Chinese Government Confident in Economic Rebound in Second Half

Strong Consumer Recovery Expected to Boost Commerce Sector Growth,

Management's Profitability Improvement Remarks Also Positive

[Asia Economy Reporter Minji Lee] Alibaba is expected to show improved performance in the second half of the year, supported by the recovery of the Chinese economy. Its stock price is also on the rise amid expectations of a performance rebound.

On the 6th, Alibaba's stock price stood at 92.9 Hong Kong dollars. Over the past five trading days, the stock price has risen by 5.39%. As forecasts for an economic improvement in China in the second half of the year have expanded and analyses suggest that the second-quarter performance has bottomed out, investor sentiment has strengthened.

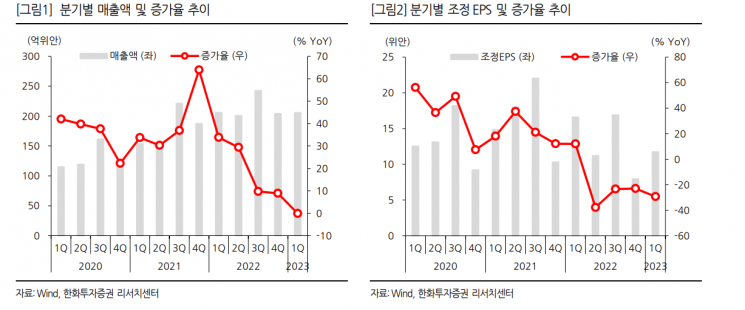

For the first quarter of the fiscal year (April to June 2022, second quarter), revenue was 205.5 billion yuan, showing a flat trend compared to the previous year. This is higher than the market expectation of 203.2 billion yuan. Net profit attributable to controlling shareholders was 27.7 billion yuan, down 50% year-on-year, and Non-GAAP net profit attributable to controlling shareholders was 30.2 billion yuan, down 30% over the same period.

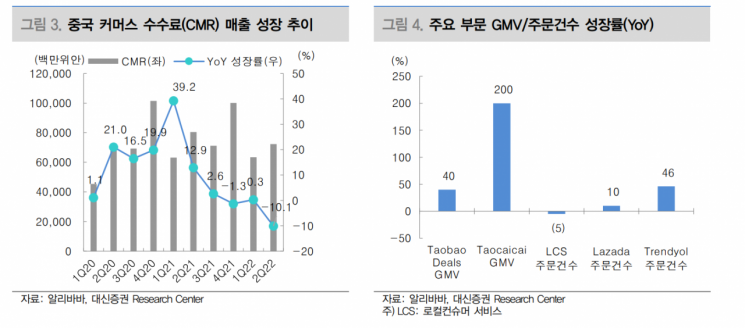

By business segment, commerce division revenue was 141.9 billion yuan, down 1.5% year-on-year, marking the first contraction since listing. Due to the impact of COVID-19 lockdowns in April and May, transaction volume fell to single digits, causing platform CRM fee revenue to decline by 10% year-on-year to 72.3 billion yuan. Park Chohwa, a researcher at Daishin Securities, said, “Considering the 8% growth rate in e-commerce transaction volume for the second quarter announced by the National Bureau of Statistics, this is somewhat disappointing.”

Revenue from the overseas commerce division was 15.4 billion yuan, growing 1.6% year-on-year, but the growth rate significantly slowed. It was affected by the depreciation of emerging market currencies, the Ukraine crisis, and a slowdown in e-commerce growth after reopening in Southeast Asia. After reaching 1 billion active customers in Chinese commerce last quarter, specific figures have not been disclosed, but it appears efforts are focused more on retaining high-ARPU (average revenue per user) subscribers rather than increasing new inflows. In the second quarter, the number of users spending over 10,000 yuan annually was 110 million, 88VIP members numbered 25 million, and annual spending was 57,000 yuan. The cloud division recorded revenue of 18.9 billion yuan. Although growth was limited to 10% year-on-year due to the economic slowdown, the revenue share from non-internet industry sectors improved by 5 percentage points to 53% compared to the previous year.

In the securities industry, Alibaba is expected to show improvement from the second quarter as a bottom. Since consumption recovery has been confirmed from July, performance recovery is anticipated with economic normalization in the second half of the year. Furthermore, management’s mention of profitability improvement through cost optimization is also positive. Accordingly, Alibaba is expected to adjust the pace of investment in loss-making platforms such as Ele.ma, Taocaicai, and Taobao Deal and to execute costs efficiently. Lee Dong-yeon, a researcher at Korea Investment & Securities, analyzed, “Cost optimization will continue in the core commerce segment, which is the key business,” adding, “The focus on ARPU increase in the commerce segment is also positive for profitability.”

The share repurchase plan is also a positive factor. In March, the company raised the plan to $25 billion by March 2024, and as of the end of June, it was found to have a share repurchase capacity of $12 billion.

However, investors should be cautious due to remaining risks from government regulations and tensions between the U.S. and China. Although the enforcement of the revised Chinese antitrust law is expected to be less stringent than before, it is more appropriate to view the company as still passing through a regulatory tunnel. Hwang Sun-myung, a researcher at Samsung Securities, said, “Alibaba’s valuation is in an oversold phase, but responses should be based on the progress of domestic and international risk factors.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}