[Asia Economy Reporter Song Hwajeong] The ratio of non-performing loans (NPLs) at banks remains at an all-time low, and it is expected to improve further in the fourth quarter.

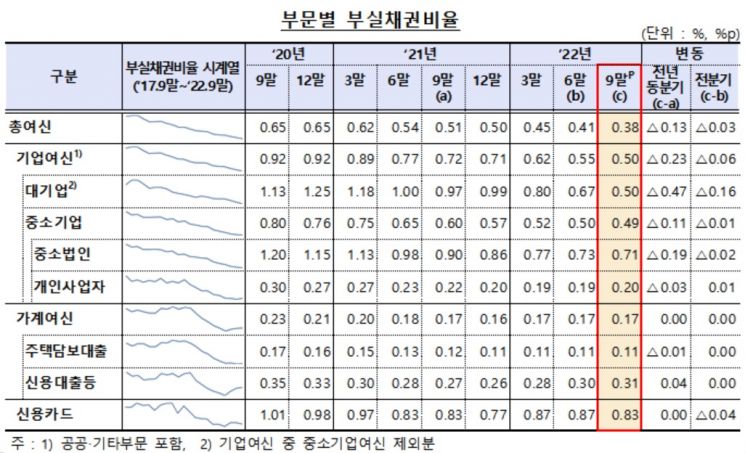

According to the Financial Supervisory Service on the 10th, the NPL ratio of domestic banks as of the end of September stood at 0.38%, down 0.03 percentage points from the end of the previous quarter. Compared to the same month last year, it decreased by 0.13 percentage points. The banks' NPL ratio has recorded the lowest level for nine consecutive quarters since the third quarter of 2020.

In the third quarter, NPLs amounted to 9.7 trillion KRW, a decrease of 600 billion KRW (5.5%) from the end of the previous quarter, while total loans increased, resulting in a decline in the NPL ratio. Newly generated NPLs during the third quarter were 2.5 trillion KRW, up 100 billion KRW from the previous quarter. Newly defaulted corporate loans were 1.8 trillion KRW, and newly defaulted household loans were 600 billion KRW, each increasing by 100 billion KRW compared to the previous quarter.

By sector, the NPL ratio for corporate loans was 0.5%, down 0.06 percentage points from the end of the previous quarter, while the NPL ratio for household loans remained similar at 0.17%. The NPL ratio for credit card loans was 0.83%, down 0.04 percentage points from the end of the previous quarter.

The scale of NPL disposals in the third quarter was 3 trillion KRW, an increase of 200 billion KRW compared to the previous quarter.

Kim Eungap, a researcher at IBK Investment & Securities, said, "Although there are market concerns about asset quality in the banking sector due to economic downturn and rising interest rates, asset quality indicators are improving. Since the scale of disposals is larger than newly generated NPLs, the decrease in the NPL balance means the decline in the NPL ratio should not be dismissed as an illusion caused by loan growth."

The banks' NPL ratio is expected to improve further in the fourth quarter. Researcher Kim said, "In the banking sector, if the scale of NPL sales and write-offs expands in the fourth quarter, the NPL ratio will improve further."

The banks' loan loss provision coverage ratio has also increased significantly. The loan loss provision coverage ratio, which indicates the ability to absorb credit losses, rose to 223.9% as of the end of September. The coverage ratio increased from 138.3% at the end of 2020 to 165.9% at the end of 2021. It has continued to rise this year, reaching 181.6% in the first quarter and 205.6% in the second quarter. Researcher Kim explained, "This phenomenon occurred due to the increased proactive provisioning for the economic downturn after COVID-19," adding, "There is a possibility that additional provisions will be made in the fourth quarter due to seasonal characteristics."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}