U.S. S&P 500 Hits Record High for 5 Consecutive Trading Days

KOSPI Fails to Sustain 3000 Level Repeatedly

South Korean Companies' Net Profit Forecasts Revised Downward

Domestic Stock Market Adjusts After Early-Year Surge

[Asia Economy Reporter Ji Yeon-jin] Recently, as the domestic stock market continues to experience a ‘decoupling’ phenomenon from advanced markets such as the United States, the securities industry is busy analyzing the background. Decoupling refers to ‘de-synchronization,’ meaning that a country or region’s economy shows independent movements that differ from the overall global economic trends.

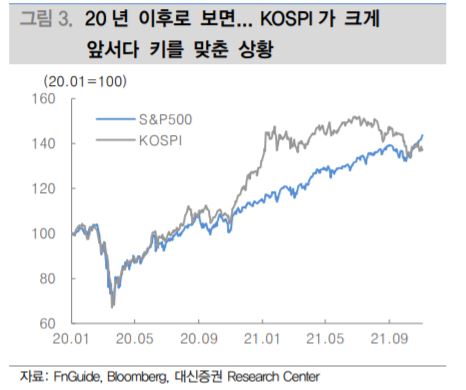

According to the financial investment industry on the 8th, the U.S. stock market hit another all-time high again on the 5th (local time). The U.S. S&P 500 index and Nasdaq index have been rising continuously since the 27th of last month, setting new highs for five consecutive trading days. Although the U.S. Federal Reserve (Fed) announced the start of tapering (reduction of asset purchases) earlier this month, investors who were concerned about this took it positively, leading to a global stock market relief rally. In contrast, during this period, the KOSPI has repeatedly failed to settle around the 3,000-point level, fluctuating near that mark. It showed early strength due to the overnight positive momentum from the U.S. market but weakened later, with the intensity of the decline deepening recently. On this day as well, the KOSPI index started lower and widened its losses during the session.

Experts identified the biggest reason for the intensified decoupling as the increasingly lowered profit expectations of domestic companies. BNK Investment & Securities forecast that the KOSPI 200 operating profit will end its ‘surprise earnings’ streak by hitting an all-time high in the third quarter of this year, and that the KOSPI 200 net profit will decrease by 1.9% next year. This is due to the expected decline in DRAM prices and the net profits of sectors that led earnings improvements next year. Kim Sung-no, a researcher at BNK Investment & Securities, said, “As recent trading volumes have decreased, volatility has expanded due to program trading. Although year-end dividend arbitrage may occur, it is difficult to find immediate stock price momentum, so a lull phase is likely to continue for the time being.”

On the other hand, in the U.S., the current capacity utilization rate is 75%, which is 80% lower than the peak. The U.S. economic momentum is likely to improve as the worst period passed in August and September, with the capacity utilization rate expected to rise. This is positive for the labor market and is expected to boost corporate profits through steady consumer expansion. Lee Jae-man, a researcher at Hana Financial Investment, said, “Without liquidity supply, stock returns are determined by earnings growth rates, and there is a clear difference between the U.S. and domestic stock markets in this regard. From now on, when selecting stocks, the 2022 earnings growth rate and whether earnings estimates are being revised upward will be important.”

The domestic stock market’s rapid rise from the end of last year to early this year, followed by a correction to align with the global market, as well as an industrial structure vulnerable to global supply shortages, have also been pointed out as causes of decoupling. The KOSPI surged by 1,000 points (44%) from its low in November last year to its peak in January this year, outperforming the global stock market by 20 to 30 percentage points. Lee Kyung-min, a researcher at Daishin Securities, pointed out, “The rapid rise of the KOSPI at that time led to a weakening of relative attractiveness compared to the global stock market, resulting in a stagnant phase.” However, although the alignment process was completed in September, the prolonged global supply shortage has reduced the attractiveness of domestic companies with high external dependence. In fact, cyclical sectors sensitive to the economy, IT, and automobile sectors related to supply chain disruptions account for 58.9% of the KOSPI, whereas they make up only 28.8% of the U.S. S&P 500. The researcher said, “As global supply chain bottlenecks are prolonged and intensified, differences in industrial structure and stock market structure are leading to differentiation between advanced and emerging markets, and between the U.S. and Korean stock markets.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}