Short- and Long-Term Government Bond Yields Fall

Corporate Bond Yields Also Slightly Decline

Investor Sentiment Expected to Improve in Early Next Year

Credit Expected to Gradually Stabilize Until Late Next Year

[Asia Economy Reporter Minji Lee] As the Monetary Policy Committee (MPC) of the Bank of Korea signaled its intention to pursue a gradual interest rate hike, escaping pressure from inflation and exchange rates, the bond market is cheering. Treasury bond yields, both short- and long-term, have sharply declined to levels seen two months ago, and corporate bond yields have also fallen slightly. Experts predict that the interest rate hike cycle is nearing its end based on the MPC's recent decision. It is analyzed that investor sentiment in the bond market will improve smoothly in the first half of next year, potentially stabilizing the credit market as well.

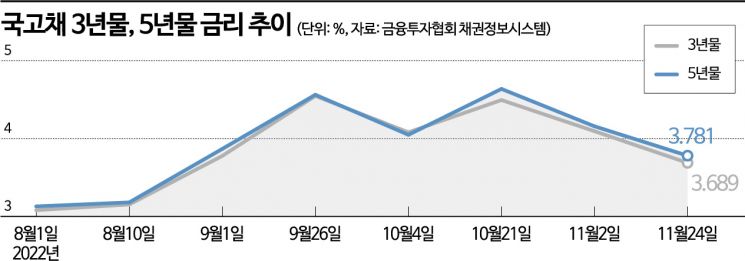

According to the Bond Information System of the Korea Financial Investment Association on the 25th, the yield on the 3-year Treasury bond was 3.689%, down 20 basis points (1bp=0.01%p) from the previous day. This stabilization in Treasury yields came as the MPC implemented a baby step rate hike and analysts anticipated a final rate level of 3.5%. Treasury yields continued to decline in the morning session. The government's liquidity supply measures to stabilize the bond market also had an effect; compared to a month ago (4.305%), the 3-year Treasury yield dropped about 61bp. Over the same period, the 5-year Treasury yield fell 77.3bp to 3.718%, and the 10-year Treasury yield was 3.622%, down 88.1bp, returning to levels seen two months ago.

Corporate bond yields, which had been stubborn despite government measures, also showed a downward trend. Overcoming year-end effects and negative institutional sentiment toward credit bonds, the 3-year (AA- rated) corporate bond yield recorded 5.4%, falling more than 30bp from the year's high of 5.73%. However, since the decline in Treasury yields was larger, the credit spread (the difference between the 3-year AA- corporate bond yield and the 3-year Treasury yield) did not narrow. As of the previous day, the credit spread was 178bp, marking a new yearly high. Due to six consecutive rate hikes, the 91-day Commercial Paper (CP) rate also rose again to 5.48%. Since CP rates are linked to the base rate, they are expected to remain high until the rate hike cycle ends.

With the MPC emphasizing "one rate hike in the first half of next year, final rate at 3.5%," supply and demand in the bond market are expected to improve in the first half of next year. Furthermore, there is analysis suggesting one or two rate cuts could occur around the fourth quarter of next year, which is expected to continue the downward trend centered on government bonds. Seungwon Kang, a researcher at NH Investment & Securities, explained, "Considering that the MPC has stopped upward revisions to inflation forecasts since February last year, the future policy focus will be on domestic economic conditions," adding, "Given the decline in government bond yields, it is necessary to increase buying mainly in long-term bonds."

Credit bonds are predicted to show a spread narrowing trend in the first half of the year, supported by the New Year effect of revived institutional sentiment and expectations of rate cuts in the second half. Currently, in the credit secondary market, purchase orders are mainly concentrated on public and bank bonds and high-quality credit bonds rated AA or higher, while quasi-government bonds and lower-rated bonds maintain high yields. On this day, Hana Capital (AA-) issued a 2-year bond worth 10 billion KRW with a coupon rate reaching 7.195%. Minji Hee, a researcher at Mirae Asset Securities, analyzed, "Although there are concerns about further widening due to recession and possible US rate hikes, the Bank of Korea's shift to a more accommodative monetary policy stance will lead to attempts to narrow spreads," adding, "Toward the end of next year, investment attractiveness will increase mainly in high-quality corporate bonds with credit ratings that have significantly widened spreads relative to corporate value."

However, some caution that the final rate level could expand up to 3.75%. Since the consumer price inflation rate still exceeds the inflation target, the Bank of Korea's response to control inflation may be prolonged. Dongrak Gong, a researcher at Daishin Securities, said, "Although the possibility of further base rate hikes has been confirmed, the rapidly falling government bond yields seem somewhat excessive," and explained, "Strategically, chasing purchases of government bonds at this time does not appear advisable."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}