Industry insiders expect launch as early as the first half of next year

Data accumulation anticipated to create synergy in credit operations

[Asia Economy Reporter Kiho Sung] Attention is focused on whether Toss Bank, the third internet-only bank in Korea, can emerge as a new credit card company after 20 years. Since Toss Bank expressed its intention to enter the credit card business at its launch, the industry expects that the "Toss Bank Credit Card" could become a reality as early as the first half of next year.

On the 25th, the Financial Services Commission began implementing the amendment to the Enforcement Decree of the Specialized Credit Finance Business Act from the 18th. This decree, reflecting suggestions from big tech companies, partially relaxes the entry requirements for credit card businesses established in July this year. The requirement for major shareholders’ equity capital to be at least four times the investment amount has been eased, and instead of separate financial requirements, only the "examination of whether the major shareholder is a distressed financial institution" is applied, allowing banks to operate credit card businesses.

Toss Bank has consistently expressed its intention to obtain credit card business approval since its inception. To this end, Toss Bank has been continuously recruiting credit card personnel since its launch last month. This will be the first time an internet-only bank enters the credit card business; among internet-only banks such as Kakao Bank and K Bank, none have yet obtained credit card business licenses.

Toss Bank’s entry into the credit card business aims to create synergy in credit operations. Toss’s operator, Viva Republica, owns various financial affiliates including electronic payment gateway (PG), banking, securities, and insurance, but has not yet ventured into the card business. Becoming a credit card company would allow the accumulation of vast payment data centered on customers and merchant infrastructure. Furthermore, with the full-scale launch of the Personal Credit Information Management Service (MyData) next month, card payment information can be big data-ized and analyzed. Based on this, Toss Bank could gain higher competitiveness in recommending customized financial products to customers.

Toss Bank’s strong performance in the check card segment is also significant. Check cards are considered a preliminary battleground in the war to secure credit card customers because they create a "lock-in effect" by binding customers. However, the issuance rate of check cards in Korea has been on a steady decline.

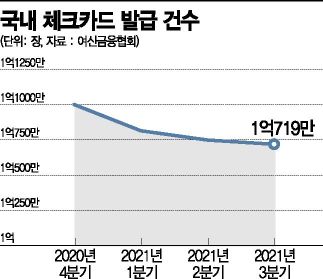

According to the Credit Finance Association, the total number of check cards issued domestically (including banks and card companies) increased from 110.01 million in the fourth quarter of last year to 108.15 million in the first quarter of this year. However, it decreased to 107.49 million and 107.19 million in the second and third quarters, respectively. In contrast, Toss Bank continues aggressive marketing through its check card, which offers a monthly cash rebate of 46,500 KRW.

However, there remains a burden that the card market has reached saturation, making further growth unlikely and inevitable leading to cutthroat competition. Additionally, Toss Bank faces the immediate challenge of normalizing its loan business, which has been hindered by the government’s total household loan volume regulations.

An industry insider said, "Like other internet-only banks, Toss Bank is bound to experience initial losses. The success or failure in the early stages will depend on how quickly it can differentiate itself, comply with regulatory requirements for soundness management, protect financial consumers, and establish internal control systems in its credit card business."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}