Sales Slightly Increased but Net Profit Decreased by 29.9%

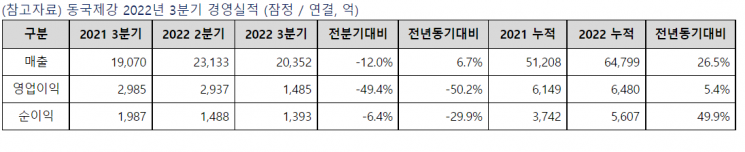

[Asia Economy Reporter Choi Seoyoon] Dongkuk Steel announced on the 31st that its consolidated operating profit for the third quarter of this year amounted to 148.5 billion KRW, a 50.2% decrease compared to the previous year.

Sales increased by 6.7% during the same period to 2.0352 trillion KRW, but net profit decreased by 29.9% to 139.3 billion KRW.

Regarding the poor third-quarter performance, Dongkuk Steel stated, "Volatility in domestic and international raw material prices caused overall weakness in product prices," and "The long steel products segment, which accounts for about 50% of Dongkuk Steel’s sales, experienced a decline in sales volume due to the seasonal off-season in the third quarter."

They added, "In the flat steel segment, including cold-rolled, color-coated steel, and thick plates, sales of cold-rolled and color-coated steel were constrained due to weak demand in home appliances and construction sectors," and "Despite market fluctuations, thick plate sales volume was maintained through proactive sales efforts." The performance of subsidiaries such as Intergis and Dongkuk Systems helped partially offset losses.

Despite the downturn in demand from upstream industries, Dongkuk Steel has continued a profitability-focused sales strategy. To proactively respond to the global complex crisis, the company improved its financial structure in the third quarter by pursuing the sale of the Brazilian CSP steel mill and divesting shares in its Chinese subsidiary (DKSC).

The debt ratio also entered double digits. The consolidated debt ratio for the third quarter was 90.6%, improving by 37.0 percentage points from 127.6% last year. Consolidated total borrowings decreased by 242.7 billion KRW to 1.9464 trillion KRW in the third quarter from 2.1891 trillion KRW last year. Consolidated cash and cash equivalents increased by 142.9 billion KRW from 428.4 billion KRW to 571.2 billion KRW during the same period.

Based on the improved financial structure, Dongkuk Steel expects further credit rating upgrades. In the first half of this year, Dongkuk Steel’s credit rating was upgraded from BBB (stable) to BBB (positive) by Korea Ratings and Korea Investors Service, and recently, Korea Ratings further upgraded Dongkuk Steel’s credit rating from BBB (positive) to BBB+ (stable).

In the third quarter, Dongkuk Steel focused on establishing eco-friendly workplaces. All business sites obtained the international energy management standard ISO 50001 certification, and the Pohang plant became the first in the industry to acquire the circular resource quality mark certification for ‘mill scale.’ The steelshop sales portfolio was also expanded. At the steelshop, sales were extended beyond general rebar products to include SD500, SD600, and seismic-resistant steel grades, and direct sales of shaped steel began.

In the flat steel segment, cold-rolled and color-coated steel exports were expanded in the third quarter due to the sustained high exchange rate, and sales focused on high value-added products. Thick plates diversified their product lineup to preserve profitability by including high-margin products such as pipe and construction thick plates, special steel thick plates, and emergency stock responses according to market fluctuations.

Dongkuk Steel plans to focus on building eco-friendly workplaces and expanding differentiated competitiveness centered on its mid- to long-term ESG management strategy ‘Steel for Green’ and the color-coated steel future strategy ‘DK Color Vision 2030.’

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}