'Loss Insurance' Real-World Insurance

Emergency Due to Accumulated Deficits... Discussion on Rate Increase at Month-End

Expansion of Non-Covered Medical Services

Some Consumers' Moral Hazard Is a Problem

Sharp Increase in Multifocal Lens Real-World Claims

Prices Vary Widely from 2.5 to 8.3 Million Won

1st and 2nd Generation Real-World Claims for Physical Therapy Rank First

Low Copayments Lead to Growing Deficits

Need for Incentives to Switch to 4th Generation Real-World Insurance

[Asia Economy Reporters Oh Hyung-gil and Ki Ha-young] Medical expense indemnity insurance premiums are expected to rise sharply again next year. This is due to the continuous deficit in indemnity insurance losses, which have reached 9 trillion won over the past four years. Unless structural issues such as establishing a non-reimbursable treatment management system are resolved, premium increases are inevitable, placing an increasing burden on policyholders.

According to the non-life insurance industry on the 25th, the loss amount for indemnity insurance by non-life insurers was tentatively estimated at 1.9696 trillion won through the third quarter of this year. This is a 10.4% increase compared to the 1.7838 trillion won loss during the same period last year.

Indemnity insurance covers the portion of medical expenses not covered by health insurance, reimbursing policyholders for actual costs. More than 39 million people, accounting for 75% of the entire population, are enrolled, earning it the nickname "the second health insurance."

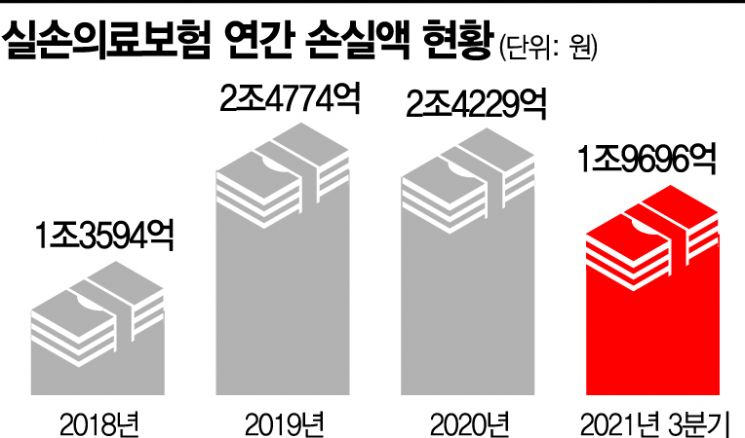

The problem lies in the moral hazard of some hospitals, clinics, and policyholders, leading to annual deficits in the trillions of won. The deficit in indemnity insurance, which was 1.3594 trillion won in 2018, surged to 2.4774 trillion won in 2019.

Last year, the deficit was 2.4229 trillion won, and this year it is approaching 2 trillion won as of September, expected to record the largest loss ever. Typically, losses increase in the fourth quarter, and considering the current upward trend and fourth-quarter projections, the non-life insurance industry's estimated indemnity insurance loss for this year is about 2.9 trillion won.

The loss amount refers to the difference between the "risk premium"?the insurance premiums paid by policyholders minus business management and operating costs?and the "incurred loss amount," which is the insurance payout. This means that the insurance payouts exceed the premiums collected, forcing insurers to bear the burden of covering these deficits.

The loss ratio, calculated by dividing the incurred loss amount by the risk premium, averages 131.0%. Older indemnity insurance products with no deductible and broader coverage showed higher ratios. The first-generation indemnity insurance sold until September 2009 had a loss ratio of 140.7% as of the end of September this year. Although a premium increase of up to 21.2% was implemented for first-generation products in April, the loss ratio remained similar to the previous year’s 141.7%.

The second-generation indemnity insurance (sold from October 2009 to March 2017), which accounts for 46% of all indemnity insurance, also had a loss ratio of 128.6%. The third-generation indemnity insurance (sold from April 2017 to June 2021) saw its loss ratio worsen from exceeding 100% in 2019 to 112.1% as of the end of September this year.

A high loss ratio means consumers pay lower premiums but receive more coverage, but the costs are inevitably passed on to those who do not receive coverage. This deteriorates the sustainability of insurance.

According to the insurance industry, among the 34.96 million indemnity insurance policyholders last year, 760,000 were high-amount claimants receiving over 10 million won, and 90,000 received over 50 million won. Conversely, 60% of all policyholders did not file a single claim.

The government, financial authorities, and the insurance industry plan to discuss the extent of indemnity insurance premium increases at the public-private insurance policy council at the end of this month. Once the council decides on the premium adjustment range and communicates it to insurers, the insurers will determine the increase rate accordingly.

An industry official said, "Although premiums were raised this year and the fourth-generation indemnity insurance was introduced, it is insufficient to prevent worsening loss ratios. Premiums will need to be raised to a higher level than this year."

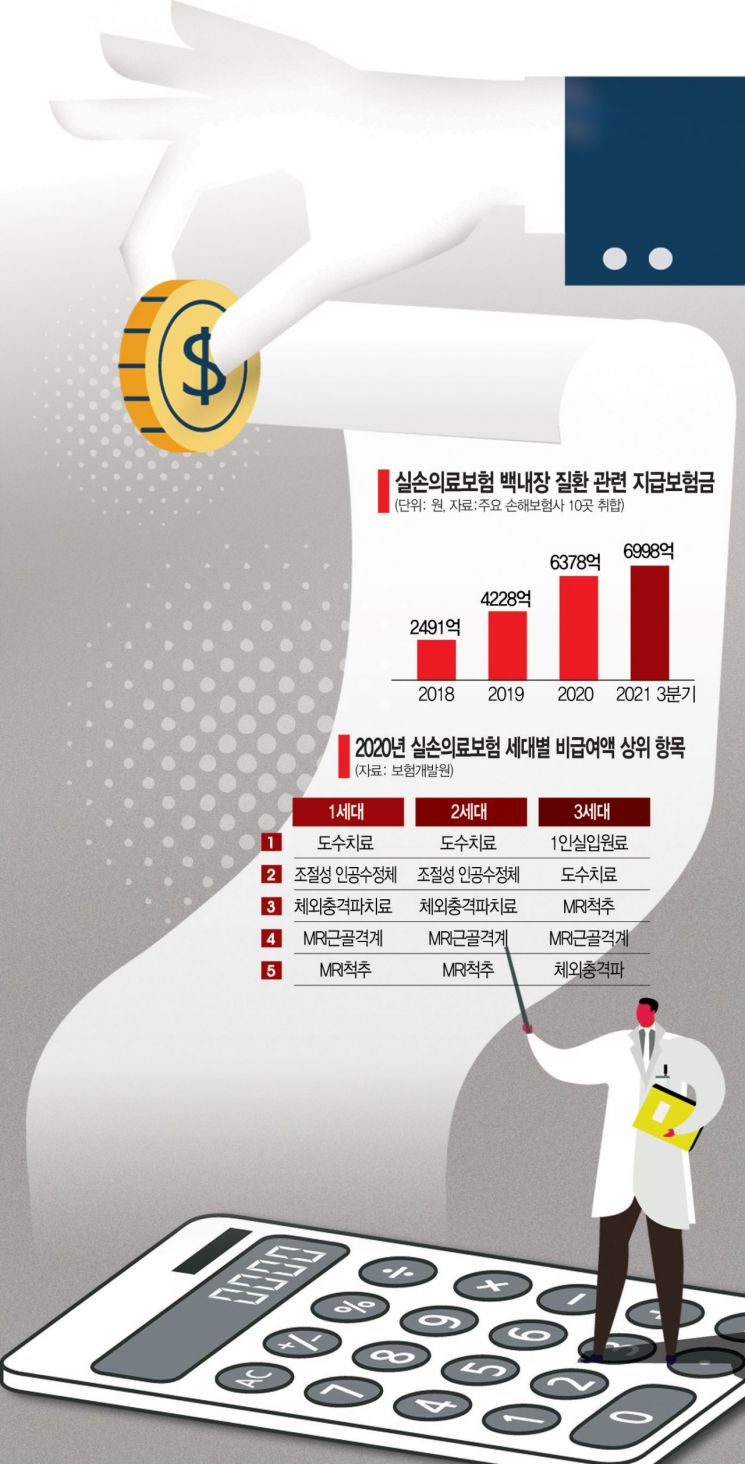

700 Billion Won in Cataract-Related Insurance Claims... Up to 8 Million Won Difference in Clinic-Level Treatment Costs

To improve the chronic deficit structure of indemnity medical insurance, strengthening the management of non-reimbursable treatments must be prioritized. Experts advise that issues such as the wildly varying prices of non-reimbursable items, exemplified by cataract surgery, need to be addressed first. Switching to the fourth-generation indemnity insurance launched this year, which reduces excessive medical use by a minority, is also considered a way to reduce indemnity insurance losses.

Recently, indemnity insurance payouts related to cataract diseases have sharply increased. As of the third quarter of this year, cataract-related insurance claims amounted to about 700 billion won, and if this trend continues, it is estimated to exceed 930 billion won by year-end. Among the proportions of non-reimbursable amounts by indemnity insurance product, the amount related to adjustable intraocular lenses (multifocal lenses) ranked second in first- and second-generation indemnity insurance.

The increase in cataract-related insurance claims is due to a surge in cases using expensive non-reimbursable multifocal lenses and claiming indemnity insurance. Accordingly, although the standard policy was revised in January 2016 to exclude coverage for multifocal lenses, after the revision, the price of multifocal lenses decreased while non-reimbursable examination fees rose sharply.

In fact, the average price per non-reimbursable examination was higher at clinics (260,000 won) than at tertiary general hospitals (80,000 won), and even within the same medical institution, price differences among clinics were severe.

In September last year, when non-reimbursable examination fees became reimbursable, the average indemnity insurance claim amount for multifocal lenses in contracts before January 2016, which allow claims for multifocal lenses, sharply increased. The average price of multifocal lenses, which had been around 2 million won in indemnity insurance claims, rose significantly to the high 3 million won range after September last year.

Conversely, non-reimbursable examination fees remained in the 400,000 to 600,000 won range until August last year but dropped to the 20,000 won range after becoming reimbursable in September. Even among clinics, multifocal lens prices vary drastically. Some clinics charged as low as 250,000 won, while others charged as high as 8.3 million won. The pattern of indemnity insurance claims related to cataract surgery has seen arbitrary and sharp fluctuations in non-reimbursable prices with each policy change, but the management system has not functioned properly.

Jung Sung-hee, a research fellow at the Korea Insurance Research Institute, advised, "Cost information on non-reimbursable items like multifocal lenses for cataract surgery should be investigated and disclosed to enhance public awareness, and socially agreed-upon guidelines for non-reimbursable prices and usage should be established."

Fourth-Generation Indemnity Insurance Launched in July... Consumers Shun It

The fourth-generation indemnity insurance, which began sales in July, is being shunned by consumers. It accounts for only 0.8% of all indemnity insurance contracts. There are calls for incentives to encourage switching to this product.

Sales of fourth-generation indemnity insurance by five non-life insurers?Samsung Fire & Marine Insurance, DB Insurance, Hyundai Marine & Fire Insurance, KB Insurance, and Meritz Fire & Marine Insurance?totaled 220,218 cases through the third quarter of this year. This is less than half the 553,394 cases sold in June, the month before the fourth-generation product was launched.

This indicates that consumers switched to the third-generation product instead of the fourth-generation, as encouraged by financial authorities. Especially in the first half of the year, many policyholders switched from the first and second generations to the third generation, resulting in lower-than-expected fourth-generation subscription rates.

The fourth-generation product features reduced premiums but higher deductibles for non-reimbursable items. Additionally, non-reimbursable items are separated into optional riders that must be purchased separately, and premium discounts or surcharges are applied based on the amount of non-reimbursable medical use.

While the first and second generations had little or no deductible, the fourth generation increased deductibles. Since premiums are surcharged for frequent hospital visitors, consumers perceive no benefit.

Although it is expected that the increased premium burden on old-generation policyholders will encourage switching to the fourth generation, there are also predictions that those with high medical usage will not switch.

An industry official said, "The fourth-generation indemnity insurance was introduced as a solution to the deficit structure, but it cannot yet be considered successful. Innovative alternatives, such as refunding premiums to policyholders who do not claim insurance, need to be considered."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}