[Asia Economy Reporter Lee Seon-ae] Since the full onset of COVID-19 in 2020, foreign investors have been relentlessly selling off Korean stocks for two and a half years. Moreover, the scale of net selling surpasses the net buying volume accumulated over the past decade. This is why the phrase "Frenzied Sell-Korea" has become a popular joke. However, it is reassuring that in most sectors, foreign investors are reducing their stakes primarily in leading stocks. This suggests that rather than turning their backs on the Korean market, they are likely engaging in asset allocation strategies for risk management. It implies that foreign investors' return can be expected once macroeconomic conditions such as interest rates and exchange rates recover.

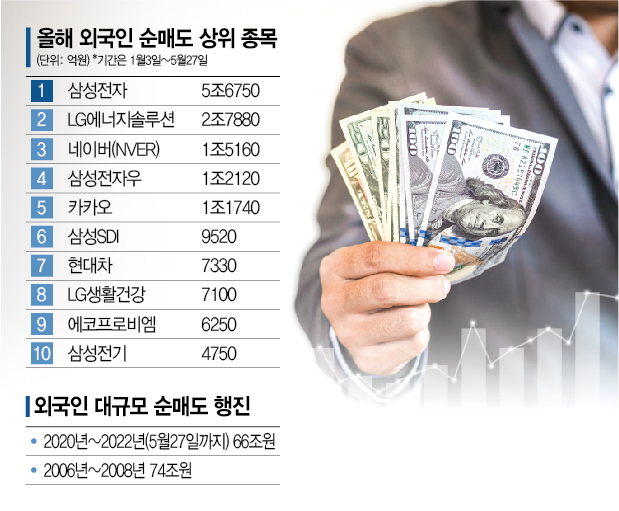

According to the Korea Exchange on the 30th, from January 2, 2020, to last Friday the 27th, foreign investors' net selling amounted to 66.0544 trillion KRW. Compared to the approximately 52 trillion KRW net buying over the previous 10 years before this net selling streak, this represents a sell-off exceeding that volume. A simple calculation shows that stocks accumulated over 10 years were sold off in just two years. Notably, the 66 trillion KRW scale is comparable to the sell-off during the financial crisis. Foreign investors sold off 74 trillion KRW worth of stocks from 2006 until the onset of the financial crisis in 2008.

The proportion of foreign investors in the Korean stock market has also sharply declined. According to the Financial Supervisory Service, as of last month, the balance of foreign investors' holdings in listed stocks was 696.222 trillion KRW, dropping to 26.7% of the market capitalization. This is the lowest level in about 13 years since May 2009 (26.5%) during the global financial crisis. After the global financial crisis, the foreign investors' share of listed stocks consistently stayed in the 30% range. It even peaked at 33.9% in October 2017. However, since June last year (29.9%) during the height of COVID-19, it fell below 30% again and has continued to decline. Samsung Securities researcher Seo Jeong-hoon noted, "The scale of foreign investors' selling since 2019 is similar to selling off all the net purchases accumulated since the financial crisis, resulting in the lowest foreign investor share in 10 years."

However, the current foreign investors' sell-off in Korea is viewed by the financial investment industry as largely an asset allocation strategy. It does not mean they have turned their backs on the Korean stock market but rather that they are reducing stakes across emerging markets as part of risk management. In fact, foreign investors are reducing their holdings centered on leading stocks across sectors, focusing simply on reducing risk assets.

According to FnGuide, since June 2021, the stock with the largest decrease in foreign ownership is Asiana Airlines (Transportation). Its foreign ownership dropped from 20.75% in June 2021 by 13.14% to just 7.61% currently. Following are Zinus (Construction & Architecture), POSCO International (Trading & Capital Goods), CJ Logistics (Transportation), OCI (Chemicals), and HMM (Transportation). Foreign ownership in Zinus and POSCO International decreased by 4.74% and 3.76%, respectively, now standing at 18.59% and 7.72%. Next are Samsung Electronics (Semiconductors), NH Investment & Securities (Securities), Shinsegae (Retail & Distribution), KCC (Construction & Architecture), Hyundai Motor (Automobiles), and GKL (Hotel & Leisure).

Looking at the top stocks net sold by foreign investors this year up to the 27th, they are mainly large-cap stocks. Samsung Electronics, ranked first, combined with Samsung Electronics Preferred shares ranked fourth, amounts to a net selling of 6.8865 trillion KRW. The second-ranked LG Energy Solution's net selling is 2.7883 trillion KRW. Their combined net selling accounts for 62.7% of the total 15.4229 trillion KRW. This indicates that foreign investors chose stocks with high ownership stakes to reduce their holdings in the Korean market.

The top net sold stocks are also sector leaders. Following Samsung Electronics and LG Energy Solution, third is Naver (NVER). Then come Samsung Electronics Preferred, Kakao, Samsung SDI, Hyundai Motor, LG Household & Health Care, EcoPro BM, Samsung Electro-Mechanics, KakaoBank, LG Electronics, Amorepacific, Pearl Abyss, and NCSoft. As of the 27th, foreign ownership in Samsung Electronics fell to 50.6%, the lowest in five years since May 22, 2017 (50.5%). Naver (53.63% on the 27th, 53.61% on the 26th) and Kakao (28.49% on the 27th) also have foreign ownership at the lowest levels since COVID-19. LG Energy Solution even dropped to the 2% range for the first time since its mid-month listing.

However, the securities industry holds an optimistic view that foreign investors' demand will improve, allowing for a gradual return. This is based on the global financial market showing relief rallies, the dollar's strength easing, and the undervaluation appeal of the domestic stock market becoming more prominent. Cape Investment & Securities researcher Na Jeong-hwan said, "The slight decline in the won-dollar exchange rate is creating a favorable environment for foreign investors, which is positive."

SK Securities cited the preference for risk assets within the financial market and exchange gains (won appreciation) as conditions for foreign investors' return. Since the Korean market is not a main market for global investors, macro factors are more important than specific profits or business conditions. SK Securities researcher Ahn Young-jin said, "In an environment of rising interest rates, liquidity tightening, and war, where risk asset investment is avoided, it is difficult for foreign investors to focus on the Korean market, causing the ownership ratio to fall below 30%, the lowest since 2009. Although it is difficult to think that foreign investors will return in a trend, the historically low ownership ratio and the current won-dollar exchange rate below 1,300 may paradoxically encourage foreign investors' entry." He added, "Ultimately, the key is the revival of risk asset preference, which could be triggered by the easing of China's lockdowns, the end of the interest rate hike trend, and the Federal Reserve's signals to slow down."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}