Woori and Shinhan Bank SME Loan Growth Rate Over 3 Times Household Loan Growth

[Asia Economy Reporter Park Sun-mi] While commercial banks are tightening household loans, they are significantly increasing corporate loans, maintaining overall loan growth. With the financial authorities' announcement of strengthened household loan management measures, it is expected that banks will find it difficult to increase household loans next year as well, accelerating the trend of focusing on corporate finance for the time being.

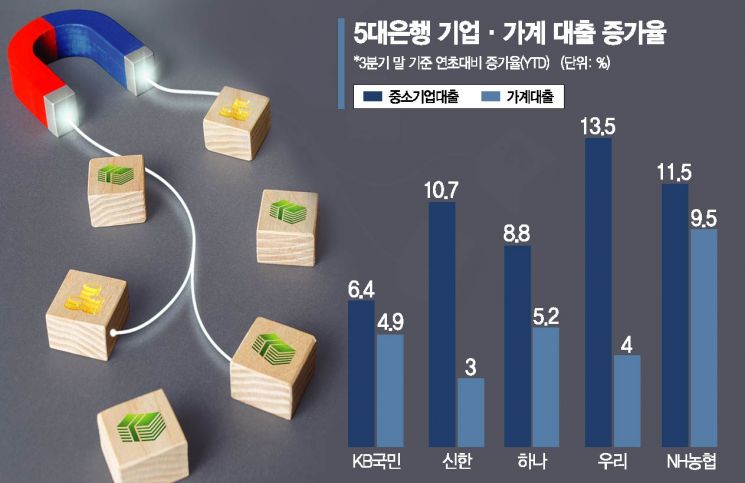

According to the financial sector on the 28th, as of the end of the third quarter, the year-to-date growth rates of small and medium-sized enterprise (SME) loans (including individual business owner loans) at the five major commercial banks are Woori (13.5%), NH Nonghyup (11.5%), Shinhan (10.7%), Hana (8.8%), and KB Kookmin (6.4%), respectively. During the same period, the household loan growth rates were Woori (4%), NH Nonghyup (9.5%), Shinhan (3%), Hana (5.2%), and KB Kookmin (4.9%), all of which were lower than the SME loan growth rates.

In particular, Woori Bank and Shinhan Bank saw the gap between SME loan and household loan growth rates widen to more than three times. Woori Financial praised the background of the significant increase in interest income when announcing its record-breaking third-quarter performance as "the result of focusing on SME-centered loans." Shinhan Bank also cited the expansion of SME-centered financial support as one of the reasons for the rise in the bank's interest income growth rate in the third quarter.

The surge in SME loans in the banking sector is largely due to the continued COVID-19-related financial support and increased demand for facility funds centered on some industries with improved business conditions. The monthly increase in total SME loans by banks in September, as compiled by the Bank of Korea, was 7.4 trillion won, the highest ever since statistics began.

Banking Sector Environment Forces Increase in Corporate Loans

With the financial authorities announcing strengthened household loan management measures, the banking sector's reliance on corporate loans is expected to increase not only in the fourth quarter of this year but also in early next year. This is because the environment has been created where it is difficult to further increase household loans.

Until the end of this month, the maximum loan limit provided by 17 banks when renewing jeonse (long-term deposit lease) loan contracts is limited to the amount of the increased jeonse price. The loan thresholds for mortgage loans, credit loans, and others are also becoming increasingly stringent. SC First Bank will completely suspend new sales of its mortgage loan product ‘First Home Loan’ starting from the 29th, and Nonghyup Bank will significantly lower the limits on credit loans and overdraft accounts to 20 million won from the 1st of next month until the end of the year.

Industry insiders expect that as the environment no longer allows loan growth to rely on household loans, the focus on expanding the share of individual business owner loans within SME loans will accelerate. Unlike household loans, total volume management is not required, so banks can increase loans at their discretion. Commercial banks such as Kookmin and Woori are launching niche products available to businesses listed on platforms like Coupang, Baedal Minjok, and Naver, and are expanding non-face-to-face services for individual business owner loans, reflecting a strategy to drive SME loan growth.

Due to these efforts by commercial banks, there is significant potential for SMEs to increase their proportion of funding through commercial banks. According to the ‘2021 SME Financial Status Survey’ recently released by the IBK Economic Research Institute, SMEs procured 49.6% of their new funds from banks last year. In particular, the share of main bank types for SMEs was 46.5% for commercial banks, 35.4% for specialized banks, and 15% for regional banks as of 2015, but last year, these shares were 62%, 16.9%, and 9.3%, respectively.

A bank official explained, "This atmosphere could pose a threat to IBK Industrial Bank of Korea, which holds the number one market share in SME loans," adding, "IBK, which continues to operate SME and small business support programs and increase SME loans, holds the top market share in SME loans (22.9%) as of the end of the third quarter, but as commercial banks turn their attention to targeting SMEs, SMEs now have more options."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}