"Bond Yields Peak in Q2... 10-Year Bonds Expected at 3.26%"

Short-Term Volatility Hedge Strategy Recommended

Biggest Variable: Bank of Korea's 'Big Step'

If Big Step Materializes, Bond Yields May Rise by 20bp

War and Fiscal Reinforcement Policy Noncompliance Also Variables

[Asia Economy Reporter Hwang Yoon-joo] There is a forecast that bond investment sentiment will recover after August. Although inflation is currently a significant issue, it is explained that from mid-3rd quarter onwards, the market focus will shift to growth slowdown, entering a stabilization phase.

Kim Sang-hoon, a researcher at Hana Financial Investment, stated on the 23rd, "Considering the medium-term fiscal soundness strengthening policy of the new government, the peak of demand-side inflation, and entering the latter phase of interest rate hikes, we recommend a preemptive response focused on long-term bonds." In the short term, he recommended a volatility hedge strategy due to uncertainties in the US-Korea base interest rate hike path.

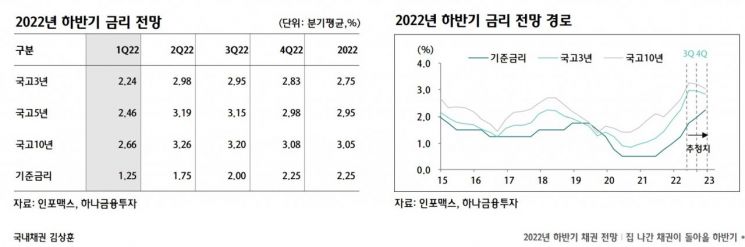

Researcher Kim predicted that the 2nd quarter of this year would be the peak for government bond yields. He expected 3-year bonds at 2.98%, 5-year bonds at 3.19%, and 10-year bonds at 3.26%, forecasting that the lower bound of interest rates would gradually decrease from the 3rd quarter.

He explained, "From the base interest rate exceeding 1.75%, the proportion of net interest burden relative to consumption surpasses the previous peak, which is expected to negatively impact household consumption," adding, "Additional hikes by the central bank to curb inflation are expected to weaken demand-side inflationary pressures after the summer vacation season."

Accordingly, domestic consumer prices are expected to reach their peak during the 3rd quarter. Domestic inflation has exceeded 3% for a prolonged period on four occasions. Researcher Kim analyzed, "It took an average of 9 months from exceeding 3% to reaching the peak," and "Considering the time lag, the core inflation peak and broad inflationary pressures will reach their peak in the 4th quarter to year-end."

He further diagnosed, "Since the root cause of the prolonged bond bear market was inflation, the economic slowdown due to consumption constraints will gradually reduce sensitivity to inflation, which is expected to lead to capital inflows into the bond market."

However, he noted that variables remain, such as △ the Bank of Korea's 'Big Step' (raising the base interest rate by 50 basis points at once), △ geopolitical risks, and △ changes in the new government's fiscal policy stance.

Researcher Kim pointed out, "The Bank of Korea's Big Step raises expectations for the terminal interest rate and is a factor that could push bond yields about 20 basis points higher than the previous peak." He added, "If geopolitical risks reoccur, crude oil and food prices could surge, raising overall inflation, and if the fiscal soundness strengthening policy is not maintained, bond yields could rise further."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}