Five Major Commercial Banks to Close 131 Branches by February Next Year

Following 236 Closures Last Year, 229 More Shut This Year

[Asia Economy Reporter Jin-ho Kim] Woo Jong-young (55, pseudonym), a self-employed person in Tongyeong, Gyeongnam, visits the bank several times a day. Due to frequent cash transactions, he often goes to the bank to deposit money. Recently, Woo heard that his bank branch would be merged and closed. At first, he did not think much of it, but he was shocked when he saw the location of the merged branch. The notice stated that the merged branch would be set up in Geoje, a neighboring city. Since it takes at least 30 minutes by car, Woo decided to change his main bank.

The five major commercial banks (KB Kookmin, Shinhan, Woori, Hana, and NongHyup) will close more than 130 branches (including sub-branches) over the next three months. This is due to the increased normalization of non-face-to-face transactions after COVID-19 and active efforts to reduce overlapping branches for efficiency and cost savings. Although financial authorities have pressured banks to refrain from closures since the beginning of the year to protect vulnerable groups such as the elderly who have difficulty with non-face-to-face transactions, banks seem indifferent. The pace of branch closures is expected to accelerate further.

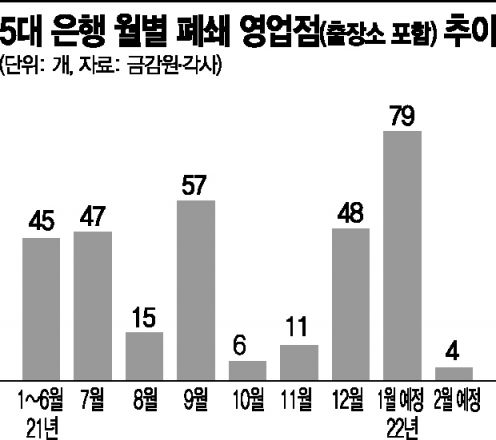

According to the financial sector on the 26th, the five major banks will close a total of 131 branches over the next three months until February next year. Starting with 48 branches next month, 79 branches will be merged in January, and 4 branches in February. Shinhan Bank will close the most branches, with a total of 47 closures. Following are Kookmin Bank (36 branches), Woori Bank (24 branches), Hana Bank (13 branches), and NongHyup Bank (11 branches), which will also reduce their branches in order.

In particular, Shinhan Bank will merge 42 branches at once on January 17 next year. Kookmin Bank and Woori Bank will also close 35 and 24 branches respectively on January 24 and February 30 in one go.

The pace of bank branch closures has been accelerating since last year. According to statistics from the Financial Supervisory Service, the number of branches of the five major banks decreased by 191 in 2017, then slowed to 27 in 2018 and 38 in 2019.

However, with the full onset of COVID-19 last year, the number sharply dropped by 236. This year, the trend is similar. Due to the financial authorities’ request for restraint at the beginning of the year, only 45 branches were closed in the first half, but 184 branches have closed or are scheduled to close in the second half. Combining the Financial Supervisory Service statistics and each bank’s announcements, about 804 branches have disappeared or will disappear over approximately five years from 2017 to February next year.

The main reason the major banks are actively slimming down branches is the spread of non-face-to-face transactions due to COVID-19, making mobile and internet banking routine. According to the Bank of Korea, as of the first half of this year, the proportion of bank counter services dropped to the 6% range, while internet banking usage rose to the 70% range. Additionally, with the prolonged low-interest-rate environment, banks are actively reducing overlapping branches to cut costs.

However, there are many concerns that rapid closures will cause financial exclusion for vulnerable groups such as the elderly. Although financial authorities have already made the branch closure process more stringent and urged restraint, the effect is said to be minimal. The Financial Labor Union held a press conference on the 25th of last month, stating, "Branch closures are banks neglecting their social responsibility toward financially marginalized groups," and urged, "Financial authorities must take active measures to ensure financial publicness and consumer protection."

Meanwhile, discussions on joint bank branches, which were suggested as an alternative to rapid bank closures, have practically subsided. It is known that some banks expressed skepticism about operating joint branches. While simple tasks such as deposits and withdrawals are not problematic, the distribution of profits from product acquisition and other revenue-generating activities is also cited as a cause.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}