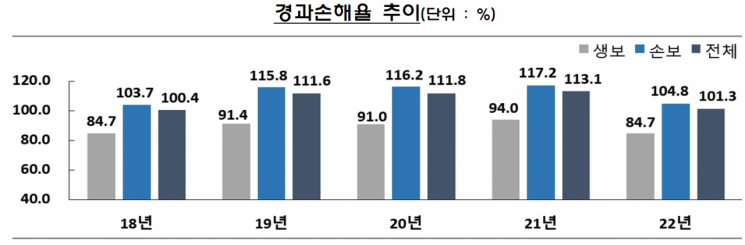

The loss ratio, which is the ratio of claims paid to premiums received, also improved. Last year, it was 101.3%, down 11.8 percentage points from the previous year. For life insurers, the loss ratio was 84.7% last year, a decrease of 9.3 percentage points from the previous year. Non-life insurers also saw a double-digit decline from 117.2% in 2021 to 104.8% last year.

By product generation, the 3rd generation had the highest loss ratio at 118.7%, followed by the 1st generation (113.2%), 2nd generation (93.2%), and 4th generation (91.5%). Unlike the 1st and 2nd generations, whose premiums have been continuously increased, the 3rd generation indemnity products had not adjusted premiums for five years since launch, resulting in a higher loss ratio. Indemnity insurance is classified by sales period and coverage structure into 1st generation (old indemnity), 2nd generation (standardized indemnity), 3rd generation (new indemnity), and 4th generation and others (elderly, pre-existing conditions). Additionally, the expense ratio, which represents business expenses relative to premium income, was 10.3%, down 1.1 percentage points from the previous year.

Meanwhile, the number of policies in force steadily increased to 35.65 million as of the end of last year, up 0.4% (150,000 policies) from the previous year. Premium income, which is equivalent to sales, rose by 13.3% (1.5438 trillion KRW) to 13.1885 trillion KRW.

Combined Effect of Excessive Treatment Prevention and Premium Increases

The improvement in performance is attributed to efforts to prevent excessive non-reimbursed medical treatments combined with premium increases. Earlier, the Financial Supervisory Service, together with the National Police Agency and the Korean Ophthalmological Society, announced a 'Special Measure to Prevent Excessive Cataract Treatment and Insurance Leakage' in April last year and revised the 'Insurance Fraud Prevention Model Regulations' the following month. A Supreme Court ruling that insurance payments should be made within outpatient medical expense limits (typically around 250,000 KRW per visit) when inpatient treatment is unnecessary also contributed to reducing excessive treatments.

The increase in the proportion of 4th generation indemnity insurance, which has higher deductibles but lower premiums and includes mechanisms to control excessive treatment, was also a significant factor. The share of 4th generation indemnity insurance rose to 5.8% at the end of last year, up 4.3 percentage points from the previous year. Additionally, the accumulated premium increases for 1st and 2nd generation indemnity insurance also helped improve performance.

A Financial Supervisory Service official emphasized, "We will rationally improve indemnity insurance compensation standards for major non-reimbursed treatment items with concerns about excessive treatment, such as physical therapy, and extend premium discount periods to promote the transition to 4th generation indemnity insurance. We will also firmly establish the individual and group indemnity suspension system and closely monitor insurance claims to minimize factors that cause premium increases, such as insurance leakage."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}