6 Saemaeul Geumgo Credit Unions Offer 1% Credit Loans to High Credit Borrowers

Cheaper Than 5 Major Banks' Loan Rates of 3.42~3.78%

Financial Authorities: "Mutual Finance Effective in Serving High Credit Borrowers"

Industry: "Interest Rate Inversion Due to Government and Financial Authorities' Regulations"

Using Secondary Financial Institutions Despite Low Rates Inevitably Lowers Credit Scores

Seong Chan-ho (38, pseudonym), who lives in Dongducheon, Gyeonggi Province, recently decided to take out a loan of 20 million KRW to prepare moving funds. While looking for a personal loan product, he found out that a local Saemaeul Geumgo offered loans at an interest rate in the 2% range. Seong said, "Although it belongs to the secondary financial sector, the interest rate is about 3 percentage points lower than that of commercial banks, significantly reducing the interest burden," adding, "I heard that my credit score might drop after taking the loan, so I'm worried whether it's okay to proceed."

As the base interest rate continues to rise, causing loan interest rates at private banks to increase, a paradoxical phenomenon is occurring where high-credit borrowers in need of loans are turning to the secondary financial sector. This 'loan interest rate inversion' caused by government and financial authorities' regulations has continued into the beginning of the year. Some mutual finance institutions have even been offering ultra-low interest personal loans, which are rarely seen, to meet this demand.

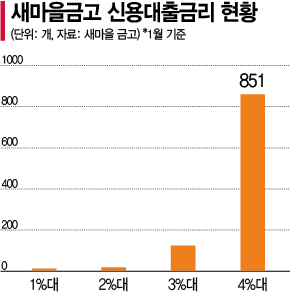

On the 15th, Asia Economy reviewed the loan interest rates by credit rating for all 1,297 Saemaeul Geumgo nationwide and found that as of the end of last month, 991 Geumgo had issued loans to high-credit borrowers with credit ratings from 1 to 3. Among them, six Geumgo offered ultra-low interest personal loans in the 1% range. The five major banks?KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup?offered personal loans to 1st and 2nd grade high-credit borrowers last month at interest rates ranging from 3.42% to 3.78%. This means that Saemaeul Geumgo, part of the secondary financial sector, provided loans more than 2 percentage points cheaper than the primary financial sector.

The Saemaeul Geumgo with the lowest interest rate was Hwagog Geumgo, where the average personal loan interest rate for high-credit borrowers with grades 1 to 3 was 1.38%. It was followed by Sangok 2 and 4-dong Geumgo at 1.48%, Kumho (1.55%), Sejong (1.73%), Uijeongbu Singok (1.77%), and Yongdu (1.87%). Among these, only Sejong Geumgo was a workplace Geumgo, while the other five were all regional Geumgo.

There were 16 Geumgo that provided personal loans in the 2% range, classified as low interest. Additionally, 118 Geumgo offered loans in the 3% range, similar to commercial banks.

Even with Lower Interest Rates in Secondary Financial Sector, Credit Score Decline Is Inevitable

It is contrary to the usual financial order that loan interest rates in the secondary financial sector are lower than those of commercial banks. Commercial banks, which belong to the primary financial sector, have many ways to raise funds cheaply, such as issuing bonds, due to their high credit ratings, and have lower default costs, allowing them to maintain low loan interest rates. On the other hand, the secondary financial sector relies almost exclusively on deposits as a funding source and suffers from many defaults, so their interest rates are generally higher than those of the primary financial sector.

This financial distortion phenomenon is observed throughout the mutual finance sector. According to the Bank of Korea, the average personal loan interest rate in the mutual finance sector at the end of last year was 4.30%, which was 0.82 percentage points lower than the 5.12% in commercial banks. Over the past three years, loan interest rates in the mutual finance sector were about 0.2 to 0.6 percentage points higher than those of commercial banks, but since the second half of last year, the inverted interest rates have continued.

The financial authorities have cited 'abundant liquidity,' 'narrowing funding cost gaps,' and 'regulatory easing for the secondary financial sector' as causes of the interest rate inversion phenomenon. At the end of last year, the Financial Services Commission released an explanatory document stating, "(The interest rate inversion phenomenon) has continued since the beginning of the year and is unlikely to be the result of recent total debt management," and claimed, "It is essentially due to the active marketing of mutual finance institutions targeting high-credit borrowers similar to banks."

However, industry insiders believe that the ongoing interest rate inversion phenomenon is closely related to government and financial authorities' regulations. A mutual finance sector official explained, "Since mutual finance is part of the secondary financial sector, it is natural for funding costs and loan interest rates to be high," adding, "As household loans at commercial banks exploded, regulations began, and there was a significant aspect of adjusting interest rates to reduce loan demand in the primary financial sector."

However, many caution that just because loan interest rates are low, blindly turning to the secondary financial sector is risky. This is because taking out a loan in the secondary financial sector can cause a drop in credit score. In such cases, borrowers may face disadvantages in interest rates and loan limits when applying for additional loans from other financial institutions.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}