National Assembly Legislative Research Office Report

Hong Kong, Singapore 5%P... Korea at 2%P Range

"Stronger Policy Intervention Makes Borrowing More Difficult"

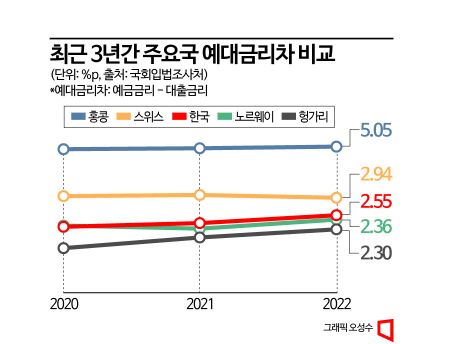

An analysis from the National Assembly Research Service has found that the interest rate spread between deposits and loans at South Korean banks is not significantly larger compared to other countries. According to the report titled 'Policy Trends and Issues for Rational Interest Rate Setting' released on the 13th, although the interest rate spread?the difference between deposit and loan interest rates?has been increasing over the past three years, it was not at a notably high level. From 2020 to 2022, South Korea's spread was 2.05 percentage points → 2.21 percentage points → 2.55 percentage points.

In comparison, Hong Kong's spread (4.94 percentage points → 4.98 percentage points → 5.05 percentage points) was much higher than South Korea's. Singapore also showed a spread exceeding 5 percentage points (5.07 percentage points → 5.13 percentage points → data pending). Switzerland (3.01 percentage points → 3.06 percentage points → 2.94 percentage points) also surpassed South Korea's interest rate spread level.

Financial authorities are currently engaged in policy discussions to ensure interest rates are set rationally amid the increased burden on financial consumers due to recent rate hikes. The mortgage loan interest rate, which has the greatest impact on household interest burdens, rose from 2.50% in 2020 to 4.24% in 2022, leading to a significant increase in banks' interest income. To curb this, authorities are pressuring banks to lower their rates.

They have announced plans to introduce additional comparative disclosures based on balance for interest rate spreads by bank, comparative disclosures for jeonse loan interest rates, and explanatory sections on factors influencing interest rate changes by bank. Since last week, Lee Bok-hyun, Governor of the Financial Supervisory Service, has been 'touring' commercial banks to encourage interest rate reductions. In the National Assembly, a ‘Banking Act Amendment’ has even been proposed that would require disclosure of loan interest rates separated into base rates and additional rates, as well as banks’ target profit margins.

The National Assembly Research Service report stated, "It is necessary to examine the economic impact of policy interventions in the interest rate setting system on the loan market," adding, "If policy interventions become stronger and act as a kind of cap on loan interest rates for banks, banks’ incentives to lend may decrease, making it harder to obtain loans than before, or leading to lending practices focused on high-credit borrowers due to banks’ risk-avoidance tendencies."

It also noted, "The operating costs, risk premiums, and target profit margins reflected in the calculation of loan additional interest rates are internal management matters of banks, and if the government controls these aspects, criticism may arise that it infringes on banks’ management autonomy."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}