[Asia Economy Reporter Lee Seon-ae] South Korea's inclusion in the Morgan Stanley Capital International (MSCI) Developed Markets Index has once again been delayed. This year, it remains classified under the Emerging Markets Index. Since being included in the Emerging Markets Index in 1992, it has not been "upgraded" to Developed Market status for 30 years. Among major countries worldwide, the KOSPI's steep decline has been the most pronounced, severely damaging its reputation as the "lowest-ranked" market. To pass MSCI's market accessibility evaluation, various laws must be amended. Moreover, the full allowance of short selling, which individual investors are extremely concerned about, is also necessary. Accordingly, the financial investment industry views the "KOSPI's advancement to Developed Market status" as a challenging and difficult task.

According to the market reclassification results announced by MSCI on the 23rd (local time), South Korea was not included as a candidate (watchlist country) for the Developed Markets Index this year. Ultimately, South Korea has failed in all four attempts, including in 2008, 2015, June last year, and June this year.

MSCI decides on market reclassification, such as Developed or Emerging, every June for countries on the watchlist. To be reclassified, a country must have been on the watchlist for at least one year. Therefore, the government's target schedule was: ① inclusion on the watchlist in June 2022, ② decision on MSCI Developed Markets Index inclusion in June 2023, and ③ actual inclusion in June 2024. However, failing to be listed on the watchlist this time means South Korea must attempt for the fifth time in June next year. The target timeline has been delayed consecutively.

The failure to be listed on the watchlist was largely anticipated. This is because South Korea's stock market received failing marks in MSCI's country-specific market accessibility evaluation announced on the 10th. South Korea was pointed out for needing improvements due to insufficient information for foreign investors, corporate governance issues, restrictions on short selling, and dividend disclosure practices that differ from international standards. Comparing this year's report card with last year's, there was no category where improvements were recognized. In fact, the score for the item concerning SK Telecom's foreign ownership limit decreased due to the limited remaining capacity.

Repeatedly criticized areas include the absence of an offshore foreign exchange (spot FX) market (foreign exchange market liberalization), lack of English disclosure materials (information flow), limitations on product development due to restrictions on stock market data usage (investment product availability), difficulties in spot transfers and over-the-counter trading (transferability), burdensome documentation for mandatory foreign investor registration (investor registration), prohibition of securities settlement with borrowed funds (clearing and settlement), and the full allowance of short selling.

Although the government announced on the 16th that Seoul's foreign exchange market operating hours would be extended until 2 a.m. Korean time (the closing time of the London foreign exchange market) and would be gradually expanded to 24 hours in the future, MSCI did not mention this in its recent announcement. Yeom Dong-chan, a researcher at Korea Investment & Securities, noted, "This MSCI evaluation should be understood as MSCI emphasizing the importance of the government's willingness to improve but stating that they will change the evaluation only after confirming actual improvements."

While inclusion in the Developed Markets Index is a long-cherished goal of the government, it is practically difficult. The key issue is the "absence of an offshore spot FX market." For global investors, the existence of a market where they can freely convert the local currency into dollars at any time when investing in a country's stocks is very important. Currently, South Korea only has an onshore spot FX market (interbank market) and an offshore non-deliverable forward (NDF) market. Offshore spot FX trading, which would allow free exchange of Korean won and US dollars after the onshore market closes, is not permitted.

To improve foreign investors' information accessibility as required by MSCI, mandatory English disclosure would require amendments to the Capital Markets Act, and changes to the dividend payment process would require amendments to the Commercial Act. Among MSCI's improvement demands is also the rigidity of off-exchange trading. This fundamentally may require changes to Korea's tax laws, which impose securities transaction tax and capital gains tax on off-exchange transactions. Researcher Yeom emphasized, "There are still many hurdles South Korea must overcome to be classified as an MSCI Developed Market," adding, "Looking at MSCI's requirements, the path to becoming a Developed Market is not smooth."

Additionally, the full allowance of short selling is an important factor. Short selling is a trading technique where investors borrow stocks expected to decline in price, sell them, and then repurchase them at a lower price to realize a profit. It was fully banned in 2020 to prevent further sharp declines when the domestic stock market was severely shaken by the COVID-19 outbreak. Since then, it has only resumed for selected blue-chip stocks in the KOSPI 200 and KOSDAQ 150 indices. However, individual investors strongly oppose full allowance, making it difficult for the government to push it through.

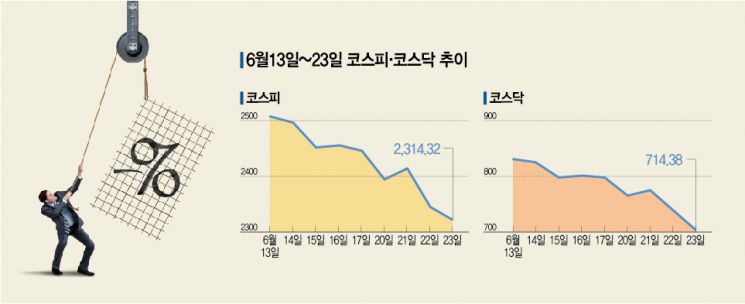

The KOSPI rose from 3,127.20 on May 3, 2022, when partial resumption of short selling was implemented, to 3,305.21 on July 6 of the same year, but then fell about 25% from its peak. There are concerns that short selling could cause further declines during periods of increased market volatility. As the domestic stock market faltered, panic selling occurred, sharply freezing investor sentiment. Considering the significant macroeconomic concerns, the financial investment industry views full resumption of short selling in the short term as unlikely.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}