Savings Banks and Internet Banks Interest Rates Similar to Fixed Deposit Rates

Disadvantageous for Fund Management and Lower Profitability

Long-term Consumer Burden Increases with Loan Interest Rate Hikes

[Asia Economy Reporter Hyunji Kwon] The competition for demand deposit accounts that pay interest even for a short deposit period, so-called parking accounts, is heating up. As liquidity flows into deposits due to the base interest rate hike, savings banks and internet-only banks have each raised deposit interest rates to attract customers and secure short-term funds. However, there are forecasts that this trend will not last long as profitability is low and fund management is not easy.

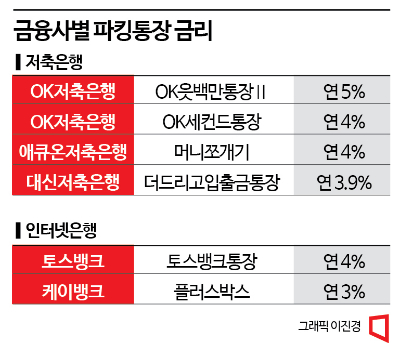

According to the financial sector on the 29th, OK Savings Bank launched the parking account ‘OK Eut Baekman Account II’ with an annual interest rate of 5% on the 26th. It offers a base interest rate of 4.5%, plus an additional preferential rate of 0.5 percentage points when registered with open banking, providing up to 5% annual interest on deposits up to 5 million KRW. The interest rate of the existing parking account ‘OK Second Account’ was also raised to a maximum of 4% annually (up to 50 million KRW). Accuon Savings Bank’s ‘Money Jjogaegi’ and Daeshin Savings Bank’s ‘The Deurigo Demand Deposit Account’ offer interest rates of 4% and 3.9%, respectively.

The situation is no different for internet-only banks. Toss Bank, the pioneer of parking accounts, applies an annual interest rate of 4% on amounts exceeding 50 million KRW starting this month, and K Bank also raised the interest rate of ‘Plus Box’ to 3% annually.

A parking account is a term combining parking and account, meaning an account where money can be deposited and withdrawn anytime as if temporarily parking. Unlike fixed deposits that require a minimum deposit period of one month to over three years, parking accounts have no restrictions on deposit period or number of transactions, making them popular among consumers seeking high interest. For this reason, parking account interest rates are usually formed around 0.1% to 1.0% annually, lower than fixed deposit rates at commercial banks. However, currently, a rare phenomenon is occurring where parking account and bank fixed deposit interest rates are similar at around 4% to 5% annually.

However, many analyses suggest that the current interest rate competition will not last long. First, funds raised through parking accounts are disadvantageous for stable management. Unlike fixed deposits, parking accounts have the advantage of securing large amounts up to 50 million KRW in a short period, but since the money can be withdrawn anytime, it is unsuitable for lending activities. A savings bank official explained, “If funds come in quickly and leave quickly, savings banks, which are smaller in scale than commercial banks, face greater deposit volatility and become vulnerable.”

Profitability also declines. Since the legal maximum interest rate is capped at 20%, raising deposit interest rates inevitably reduces the interest margin. A banking official predicted, “It will not be easy to continuously maintain demand deposit products that pay interest rates higher than fixed deposits.”

In the long term, raising deposit interest rates encourages loan interest rate hikes, increasing the burden on borrowers. A savings bank official said, “Continuous deposit interest rate increases may be beneficial for customers in the short term by providing financial benefits, but if prolonged, they will be reflected in loan interest rates and ultimately passed on to customers.”

In fact, loan interest rates at these financial institutions are on the rise. According to the Korea Federation of Savings Banks, as of last month, the average interest rate on household credit loans at the top five savings banks by asset size (SBI, Welcome, OK, Pepper, Korea Investment) was 16.55% annually, up 1.12 percentage points from the previous month. Toss Bank, which is active in parking accounts, saw its household loan interest rate exceed 7% shortly after August this year and rose to 8.61% as of November. K Bank and Kakao Bank also show a continuous upward trend, with average rates of 6.6% and 5.52%, respectively, as of November.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}