Revolving Balance Hits Record High in December Last Year

Cash Service Balance Also Rising Since COVID-19

'Balloon Effect' Due to Card Loan Regulations

[Asia Economy Reporter Minwoo Lee] The amount of 'revolving' credit card payments, where only a portion of the credit card bill is paid and the remainder is carried over, has reached an all-time high. Use of cash advances (short-term loan services) by card companies has also been on the rise for the second consecutive year. Amid a high-interest-rate era, it appears that low-income individuals in urgent need of funds are being driven to short-term loan products offered by card companies. As low-credit borrowers find themselves in a tight spot, there are concerns that the risk for card companies could increase due to a sharp rise in delinquency rates.

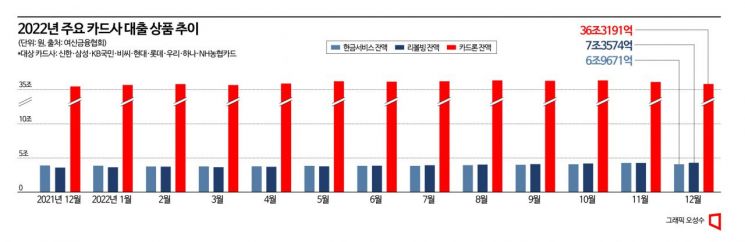

According to the Credit Finance Association on the 19th, the revolving balance of nine card companies?Shinhan, Samsung, KB Kookmin, BC, Hyundai, Lotte, Woori, Hana, and NH Nonghyup Cards?stood at 7.3574 trillion KRW as of the end of December last year. This represents an increase of 1.2125 trillion KRW (19.7%) compared to the end of the previous year. The balance has grown for ten consecutive months since March last year, reaching an unprecedented scale. Revolving is a service that allows credit card holders to pay only a portion of their bill in the current month and carry over up to 90% of the balance to the next month without any delinquency record. Because the burden of lump-sum repayment is reduced, it is mainly used by those in urgent need of funds.

Cash advances (short-term card loans), also considered a 'quick cash' channel, are likewise increasing. According to the Credit Finance Association, the cumulative usage amount of cash advances by the nine card companies last year was 56.6358 trillion KRW (domestic basis), up 2.7% from the previous year. It has shown a steady upward trend since 54.084 trillion KRW in 2020. The month-end balance of cash advances steadily increased from 6.4119 trillion KRW in February last year to surpass 7 trillion KRW in November. This is interpreted as low-credit borrowers flocking to these products amid the high-interest-rate era and tightened loan regulations.

The balance of card loans showed a relatively smaller increase compared to cash advances and revolving. As of the end of December last year, the card loan balance of the nine card companies was 36.3191 trillion KRW, showing a decline for two consecutive months. This is believed to be due to funding difficulties in the credit industry and the inclusion of card loans in the government's Debt Service Ratio (DSR) regulations. Last year, financial authorities included card loans in the regulation that if total loan amounts exceed 200 million KRW, the ratio of principal and interest repayment to annual income must not exceed 40%. As a result, those in urgent need of funds appear to be reluctantly choosing cash advances and revolving, which have higher interest rates than card loans.

Despite being the highest interest rate products in the high-interest-rate era, there are concerns that delinquency risks and financial institution insolvency risks could increase. According to the Credit Finance Association, the average interest rates for revolving among the nine card companies range from 13.29% to 18.40%. In some card companies, even those with credit scores exceeding 900 are subject to interest rates as high as 16.61%. For cash advances, the lowest average interest rate offered by BC Card is still 16.85%.

According to the Financial Supervisory Service, as of the third quarter of last year, the amount of overdue claims (over one month) for card companies was 1.7121 trillion KRW. According to the Financial Supervisory Service's electronic disclosure, the delinquency rate as of the third quarter last year ranged from 0.74% to 1.34%, slightly higher than the 0.25% to 1.35% range in the same period the previous year. The overall low delinquency rate in the industry is attributed to government measures such as loan maturity extensions and interest payment deferrals following COVID-19. This suggests that the actual delinquency rate could be higher.

With the base interest rate having been raised further, the level of interest rates is increasing, which could lead to a larger scale of delinquencies. Card companies are also focusing on risk management by lowering credit limits for some members and evaluating limits under stricter criteria.

Professor Ji Yong Seo of the Department of Business Administration at Sangmyung University explained, "Including card loans in the DSR regulation has caused a balloon effect, increasing revolving and cash advances. In the current situation where credit risk is rising due to the increase in high-interest-rate products, it is necessary to ease regulations, such as temporarily excluding card loans from the DSR regulation."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}