Hana Financial Research Institute '2022 Financial Industry Outlook'

A Time for Solid Management Over Asset Expansion Competition

[Asia Economy Reporter Kiho Sung] It is forecasted that asset growth will weaken next year due to the end of financial regulatory easing measures and a slowdown in the increase of market liquidity. Additionally, as the interest rate rise period begins, the burden of funding costs in the secondary financial sector is increasing, indicating that sound management is needed rather than competition to expand assets.

Hana Financial Management Research Institute, affiliated with Hana Bank, released the '2022 Financial Industry Outlook' report on the 21st containing these insights.

The report projected that with the scheduled end of loan maturity extensions, interest payment deferrals, and financial regulatory easing measures in March next year, asset growth will weaken alongside a slowdown in market liquidity growth. Furthermore, except for banks and life insurance companies which benefit positively from the interest rate rise period, the secondary financial sector is expected to see profitability weaken due to increased funding cost burdens.

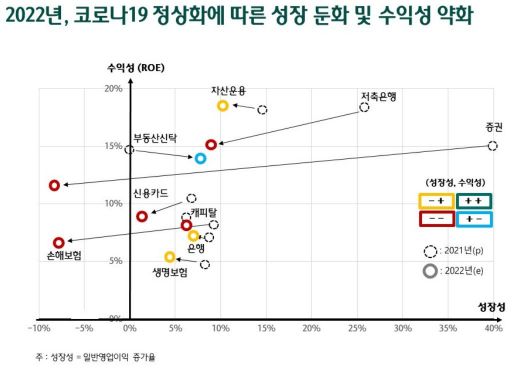

The institute anticipated that considering the sharp increase in assets across all financial sectors this year due to the surge in market liquidity from COVID-19 related policy support, loan regulations will tighten across all financial sectors next year, slowing asset growth. In particular, demand for loans for investment is expected to significantly slow due to credit loan limits and base rate hikes, but demand for real needs such as mortgage loans and jeonse (long-term deposit) loans is expected to continue, making a sharp decline in loan growth rates unlikely. Since household loan regulations include the secondary financial sector, the balloon effect is expected to be partially blocked. Although funding support for small and medium enterprises and small business owners will shrink compared to this year during the COVID-19 normalization process, it is expected to continue for a considerable period.

Meanwhile, as the interest rate rise period begins next year, banks’ net interest margin (NIM) is expected to enter a full recovery phase due to increases in low-cost deposits and wider loan interest rate hikes. Along with the rise in net interest margin, non-interest income is also expected to increase as commercial banks strengthen asset management businesses. However, since banks’ loan loss costs are expected to slightly increase compared to this year during the COVID-19 normalization process, close monitoring is necessary. Life insurance is also expected to see a slight improvement in profitability benefiting from the interest rate rise through improved investment gains and eased variable guarantee reserve burdens.

With the interest rate rise, the profitability of the secondary financial sector is expected to generally weaken due to increased funding costs. In particular, for credit card companies, the amount of credit card bonds maturing in 2022 is expected to reach 36 trillion won, and the limit on credit card bonds included in hedge assets for derivative-linked securities will be reduced from 15% to 12% next year, making funding more difficult.

The institute expects that although deterioration of soundness indicators is inevitable during the COVID-19 normalization process, the indicators will not be significantly damaged as government and private financial companies’ soft-landing programs operate. Proactive provisioning has been made so far, and with the entry into the With COVID-19 phase, consumption recovery and sales increases in vulnerable industries are expected to improve borrowers’ principal and interest repayment ability. However, potential risks of vulnerable borrowers still exist, so monitoring of multiple debtors and marginal companies is necessary. Furthermore, the role of private financial companies is considered important to minimize shocks during the COVID-19 normalization process.

As the untact culture becomes entrenched due to COVID-19, and the MyData business is fully implemented, competition for market dominance between banks and non-financial companies is expected to intensify. Along with this, competition among financial companies in markets such as mid-interest loans, retirement pensions, and wealth management (WM) is expected to become fierce, making securing competitiveness for survival the most important task next year.

Additionally, with the planned revision of the Electronic Financial Transactions Act and enactment of the Fintech Promotion Support Act next year, platform companies’ entry into finance and financial companies’ fintech investments are expected to be activated. Through this investment activation, technologies such as artificial intelligence (AI) and blockchain are expected to be widely utilized across the financial sector. As competition intensifies, securing competitiveness in specific businesses is considered important.

Researcher Heesoo Jung of Hana Financial Management Research Institute stated, “Entering the With COVID-19 era and the interest rate rise period next year, it is important for the financial sector to focus on profitability-centered sound management rather than asset expansion.” He emphasized, “Since the impact of COVID-19 has not been completely resolved, it is necessary to prepare measures to gradually mitigate potential risks.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}