Overlap of Jeonse Loan Support Expansion and Jeonse Price Increase Period

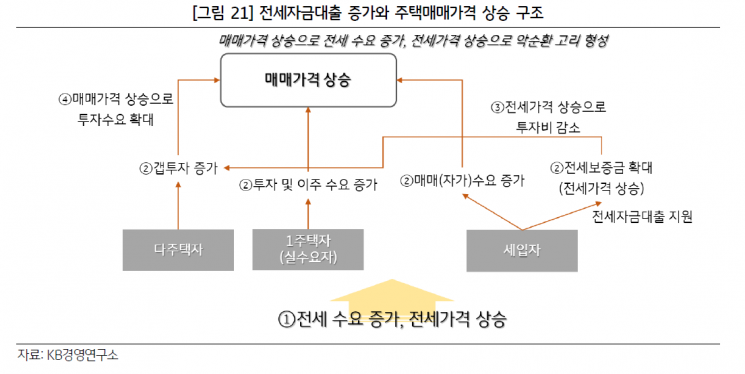

Rise in Gap Investments Influences Housing and Jeonse Prices

Need for Rational Management Measures Supporting Actual Demand

[Asia Economy Reporter Minwoo Lee] While jeonse loan has been used as a means to stabilize housing for low-income households, it is also analyzed to have acted as a factor driving up jeonse prices. It not only created a favorable environment for gap investment, which involves purchasing homes with jeonse deposits, but also likely served as an investment tool for homeowners residing in jeonse.

On the 10th, KB Financial Group Management Research Institute published a report titled "Review of Market Changes Due to the Increase in Jeonse Loans," containing these findings.

The report analyzed that although the jeonse market is influenced by various factors including supply, the increase in jeonse loans likely had a direct and indirect impact on the rise of jeonse prices and housing prices.

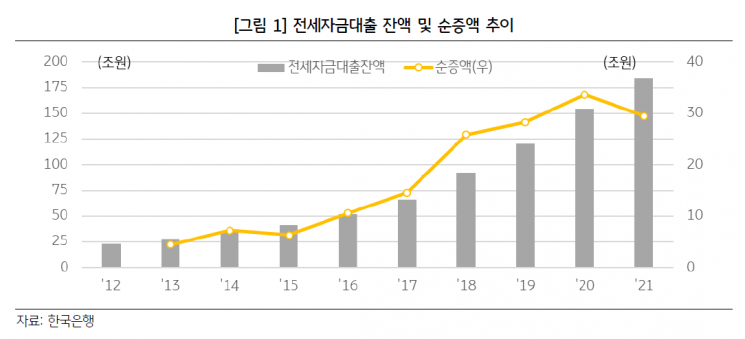

Recently, jeonse loans have been rapidly increasing in a short period. The outstanding balance of jeonse loans was only about 23 trillion won in 2012 but surged sharply after 2016. It exceeded 100 trillion won in 2019 and reached 180 trillion won by the end of last year.

During this period, various supports for jeonse loans also began to expand. From 2010 to 2013, various support measures were implemented, such as raising guarantees by the Housing Finance Credit Guarantee Fund and relaxing recognized income conditions, to ensure housing stability. Although support was limited mainly for high-value loans due to concerns that jeonse loans might cause housing price increases, the support began to expand rapidly from 2015, focusing on private guarantees.

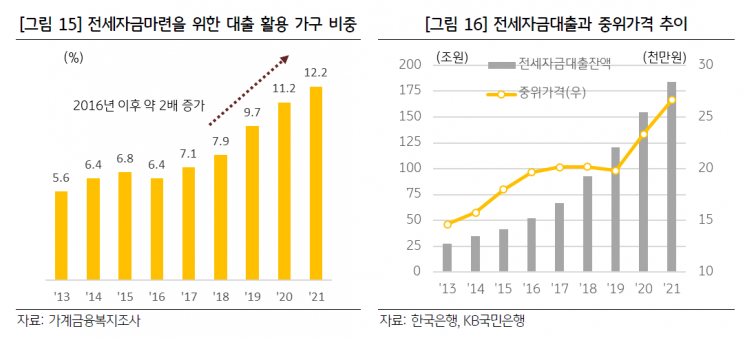

Low interest rates and expanded limits on jeonse loans were used as means for monthly rent residents to switch to jeonse demand and for jeonse residents hoping to move to better places to secure funds. The proportion of households taking loans to prepare jeonse funds increased more than twofold from 5.6% in 2013 to 12.2% last year, especially rising sharply since 2016.

Although the burden on tenants inevitably increased as jeonse prices rose, jeonse loans alleviated tenants' loan burdens, acting as a factor in the rise of jeonse prices. Both the number of households needing jeonse loans and the required amounts increased as jeonse prices went up. KB Financial Group Management Research Institute explained, "Even during periods when jeonse loans were not widespread, jeonse price growth rates were high, but easier access to jeonse loans likely amplified the increase. Also, even though tenants moving to better facilities or closer to work might face higher housing costs, the availability of jeonse loans probably helped with housing relocation."

This trend led to an increase in the proportion of monthly rent households. Especially since 2018, the proportion of households converting part of the jeonse price increase into monthly rent because they could not cover the rise with jeonse loans has significantly increased. The decrease in pure jeonse and the conversion of part of the deposit into monthly rent were more pronounced in the top 20% income quintile based on jeonse prices. In Seoul rental transactions, the decline in pure jeonse transactions was faster for jeonse homes in the top 20% quintile, and the proportion of transactions with 40% deposit converted to monthly rent rose sharply.

Jeonse loans were also used as funds for home purchases, stimulating buying demand and causing housing prices to rise. KB Financial Group Management Research Institute analyzed, "Multi-homeowners found gap investment advantageous as sales prices and jeonse prices converged, and actual demanders could purchase homes for replacement or investment purposes. Tenants had the capacity to increase deposits through jeonse loans, and on the other hand, the number of households switching to purchase demand due to higher jeonse qualifications increased."

Ultimately, jeonse loans are a very useful loan tool for low-income households but require rational management. KB Financial Group Management Research Institute emphasized, "Jeonse loans play an important role in stabilizing housing for low-income households, but contrary to the original purpose, it is necessary to minimize liquidity increases and side effects caused by excessive loans. Rather than regulating jeonse loans, it is important to guide loans rationally through the market's autonomous functions while expanding support for housing-vulnerable groups."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}