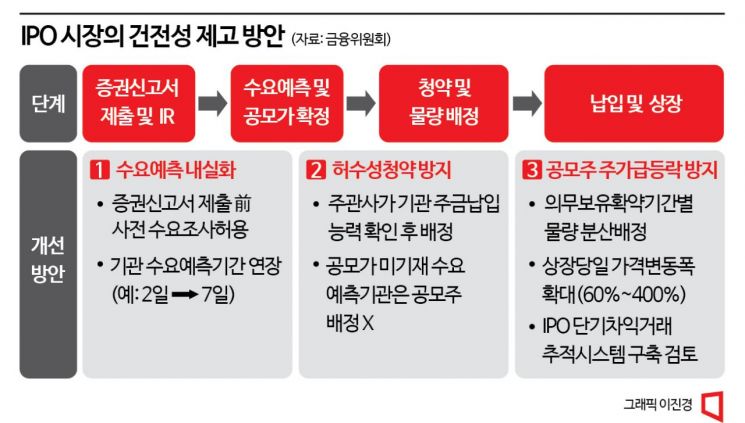

Preliminary Demand Survey Allowed Before Securities Registration Statement Submission

Penalty Restricting Participation in Demand Forecasting During Inflated Subscription

"Effectiveness Not Significant and Only Increasing Burden on Securities Firms" Concerns

[Asia Economy Reporter Lee Seon-ae] As the IPO market has sharply contracted due to sluggish stock markets, financial authorities are set to improve the IPO system. Expectations and concerns are mixed over whether this can maintain market soundness while revitalizing activity.

According to the Financial Services Commission and the financial investment industry on the 9th, the financial authorities plan to complete revisions to related regulations in the first half of the year and implement "measures to enhance IPO soundness, including prevention of fictitious subscriptions." To this end, a joint task force (TF) with related organizations and the industry will be operated in earnest starting this year.

The key points of the system improvement are ▲allowing preliminary demand surveys to set an appropriate public offering price band ▲confirming payment ability under the responsibility of the underwriter to conduct subscription and allocation ▲expanding the price fluctuation range on the listing day to enable early discovery of an appropriate equilibrium price.

Until now, preliminary demand surveys targeting institutional investors before submitting the securities registration statement were prohibited. However, the authorities plan to allow preliminary demand surveys so that underwriters can reasonably reassess the public offering price range through amendments to the Capital Markets Act. The customary two-day institutional demand forecasting period will also be extended to up to seven days. This aims to induce an appropriate public offering price within the price range.

The authorities plan to link this with the mid- to long-term introduction of the "cornerstone system," which allows some pre-subscription of public shares before submitting the securities registration statement. The cornerstone system refers to allocating a portion of the IPO shares to large institutional investors before the public offering price is finalized. It was established in Hong Kong in 2007 and is mainly used in Asian stock markets such as Singapore and Malaysia. Once introduced, certain qualified investors can be allocated some public shares before demand forecasting.

Measures to prevent "inflated (fictitious)" subscriptions will also be strengthened. It has long been a practice for institutional investors to place excessive subscriptions beyond actual demand to receive desired allocations. For example, LG Energy Solution, recorded as a historic "big fish" last year, had an abnormal institutional order amount of 1,500 trillion won at the time of its public offering due to fictitious subscriptions. The public offering price was set at the top end of 300,000 won. However, when the stock price did not rise as expected, controversy arose over the overvaluation of the public offering price. Individual investors complained that institutions only raised the public offering price during IPO demand forecasting and sold immediately after listing to pocket profits.

Underwriters will independently verify the payment ability of institutions placing fictitious subscriptions and allocate shares to demand forecasting participants according to their ability. To prepare for cases of poor management by underwriters, penalties will be increased. The authorities plan to establish grounds to impose up to suspension of business on underwriters who neglect verification duties. Institutions placing fictitious subscriptions will face significant reductions in allocated shares and restrictions on participation in demand forecasting. Institutions that do not state the public offering price in demand forecasting will not be allocated public shares.

The Financial Services Commission expressed expectations, saying, "By verifying actual payment ability to allocate shares and finding an appropriate public offering price through preliminary demand surveys, soundness will be secured." The financial investment industry also anticipates that verifying institutional payment ability and allocating shares accordingly will alleviate the market bubble caused by distorted public offering prices to some extent.

Allocating Shares by Verifying Institutional Payment Ability

To prevent situations where institutions sell large amounts of public shares all at once after the mandatory holding period ends, securities firms will allocate shares differentially according to the holding period commitment made by institutions. This aims to stabilize the stock price of public shares. Additionally, to quickly find the equilibrium price of public shares, the price fluctuation range on the listing day will be expanded. Currently, the stock price can fluctuate between 63% and 260% of the public offering price on the first day of listing, but the maximum fluctuation range will be increased to 400%.

A Financial Services Commission official explained, "Institutional investors will be provided with fair trading opportunities based on actual demand and payment ability, enabling stable long-term investment. Furthermore, underwriters will autonomously review and decide on public share demand, appropriate prices, and payment ability of subscription investors, thereby cultivating differentiated capabilities."

The current IPO market has rapidly contracted, with many companies canceling listing plans due to poor demand forecasting. Therefore, attention is focused on whether the system improvements can revitalize the market. Senior Research Fellow Lee Seok-hoon of the Capital Research Institute said, "Extending the demand forecasting period allows sufficient time to understand institutional investors' bidding demand and better predict market demand for public shares. Also, if underwriters identify an appropriate expected public offering price range through preliminary demand surveys and base demand forecasting on this, effective price discovery will be achieved."

However, there are concerns that the effectiveness may be limited since preliminary demand surveys are already conducted unofficially. Because underwriters' IPO staff and institutions communicate to some extent before demand forecasting to predict its success, it is not much different from conducting preliminary demand surveys. An industry insider pointed out, "Even if the number of demand forecasting institutions increases, not many institutions will participate. Without the simultaneous introduction of the cornerstone system, preliminary demand surveys will have little significance."

There are also criticisms that it is difficult for underwriters to verify the payment ability of institutions placing fictitious subscriptions. A securities firm official said, "It is difficult for underwriters to grasp each institution's status based only on documents. It is not desirable for securities firms to bear penalties and responsibility if incorrect information is intentionally or accidentally recorded in documents."

Expanding Fluctuation Range May Rather Dampen Investor Sentiment

Concerns have also been raised regarding the expansion of the price fluctuation range. In the past two years, due to excess liquidity, there have been cases of "ttasang" (when the opening price is twice the public offering price followed by a limit-up) and "ttasangsang" (when the opening price is twice the public offering price followed by two consecutive limit-ups), but these are rare in the public offering market. Critics argue that expanding the price fluctuation range to address this is illogical. Expanding the fluctuation range may lead investors to perceive the market as riskier, thereby dampening investor sentiment.

In response, the authorities claim that expanding the price fluctuation range aims to address the problem of price fixation and trading cliffs after ttasang, and that overheating up to 400% is unlikely, so equilibrium price discovery will be possible. The authorities also plan to establish a system to track short-term IPO arbitrage trading in the mid- to long-term to prevent sharp price fluctuations.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}