Year-end USD-KRW Exchange Rate Reaches 1350 Won "Upside Risk, Foreign Panel Selling Induced"

Inflation Indicators Becoming Unstable Again May Increase Financial Market Volatility

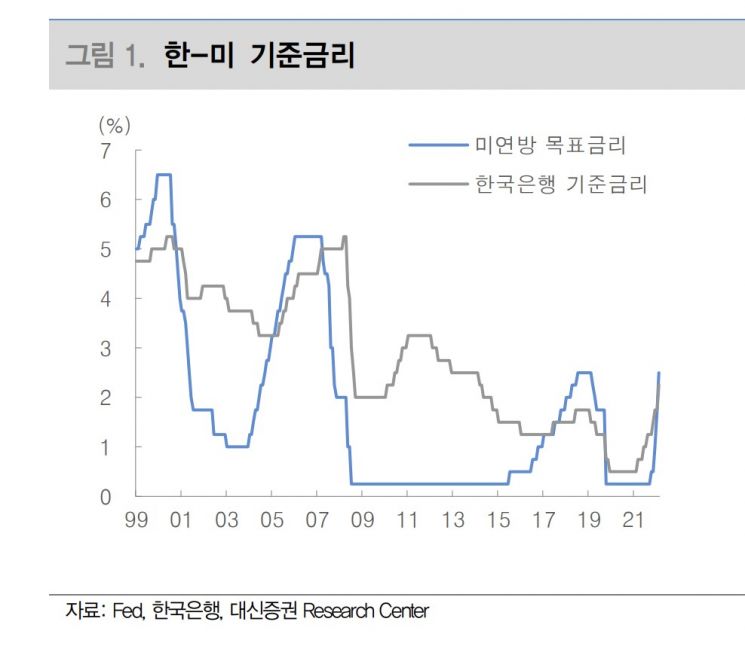

[Asia Economy Reporter Lee Seon-ae] As the U.S. central bank, the Federal Reserve (Fed), raised its benchmark interest rate from 1.75% to 2.50% in July, surpassing South Korea's benchmark rate (2.25%) and causing the Korea-U.S. interest rate differential to invert for the first time since March 2018, the interest rate gap is expected to widen further by the end of the year. This has drawn attention to the potential impact on the domestic stock market in the third and fourth quarters. Based on past cases of Korea-U.S. interest rate inversion, the possibility of a sharp outflow of foreign capital solely due to the rate inversion is low, and the KOSPI's direction has varied, leading to somewhat mixed expert opinions on the impact on the domestic capital market. However, the story changes when the 'exchange rate' issue is considered. With the year-end interest rate gap expected to widen up to 0.5 percentage points and the won-dollar exchange rate breaking through 1,310 won for the first time in 13 years, there are forecasts that it could rise to 1,350 won, suggesting that caution is needed regarding KOSPI volatility and foreign capital outflows.

According to the financial investment industry on the 2nd, as the interest rate differential is expected to widen further in the second half of the year, upward pressure on the won-dollar exchange rate is a concern. This ultimately means a high possibility of stimulating foreign capital outflows. Although foreigners, who had been continuously 'selling Korea,' turned to net buying in the domestic stock market for the first time last month, considering the upward risk of the exchange rate, capital could again flow out like an ebb tide. Typically, emerging markets have weaker economic fundamentals compared to developed countries, so when the interest rate differential narrows during the developed countries' rate hike cycle (emerging market rates > developed market rates), foreign investors may withdraw their funds.

Da-eun Lee, a researcher at Daishin Securities, noted, "In the second half of the year, the won-dollar exchange rate is expected to fluctuate between 1,250 and 1,350 won, with a high upward risk," adding, "Although the dollar strength pressure from monetary policy may gradually ease as the rate hike cycle is halfway through, other macroeconomic environments remain challenging." She continued, "Reflecting domestic and external fundamental weaknesses, the won is likely to continue weakening in the second half. Considering the preference for safe assets due to global economic slowdown, euro weakness due to deteriorating Eurozone fundamentals, and relatively robust U.S. economic fundamentals, the U.S. dollar strength remains valid, but there are hardly any factors supporting won strength."

Looking at past cases of Korea-U.S. interest rate inversion, capital outflows did not necessarily occur just because rates inverted. Especially for emerging markets, not only external factors such as global economic uncertainty but also internal factors like domestic fundamentals influence capital movements. The problem lies with Korea's economy. The researcher pointed out, "Looking at the background of the recent won-dollar exchange rate surpassing 1,300 won, domestic and external factors are complexly intertwined, similar to the past," adding, "Currently, the Korean economy faces issues such as household debt and a decline in global trade volume."

As of the end of Q1 2022, Korea's household debt-to-GDP ratio was 104.3%, ranking first among 36 major countries worldwide. Another risk to Korea's economy in the second half is the global economic slowdown and reduced global trade volume due to China's economic weakness. External factors are also significant. With inflation and U.S. monetary policy impacts pushing the global policy uncertainty index above 200 points, factors such as a strong dollar, developed countries' rate hikes, signs of global demand slowdown, and inflation are weakening emerging market economic momentum. Due to these phenomena, the researcher believes that the exchange rate will face strong upward risk pressure by year-end.

Exchange rate risk is negative for the domestic stock market as it can induce foreign investors' panic selling due to concerns over foreign exchange losses. Accordingly, advice has been given to keep KOSPI volatility in mind.

Including the fourth inversion following the Fed's rate hike on the 27th of last month (local time), there have been three periods of Korea-U.S. benchmark interest rate inversion since 1990 (June 1999?March 2001, August 2005?September 2007, March 2018?February 2020). The maximum interest rate gaps during each period were 150 basis points, 100 basis points, and 100 basis points, respectively.

During the first inversion period, the Korea-U.S. interest rate gap widened to 1.50 percentage points. At that time, Korea lowered rates following the foreign exchange crisis amid expectations of a sovereign credit rating upgrade, while the U.S. raised rates to cool down the dot-com bubble. During this period, the KOSPI fell about 35%. The KOSPI, which had risen to 851 in July 2000, dropped to 688 the following month, closing the year at 504.62. Foreign capital actually flowed in for bottom-fishing. In the second inversion period, the opposite occurred. It was a time when China's massive monetary expansion caused demand-driven inflation. The U.S. rapidly raised benchmark rates to cool the real estate and stock market boom, but the Bank of Korea could not keep pace, causing the Korea-U.S. rate gap to widen by 1.00 percentage point. The KOSPI surpassed 2,000, rising 90%, while foreign capital flowed out. During the third inversion period, Korea, hit by the U.S.-China trade dispute affecting exports, found it difficult to significantly raise benchmark rates. The KOSPI fell 17%, and foreigners turned their backs on the domestic stock market.

Looking at these three past records, the KOSPI's movements were varied. Experts diagnose that the current interest rate inversion is similar to the third case. At that time, the Korean economy was frozen by the U.S.-China trade conflict, with consumption stagnating and low growth concerns intensifying. If U.S. inflation indicators rise further, the interest rate gap will widen further, potentially accelerating capital outflows.

Yumi Kim, a researcher at Kiwoom Securities, cautioned, "In the short term, the financial market may be relieved by easing concerns over the Fed's aggressive tightening, but if inflation indicators become unstable again in September, it is necessary to keep in mind the possibility of renewed financial market volatility."

However, some argue that there is a defensive aspect and that excessive concern should be avoided. This is based on the judgment that further declines are limited. The KOSPI has fallen 18.21% this year, with the price-to-book ratio (PBR) dropping to around 0.9 times, a level seen during the financial crisis, suggesting limited room for further decline. Hyunki Kang, a researcher at DB Financial Investment, said, "The domestic stock market has already priced in concerns such as U.S. inflation, rate hikes, and the Korea-U.S. rate inversion, forming the current valuation level," adding, "Based on past experience, the additional decline in the Korean stock market triggered by the Korea-U.S. rate inversion is unlikely to be significant, and it is unreasonable to predict further declines by comparing the current situation to the past."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}