Just Swipe Your Smartphone Screen to Open Payment Window Easily

3 Companies Participate, but Usage Scope Limitations Exist

Attracting Customers with Points and Discount Benefits

[Asia Economy Reporter Hyunji Kwon] On the 4th, in front of the cashier at a restaurant in Sangdo-dong, Dongjak-gu, Seoul, I opened the payment window of KB Kookmin Card's application (app) ‘KB Pay’ on my smartphone. I chose a Shinhan Card, which needs to meet a usage amount of 500,000 KRW this month, as the card for payment. After fingerprint recognition, I held the phone to the card payment terminal, and 1-2 seconds later, a receipt was printed as if to indicate the payment was completed.

It has been two weeks since the launch of the 'App Card Interoperability Service (Open Pay)', which allows registering and using other companies' card products within one credit card company's app. While convenience has greatly increased by enabling the use of various card products in a single company's app, the limited number of participating card companies and the lack of support for online payment functions remain challenges to be addressed in the future.

Shinhan, Hana, and KB Kookmin Cards launched the Open Pay service on December 22. Major card companies, latecomers in the pay market, joined forces to compete against early players such as Samsung Pay, Kakao Pay, Naver Pay, and the reportedly upcoming Apple Pay.

The card industry introduced the joint pay service after much difficulty because the simple payment market is rapidly growing. According to the Bank of Korea, the average daily number of simple payment service uses in the first half of last year was 23.17 million, with a transaction amount of 723.2 billion KRW. Compared to the first half of 2020 (12.93 million uses, 400.9 billion KRW), this represents an approximately 80% increase, showing a steep upward trend.

However, in the simple payment market, IT and big tech companies such as Samsung Pay, Kakao Pay, and Naver Pay hold a large share. In the first half of this year, these big tech companies accounted for 85.9% of total payments. Meanwhile, the financial sector's share decreased by 1.9 percentage points from a year ago to 14.1%. Recently, with Apple Pay preparing to enter, the position of card companies appears to be narrowing further.

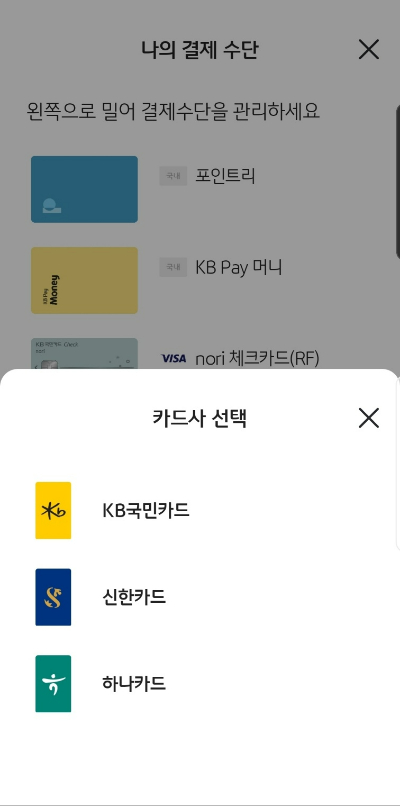

◆Usage is ‘super simple’… but usage restrictions remain=Using Open Pay is straightforward. First, access the card company app (KB Pay, Shinhan Play, One Q Pay), select the card company you want to link under the ‘Register Payment Method’ tab, and enter card number, expiration date, and other information to complete registration.

For payment, after fingerprint recognition or password input, simply hold the smartphone to the card payment terminal (based on Samsung smartphones). Regardless of which app is used, you can set the card of your desired card company as the ‘representative card.’ Previously, to use each card company's simple payment service, you had to install each card company's app individually, but now you can use other companies' cards with just one app, reducing inconvenience.

It also has handy convenience features. Similar to Samsung Pay, which switches to the payment screen by swiping up on the smartphone screen without entering the app, KB Pay and Shinhan Play have an ‘Edge Panel’ feature. After activating this function, touching the upper right corner of the smartphone home screen (location selectable) and dragging left immediately switches to the payment screen.

Although a latecomer, it has some specialized advantages over existing simple payment services. Open Pay uses the payment network already established by card companies, making it easy to use even in local neighborhood markets. Unlike convenience stores and large commercial areas equipped with infrastructure for Kakao Pay and Naver Pay barcode payments, neighborhood markets that do not have all these infrastructures require physical card use, where Open Pay has an advantage. The card companies' big data capabilities are also a strength. An industry insider explained, “We can provide personalized services using big data, which is among the top in the entire industry.”

◆Expansion of participating companies by the second half… “Marketing will be activated”=On the other hand, there are clear drawbacks. First, only three companies participate, limiting universality. Contrary to the initial plan where six card companies including Lotte, BC, Shinhan, Hana, KB Kookmin, and NH Nonghyup Cards were to participate, only three companies have joined initially. If a user has fewer than two participating card companies, the utility is not very high. In the reporter’s case, the main card company did not participate in Open Pay, so the service was rarely used during the two weeks of trial. Unlike other simple payment services such as Samsung Pay, Kakao Pay, and Naver Pay, the inability to make online payments is also a limitation.

Therefore, card companies plan to continuously improve the service to enhance customer convenience. The key is expanding universality. All remaining card companies need to participate to fulfill the original purpose of the service. It is encouraging that the number of participating card companies is increasing in the first half of this year. Lotte Card and BC Card are scheduled to join in February and March respectively, and NH Nonghyup will join in the second half. Woori Card has also decided to participate. Online payments are expected to become available by the second half of the year. A card industry official stated, “We plan to activate marketing by offering point accumulation and discount benefits to Open Pay users.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}