Contraction Resumes Since August 2020 Due to Lockdowns in Major Cities Including Shanghai

Infrastructure Investment Soars Thanks to Special Bond Issuance

[Asia Economy Beijing=Special Correspondent Jo Young-shin] China's retail sales (domestic demand) recorded negative growth. It is the first time since August 2020 that the domestic sales growth rate has turned negative. Consumption appears to have sharply cooled due to overlapping lockdown measures caused by the resurgence of COVID-19 and the Russia-Ukraine war. A red light has turned on for the Chinese leadership's economic growth target of 'around 5.5%' this year.

China's National Bureau of Statistics announced on the 18th that the first quarter gross domestic product (GDP) increased by 4.8% compared to the same period last year. This is far below China's growth target of around 5.5% for this year.

Red light on China's growth engine

China's economic growth rate in the first quarter this year was only 4.8% compared to the same period last year. Internally, China considers a growth rate above 5% as a sign that the economy is doing well. Growth above 5.5% means the Chinese economy is strong. Conversely, below 5% is regarded as unfavorable.

Although higher than the 4.2?4.5% forecast by Bloomberg and Chinese economic media Caixin, it is still below the psychological benchmark of 5%. It is also 0.7 percentage points lower than the Chinese government's target of around 5.5% this year.

The problem lies in the second quarter. Internally, there is the challenge of controlling the large-scale spread of COVID-19, and externally, the difficulties of the Russia-Ukraine war and US-China conflicts are faced.

China's economy stuck in the 'zero (0)' swamp

What has held back China's economy is domestic demand. China was the first among major countries to emerge from the pandemic shock, thanks to its strong quarantine policy symbolized by 'Zero COVID.' Ironically, this time, China's quarantine policy has become a hindrance.

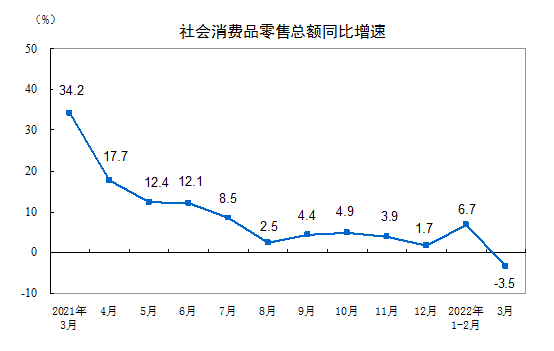

In fact, China's retail sales showed a negative (-) 3.5% compared to the same month last year. The 6.7% increase over January and February helped limit the decline. The retail sales growth rate peaked at 34.2% in March last year and fell to 1.7% in December last year. China's retail sales dropped to minus 20.5% in January and February 2020 when COVID-19 was rampant. After seven months of negative retail sales, it turned positive in August (0.5%). Following the Chinese government's de facto declaration of the end of COVID-19, the retail sales growth rate rose to 34.2% in March last year. Retail sales growth slowed again due to coal shortages caused by rising international raw material prices last year, and in December last year, it only grew by 1.7%.

Domestic demand is a major foundation of China's economic growth. Last year, domestic demand contributed 65.4% to China's GDP. Domestic demand is a barometer of the Chinese economy. There are concerns that lockdown policies reduce income for small business owners and workers, dampening consumption vitality. Industrial production also took a direct hit from the COVID-19 resurgence in March. Industrial production announced on this day was recorded at 5%. Industrial production seemed to recover from the shock of rising international raw material prices with a 7.5% increase in January and February but was hampered by the epidemic.

The dilemma of the Chinese economy

China's central bank, the People's Bank of China, cut the reserve requirement ratio (RRR) by 0.25 percentage points on the 15th. This preemptive RRR cut was made due to concerns about downward pressure on the economy, especially consumption contraction caused by lockdowns. It is the first cut in four months since a 0.5 percentage point cut in December last year. The 0.25 percentage point cut is expected to inject 530 billion yuan (about 102 trillion won) of liquidity into the market.

The problem is that even if money is released into the market, the consumers who would spend it are confined at home. Also, with the flood of special bonds issued by local governments, a considerable amount of funds has already been released into the market. The scale of new yuan loans in the first quarter was 8.34 trillion yuan (1,616.3 trillion won), an increase of 663.6 billion yuan compared to the same period last year. This is the largest increase on record for the first quarter. As of the end of March, the M2 (broad money supply) balance, which indicates cash liquidity released into the market, reached 249.77 trillion yuan (48,411 trillion won), up 9.7% from the same period last year.

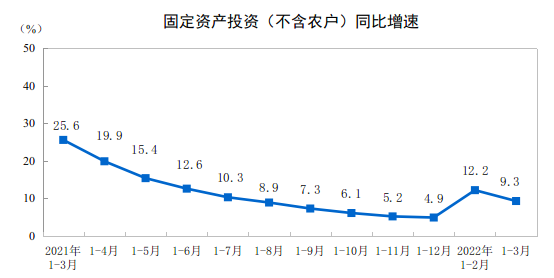

In fact, fixed asset (infrastructure) investment in China in the first quarter increased by 9.3% compared to the same period last year. By industry, primary industry increased by 6.8%, secondary industry by 16.1%, and tertiary industry by 6.4%, indicating that a considerable amount of money was used for economic stimulus.

Since the Chinese government is maintaining the existing Zero COVID quarantine policy of lockdowns, there is a high possibility that money will be released into the market but will not connect to consumption. The Chinese economy cannot be supported by online clicks alone. With the 20th Party Congress scheduled for this fall, the Chinese leadership's concerns are expected to deepen further.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}