3-Year Korean Treasury Bonds Fall to Low 3% Range

Fed Unlikely to Maintain High-Intensity Tightening Due to SVB Crisis

Investment Sentiment Expected to Weaken for Non-Investment Grade Credit

As Treasury bond yields, which had surged sharply earlier this month due to concerns over tightening, have turned downward, analysis suggests that bond market volatility will increase until the March Federal Open Market Committee (FOMC) meeting. Amid persistent inflation worries, the collapse of the U.S. Silicon Valley Bank (SVB) and concerns over the financial soundness of global investment bank Credit Suisse (CS) have complicated the calculations of Jerome Powell, Chair of the U.S. Federal Reserve (Fed), who had expressed a commitment to raising interest rates. The market already expects a lower terminal rate and does not anticipate a sharp rate hike at the March FOMC.

3-Year Treasury Yield Plummets from 3.8% to 3.4%

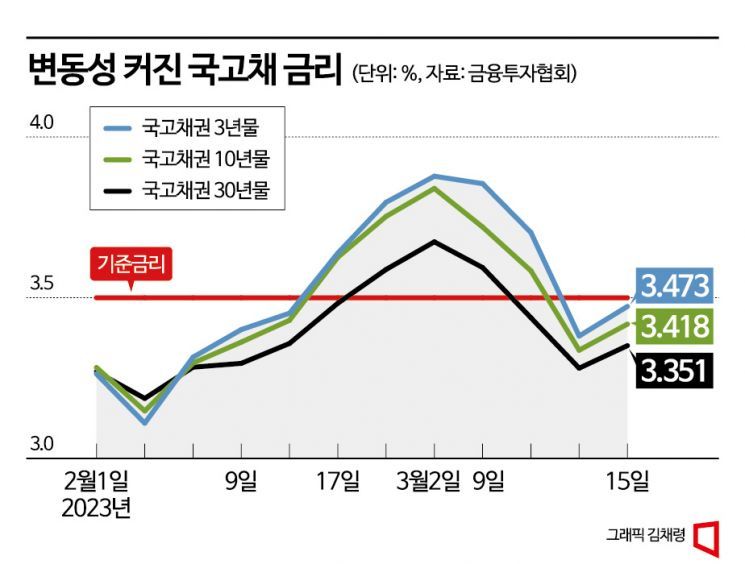

According to the bond industry on the 16th, the 3-year Treasury yield closed at 3.473% the previous day. The 3-year Treasury yield had been moving between 3.7% and 3.8% until the 10th of this month, a level higher than last month's low of 3.1%. This reflected concerns that the Bank of Korea's interest rate direction might change amid expectations that the Fed would resume aggressive rate hikes. However, on the 13th, the 3-year Treasury yield dropped to the 3.4% range. The 10-year and 30-year Treasury yields also fell by 43 basis points (bp) and 32 bp respectively from this month's peak, closing at 3.41% and 3.35% on that day.

The bond market sentiment sharply reversed following the SVB collapse. Starting with SVB's failure, concerns grew over a domino effect of liquidity-strapped regional banks collapsing. Subsequently, worries about Credit Suisse's financial soundness emerged. As a result, the Fed's plans to tighten monetary policy are expected to be restrained. Earlier this month, a 50 bp rate hike at the March FOMC was considered certain, but now a 25 bp increase is the prevailing forecast, with the possibility of a rate hold also being raised. The terminal rate implied by U.S. futures contracts has dropped from the previous 5.75% to 5% (reflecting a 25 bp hike in March).

The Bank of Korea's base rate direction also appears to be solidifying toward a 'hold for the year.' Initially, due to the Fed's tightening, the terminal rate was expected to rise 25 bp above the current 3.5%, but the SVB incident and other factors have led to the judgment that further rate hikes will be difficult. Kim Ji-man, a researcher at Samsung Securities, predicted, "The unexpected SVB incident has heightened financial instability concerns, lowering the Fed's terminal rate level, so the base rate will be held steady for the year."

Experts say that while concerns over rate hikes have eased, the SVB incident is unlikely to trigger a systemic crisis in the U.S. financial market. This is because the U.S. government took unprecedented initial measures by deciding to fully protect all deposits at the failed SVB. The Swiss National Bank also stated that it would provide liquidity if necessary should Credit Suisse's financial soundness issues worsen.

Bond Market Volatility Expected to Increase Due to SVB Incident and Others

However, considering past bank failures, another crisis could emerge, so bond market volatility is expected to remain high for the time being. Samsung Securities, taking this situation into account, forecasts that the 3-year Treasury yield band will move between 3.1% and 3.65%, and the 10-year Treasury yield between 3.15% and 3.6%.

Bond experts recommend a strategy of staggered purchases of long-term bonds whenever Treasury yields rise amid increased market volatility. Given that the SVB and other bank failures have led to expectations of a rate cut within the year, it is judged that yields are unlikely to rise again to near the 4% level. Although it will be difficult to enjoy the rate benefits seen in October-November last year (early 4% range), short-term investors aiming for capital gains are expected to increase. In fact, products investing in long-term bonds have shown higher returns compared to equity products. For example, the ‘KBSTAR KIS Treasury Bond 30-Year Enhanced ETF,’ which has a duration (principal recovery period) of 25 years, recorded a return of 8.9% since the beginning of the year, outperforming the KOSPI (6.9%) over the same period.

Regarding credit bonds, there is a possibility that investor sentiment may weaken due to rising concerns over corporate bankruptcies. Experts also recommend a conservative approach. Although there has been a shift in investor sentiment this year from high-grade AA-rated bonds to lower-rated A-grade non-investment grade bonds, this trend is not expected to continue for the time being. The credit spread, which reflects institutional investors' sentiment toward corporate bonds, hovered around 60 bp at the end of last month but rose to 72 bp recently. Kim Sang-man, a researcher at Hana Securities, said, "It is clear that the SVB incident has increased the risk premium from a credit risk perspective. The direction of credit spreads is open upward, so caution at this point is not a bad idea."

However, there is also analysis that preference for high-quality credit bonds will persist. Kim Ki-myeong, a researcher at Korea Investment & Securities, explained, "During the liquidity crunch triggered by Legoland, credit spreads for high-quality credit bonds quickly narrowed thanks to the government's active response. After the Treasury bond strength trend, high-quality credit bonds will attract attention."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}