Record High Interest Income Due to Suppressed Bad Debt Costs in Special Environment

Profit Growth Rate Expected to Slow After End of COVID-19 Financial Support

[Asia Economy Reporter Minwoo Lee] Due to the global trend of interest rate hikes following the U.S.'s tightening measures, banks' interest income is surging. Since this performance improvement is a result of suppressed loan loss costs due to the government's COVID-19 financial support measures, it is expected that the current upward trend will slow down once the policy support ends.

On the 21st, Hana Financial Investment made this forecast regarding the future performance of the banking sector. Amid high inflation caused by Russia's invasion of Ukraine, China's strengthened COVID-19 prevention measures, and global supply chain disruptions, interest rates worldwide are rising sharply as the U.S. embarks on full-scale tightening. Due to the interest rate-sensitive asset-liability structure of banks, rising interest rates primarily improve the net interest margin (NIM), resulting in a rapid increase in banks' interest income.

In fact, banks' NIM has accelerated since the global interest rate began rising early last year. It increased by 4 basis points (bp; 1bp = 0.01%) annually last year alone and rose by 5bp in the first quarter of this year. It is expected to increase by more than 7bp in the second quarter as well. Since the U.S. Federal Reserve is expected to continue 'big steps' of raising interest rates by 0.5 percentage points at a time for a while, domestic benchmark interest rates are also anticipated to rise further. Jungwook Choi, a researcher at Hana Financial Investment, analyzed, "The upward trend in banks' NIM is likely to continue for the time being," adding, "The annual NIM is expected to rise by more than 16bp this year."

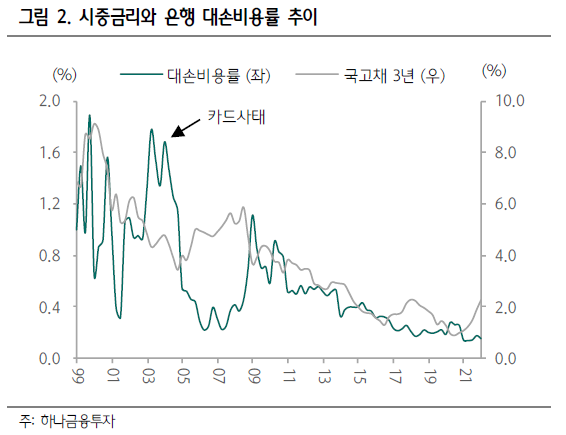

Along with this, banks' loan loss cost ratios have continued to decline. Typically, when interest rates rise, borrowers' interest burdens increase, leading to higher loan loss costs, but this trend has been quite different. Researcher Choi explained, "While factors such as the previously very low interest rates, banks' efforts to change their loan portfolios, and improvements in borrowers' credit ratings have played a role, the government's COVID-19 financial support measures, including loan maturity extensions and interest repayment deferrals for small and medium-sized enterprises and small business owners, were also significant factors," adding, "Since these policies are likely to end around September, it will be difficult for the situation of suppressed loan loss costs and sharply increased interest income to continue."

Therefore, it is forecasted that the growth rate of banks' profits will slow down considerably starting next year. This is because the rate of NIM increase is expected to decelerate and loan loss costs will gradually begin to rise. Researcher Choi predicted, "Considering that it will be somewhat difficult to freely implement capital efficiency policies such as dividend expansions, banks' return on equity (ROE) is expected to turn downward next year."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}