The Largest Copper Processing Company in Korea

Record High Operating Profit of 314.1 Billion KRW Last Year

Copper Price per Ton Up $3,000 in One Year

Over One Year’s Worth of Raw Material Inventory

Bullet Also Expects Increased International Demand

[Asia Economy Reporter Park Jihwan] Pungsan is not a widely known company to the public, but it is regarded as the largest copper processing company in Korea, boasting solid performance by manufacturing ‘coins’ and ‘bullets.’ Last year, its main product, copper processed goods, enjoyed a significant increase in demand and price due to the global economic recovery, achieving the highest-ever operating profit. This year, it is analyzed that solid performance will continue due to increased demand in core businesses such as copper processing and military ammunition.

Pungsan started in 1968 as Pungsan Metal Industry Co., Ltd. and has built technological expertise in the non-ferrous metal materials industry for over 50 years. In 2000, the second son, Chairman Ryu Jin, succeeded his father and founder, Chairman Ryu Chan-woo, and has been leading the company for more than 20 years. Pungsan’s business structure is broadly divided into the ‘non-ferrous business,’ which produces copper and copper alloy products, and the ‘defense business,’ which manufactures various types of ammunition.

Sales are composed of 74.2% from the non-ferrous business and 25.8% from the defense business. In the non-ferrous segment, copper (electrolytic copper) supplied from companies such as LS Nikko Copper is processed into metal plates, rods, wires, and coins. The defense business produces various military ammunition ranging from 5.56mm small-caliber bullets to 155mm howitzer shells, as well as sports ammunition, propellant explosives, and ammunition components.

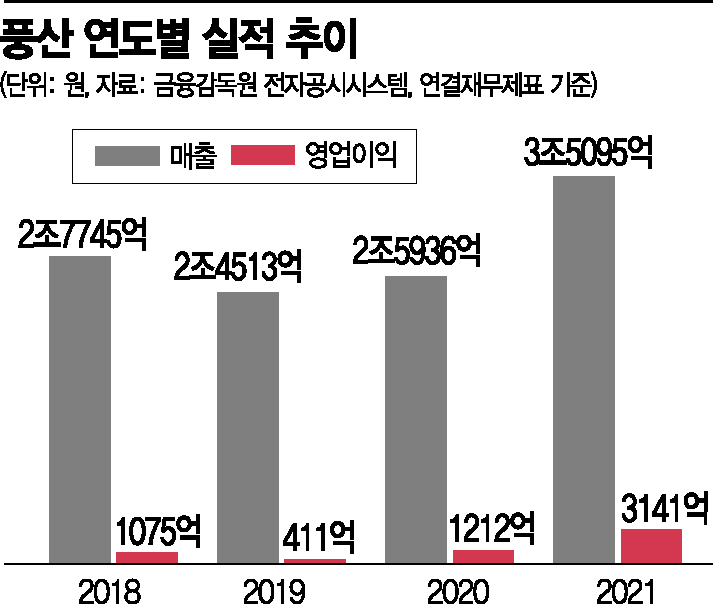

Pungsan recorded its best performance since its establishment last year. On a consolidated basis, operating profit rose 159.2% year-on-year to 314.1 billion KRW. During the same period, sales increased by 35.3% to 3.5095 trillion KRW. Pungsan’s performance is determined by inventory asset valuation gains and the ‘roll margin,’ which is the price difference between products and raw materials per unit weight. When the price of the main raw material, electrolytic copper, rises, the increase in product prices compared to raw material purchase costs improves operating results.

According to the London Metal Exchange (LME), the price of electrolytic copper, which was in the high $7,000s per ton in January last year, has now surpassed $10,000, reaching an all-time high. Additionally, Pungsan stocks over a year’s worth of inventory for product processing, so when copper prices rise, the inventory asset valuation gains directly add to operating profit.

Copper prices are expected to remain at high levels for the time being. Baek Jae-seung, a researcher at Samsung Securities, said, “Due to the expansion of electric vehicles and infrastructure investment, copper demand is expected to maintain a favorable trend this year as well,” adding, “The recovery speed of copper supply is still not fast due to the spread of Omicron, so copper prices will show a solid trend above $9,000.” Another source of revenue for Pungsan, bullet sales, is also expected to increase due to rising military tensions in the Russia-Ukraine region and the Middle East. Lee Hyun-soo, a researcher at Yuanta Securities, said, “Last year, defense sales increased by 5% year-on-year despite a decline in domestic sales, thanks to strong exports,” and forecasted, “This year, exports of ammunition to the U.S. and the Middle East will remain solid, and domestic sales may also increase.”

There is some concern that the growth rate of this year’s performance may slow down. According to financial information provider FnGuide, securities analysts forecast Pungsan’s sales this year at 3.7307 trillion KRW and operating profit at 228.5 billion KRW. While the sales forecast is 6.3% higher than last year, operating profit is expected to decrease by 27.3%. Even if copper prices remain high, the rise is expected to be smaller, reducing inventory asset valuation gains. However, compared to the usual operating profit level in the 100 billion KRW range, it is still evaluated that Pungsan will maintain more than double the strong performance.

The securities industry anticipates further upside potential for Pungsan’s stock price. The current average target price set by securities firms for Pungsan is 45,000 KRW. Based on the previous trading day’s closing price of 34,300 KRW, there is a 31.2% upside potential. Lee Kyu-ik, a researcher at Cape Investment & Securities, said, “As of the end of last month, Pungsan’s 12-month forward price-to-book ratio (PBR) was about 0.48 times. Considering that copper prices and non-ferrous sales volume are likely to remain favorable this year, Pungsan’s current stock price level is judged to be undervalued.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}