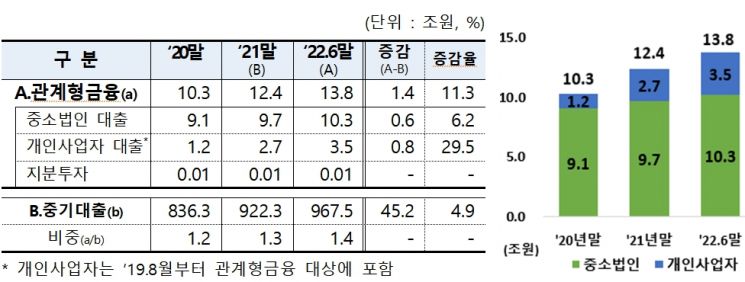

[Asia Economy Reporter Song Seung-seop] In the first half of this year, the balance of relational finance at domestic banks reached 13.8 trillion KRW, an increase of 11.3% (1.4 trillion KRW) compared to the end of last year. The supply of stable long-term funds with maturities of over three years to small and medium-sized enterprises (SMEs) and self-employed individuals has expanded.

According to the Financial Supervisory Service on the 28th, loans to individual business owners increased by 295% (800 billion KRW), and loans to SMEs rose by 6.2% (600 billion KRW). In addition to loan and fund supply, a total of 2,688.5 hours of non-financial services (management, accounting, and tax consulting) were provided.

Relational finance refers to providing loans, equity investments, and management consulting for over three years to companies with low credit ratings or insufficient collateral but with favorable business prospects. Banks conduct relational finance by comprehensively evaluating not only quantitative information but also qualitative information (such as expertise and client stability) of the companies.

The balance of relational finance has been steadily increasing. It rose by 20.8% from 10.3 trillion KRW at the end of 2020 to 12.4 trillion KRW at the end of last year. Although statistics for the second half of the year have not yet been compiled, the balance of relational finance has already exceeded 13 trillion KRW.

By borrower type, loans to small and medium-sized corporations accounted for 74.5%, totaling 10.3 trillion KRW. Loans to individual business owners amounted to 3.5 trillion KRW. Loans to individual business owners increased by 800 billion KRW compared to the end of the previous year, and loans to small and medium-sized corporations increased by 600 billion KRW. By industry, wholesale and retail trade accounted for the largest share at 31.3%, followed by manufacturing (29.0%), services (15.4%), and food and accommodation (7.1%).

The average loan interest rate was 3.35%, rising by 0.52% from 2.83% at the end of last year due to the impact of the base interest rate hike.

In the first half of the year, NongHyup Bank (large) and Gwangju Bank (medium and small) were selected as excellent banks. In the large group, NongHyup Bank excelled in the proportion of loans to low-credit borrowers, the proportion of loans to early-stage companies, and the number of business agreement signings. Shinhan Bank, which ranked second, showed somewhat sluggish growth in supply but scored high in the proportion of loans to self-employed individuals and unsecured loans.

In the medium and small group, Gwangju Bank ranked first by scoring high in the number of business agreement signings, the proportion of loans to low-credit borrowers, and the proportion of unsecured loans. Gyeongnam Bank, ranked second, showed excellent performance in the proportion of loans to self-employed individuals and non-financial service support despite a low proportion of unsecured loans.

The Financial Supervisory Service plans to continue expanding the supply of relational finance to support SMEs and individual business owners in overcoming crises amid difficult economic conditions. Through meetings with the banking sector, it will encourage continuous expansion of relational finance supply and sufficient support for non-financial services such as consulting. Additionally, to increase relational finance supply to borrowers with insufficient collateral or medium to low credit ratings and to actively provide non-financial services such as consulting, the scoring criteria for related excellent banks will also be expanded.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}