Loss ratios and costs decrease while subscribers increase

Big 4 oligopoly deepens... Carrot and other non-face-to-face specialists also rise↑

Last year, the performance of automobile insurance by non-life insurance companies improved compared to the previous year. Operating profit increased by more than 20%. This is attributed to an increase in the number of insurance policies, a decrease in the loss ratio?which is the ratio of claims paid to premiums received?and reduced costs due to the expansion of non-face-to-face sales.

According to the '2022 Automobile Insurance Business Performance (Preliminary)' announced by the Financial Supervisory Service on the 3rd, last year's automobile insurance sales (gross premiums written, based on 12 non-life insurance companies) amounted to 20.7674 trillion KRW. This represents a 2.4% (490 billion KRW) increase compared to the previous year. This is believed to be due to the increase of 570,000 in the number of insured vehicles, reaching 24.8 million.

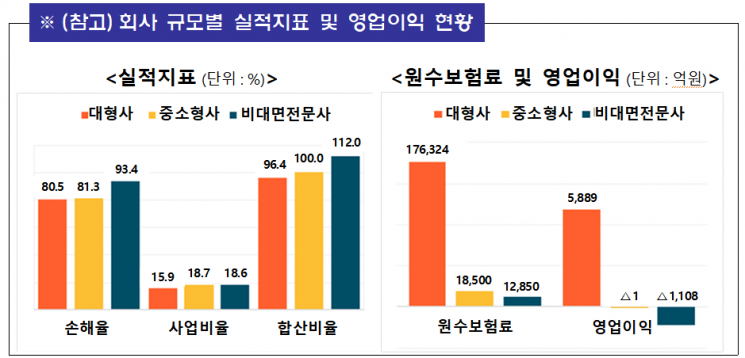

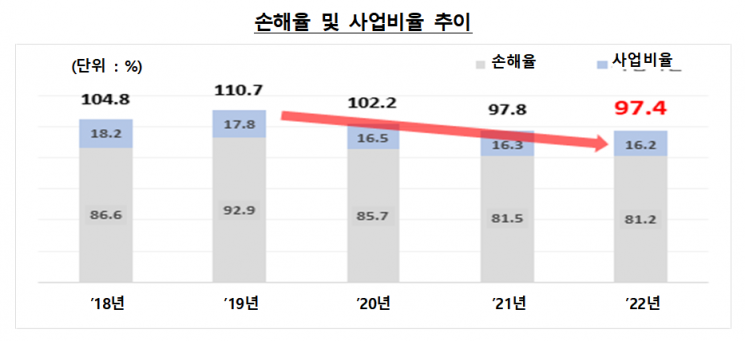

The operating profit was even more robust. It recorded 478 billion KRW, an increase of 20.1% (79.9 billion KRW) compared to the previous year. The loss ratio fell by 0.3 percentage points from 81.2%, which was at its peak in 2021 due to COVID-19 when outdoor activities were restricted. Although the number of insured vehicles increased, leading to higher premium income, the loss ratio improved as it dropped by 2.0 percentage points to 15.0%.

Cost-saving effects also played a role. The proportion of non-face-to-face CM channels, which have relatively lower selling expenses, increased, causing the expense ratio to decrease from 18.2% in 2018 to 16.2% last year. Since CM channels do not pay sales commissions to agents, they typically incur about 17% less cost compared to face-to-face channels. The CM channel's share surpassed 30% for the first time, reaching 31.6% last year. Consequently, the combined ratio, which considers both the loss ratio and expense ratio, was recorded at 97.4%, a 0.4 percentage point decrease from the previous year.

Meanwhile, the oligopoly structure intensified as the market share of large companies expanded further. According to the Financial Supervisory Service, last year, the market share of large companies such as Samsung Fire & Marine Insurance, Hyundai Marine & Fire Insurance, KB Insurance, and DB Insurance in the automobile insurance market was 84.9%, up 0.2 percentage points from the previous year.

On the other hand, the market share of small and medium-sized companies such as Meritz Fire & Marine Insurance, Hanwha General Insurance, Lotte Insurance, MG Insurance, and Heungkuk Fire & Marine Insurance fell by 0.5 percentage points to 8.9%. However, the market share of non-face-to-face specialized companies, including Carrot Insurance, Hana Insurance, and AXA Insurance?which mainly generate sales through TM and CM channels?increased by 0.3 percentage points to 6.2% during the same period.

A Financial Supervisory Service official stated, "Since institutional improvements to prevent excessive treatment of outpatients will be implemented from this year, we will closely analyze the effects and market conditions such as insurers' monthly loss ratios. If loss ratios are managed stably, we will promote institutional improvements such as premium adjustments that reflect performance, rationalization of compensation standards, and development of insurance products for vulnerable groups."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}