Transaction Volume Cut to One-Quarter Compared to Two Years Ago

Last Year's Operating Profit Decreased by Over 60% Year-on-Year

"Liquidity Concerns for Small and Medium Securities Firms to Grow"

[Asia Economy Reporter Minji Lee] The slowdown in securities firms' earnings is becoming a reality. Following the halving of trading volumes, which had reached record highs thanks to the Donghak Ant movement after COVID-19, profitability has turned red due to the sharp downturn in the real estate market. Large securities firms are rushing to strengthen their focus on individual customers and asset management to prevent client attrition, but small and medium-sized securities firms have yet to find a sharp solution to overcome this hardship.

According to the Financial Investment Association's comprehensive statistics service, as of the 3rd, the KOSPI trading value was 6.1491 trillion KRW, down by more than 2 trillion KRW compared to 8.1939 trillion KRW on January 3, 2022, a year earlier. Compared to the trading value of 25 trillion KRW recorded on January 4, 2021, two years ago, it has dropped to a quarter. The strong tightening stance of global central banks caused the stock index to fall by more than 30% over two years, leading to a massive exit of individuals who had enjoyed stock trading since COVID-19. Investor deposits, which serve as standby funds for the stock market, recorded levels of 60 to 70 trillion KRW from 2021 to the first half of last year but have fallen to the 50 trillion KRW range this year.

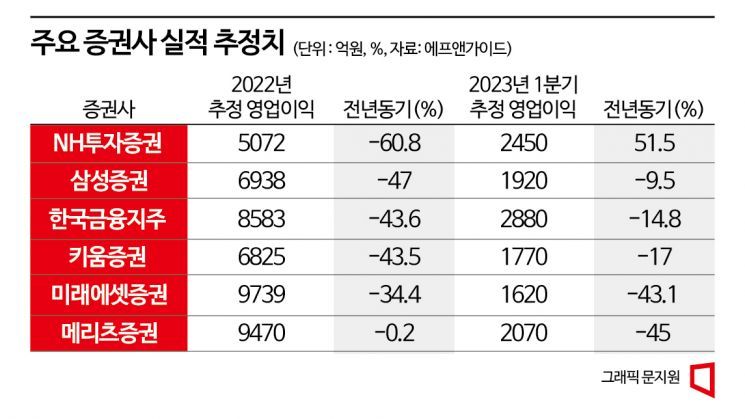

The profit decline in the retail sector (brokerage commissions, etc.), which has been the driving force behind securities firms' earnings over the past two years, is becoming more evident, and a series of earnings shocks is expected. Some securities firms are already expected to see their annual profits halved compared to last year. According to FnGuide, based on operating profit estimates from two or more securities research centers for last year, NH Investment & Securities recorded 507.2 billion KRW, shrinking by more than 60% compared to 1.2939 trillion KRW in 2021. Daishin Securities also recorded 309 billion KRW, a drop of more than 65% over the same period. Samsung Securities (-47%), Korea Financial Group (-43.6%), Kiwoom Securities (-43%), and Mirae Asset Securities (-34%) are also expected to record double-digit profit declines compared to the previous year.

An official from a securities firm said, “There is nowhere to lean on, whether retail, trading, or investment banking (IB) businesses, so it is daunting to figure out how to make money this year,” adding, “Thanks to the performance adjustment since the first quarter of last year, the decline will lessen from the first quarter of this year, but in absolute terms, it is still dismal.”

At least large securities firms can survive by focusing on asset management based on a solid retail customer base. KB Securities has created an asset management-dedicated organization called the 'Asset Management Group' to strengthen its WM (wealth management) division. NH Investment & Securities established a retail business division that combines asset management, Namu (MTS), and Premier Blue (PB). Hana Securities appointed Kang Sung-mook, who has strengths in the retail sector, as president to reorganize its profit structure around retail and asset management.

However, small and medium-sized securities firms with weak retail foundations find even this difficult. The retail sector of securities firms mainly earns revenue from credit loan fees and fees earned by depositing investor deposits with Korea Securities Finance, but small and medium-sized firms without a solid customer base cannot expect such income. It is also not a situation where aggressive marketing can covet the 'storehouse' next door. The only hopeful area is the bond trading sector, but since many have lowered bond rate sensitivity to reduce damage from rising interest rates, the benefits are expected to be limited.

Due to the increased exposure to bridge loans (pre-PF stage) and mezzanine/subordinated exposures in the real estate project financing (PF) market, it will take more time before liquidity concerns disappear. Yoon Yudong, a researcher at NH Investment & Securities, said, “It will take time for financial companies to prove their financial soundness capabilities to resolve PF issues,” adding, “Unless a low-interest, liquidity-driven market like in the past returns, it will be difficult to expect interest income from the retail sector.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}