[Asia Economy Reporter Lee Seon-ae] Attention is focused on the impact of the government's strengthened regulations on money market funds (MMFs) (conditional market valuation and changes to the weighted average remaining maturity). The introduction of the market valuation system for MMFs is expected to suppress large-scale redemptions and stabilize the short-term financial market, but concerns are widespread that market contraction is inevitable and will trigger a negative chain reaction on liquidity supply.

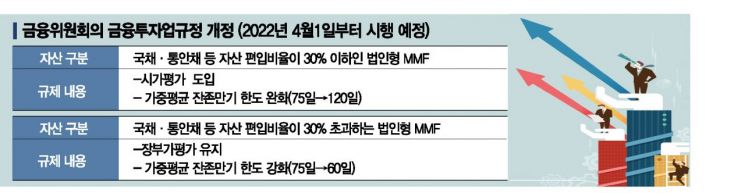

According to the financial investment industry on the 20th, the market valuation system for MMFs will be implemented on April 1 next year. Following the Financial Services Commission's amendment to the Financial Investment Business Regulations on March 18, 2020, the market valuation method will be introduced for corporate MMFs with a relatively low proportion (30% or less) of stable assets such as government bonds and monetary stabilization bonds. However, as risk management is strengthened through market valuation, the weighted average remaining maturity limit will be relaxed from the current 75 days to 120 days. Corporate MMFs with an asset composition exceeding 30% in government bonds and monetary stabilization bonds will maintain the current book value evaluation method, but since the book value method has limitations in timely reflecting risks, the weighted average remaining maturity regulation will be tightened from 75 days to 60 days.

Under the current standards, MMF base prices are evaluated at book value, creating an incentive for "pre-redemption gains" where investors redeem before the price reflects potential asset deterioration. Corporate MMFs, which are sensitive to market fluctuations, are particularly vulnerable to large-scale redemptions. For example, in 2018, when concerns about the default of Qatar National Bank (QNB) term deposits and ABCP arose, a large-scale MMF redemption crisis occurred. Additionally, in March 2020, when the stock market plunged sharply, a surge in MMF redemptions triggered liquidity concerns. The financial authorities view conditional market valuation as a way to curb mass redemptions.

However, experts worry about market contraction. Kim Sang-hoon, a researcher at Shinhan Financial Investment, said, "The series of MMF regulatory enhancements, including market valuation and redemption restrictions, aim to stabilize the short-term financial market, but they may also cause the MMF market to shrink due to reduced attractiveness of MMF products." He emphasized, "Especially, the contraction of the MMF market could negatively affect liquidity supply in the short-term financial market, such as commercial paper, so regulatory strengthening should be approached cautiously."

In fact, MMFs play a major role as fund suppliers in the short-term financial market, so changes in deposit size and investment methods significantly impact the short-term financial market. This is because MMFs have limited asset types (bonds, repurchase agreements, certificates of deposit, commercial paper, etc.) and maturities, resulting in a relatively high proportion of short-term financial products compared to other collective investment products.

In reality, a significant portion of funds for reinvestment after profit-taking in a rising stock market and standby funds that hold off investing during volatile markets tend to flow into MMFs. This characteristic was even more pronounced this year. From June to early July, as the KOSPI continued its upward trend and reached a high of 3305.21, MMF net assets decreased to 142 trillion won. Subsequently, as profit-taking and cautious sentiment emerged, MMF net assets increased to 189 trillion won by early August. Thus, funds moved into MMFs according to stock index trends, supplying liquidity to the short-term funds market.

Accordingly, the financial investment industry views some changes in market trends as inevitable once the MMF market valuation system is implemented. A bond researcher said, "Depending on operational performance and market conditions, if the corporate MMFs subject to market valuation do not generate returns from extended maturities that sufficiently offset principal losses during the investment period, the incentive to hold MMFs will decrease." He added, "In that case, if short-term funds are not sensitive to yield changes, they will move to government bond-type MMFs with no principal loss, but if investors are unwilling to accept low yields, they will seek other investment alternatives, causing the MMF market to shrink."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}