Following NongHyup and Hana, KB Kookmin Bank Drastically Reduces Loan Limits Starting the 29th

[Asia Economy Reporter Lee Kwang-ho] Following NongHyup and Hana Bank, KB Kookmin Bank is also drastically reducing household loan limits. The household loan growth rate is approaching the financial authorities' management target of 5-6% annually for this year, putting loan windows at risk of closing entirely. As the loan cliff becomes a reality in three of the five major banks, there is a strong possibility of a balloon effect toward Shinhan and Woori Banks, which still have some leeway. With the domino effect of banks potentially halting loans and tightening credit even in the secondary financial sector, the frustration and backlash from real demand borrowers preparing for marriage and moving are expected to intensify.

According to the financial sector on the 27th, KB Kookmin Bank will drastically reduce limits on mortgage loans, jeonse deposit loans, and group loans starting the 29th.

The limit on jeonse deposit loans will be restricted within the range of the increase in the rental deposit (jeonse price). For example, if the jeonse price rises from an initial 400 million KRW to 600 million KRW, an increase of 200 million KRW, tenants without existing jeonse deposit loans could previously borrow up to 80% of the jeonse price (480 million KRW). However, from the 29th, loans exceeding the increase in the jeonse price of 200 million KRW will no longer be possible.

The collateral criteria for move-in balance loans among group loans will change from "KB market price or appraisal value" to "the lowest amount among the sale price, KB market price, and appraisal value." For example, if the sale price of an apartment is 500 million KRW but the current market price has surged to 1 billion KRW, the loan limit for the balance will now be based on the original sale price of 500 million KRW, not the 1 billion KRW market price.

Mortgage loans will have restrictions on subscribing to Mortgage Credit Insurance (MCI) and Mortgage Credit Guarantee (MCG). MCI and MCG are insurances subscribed simultaneously with mortgage loans; borrowers with these insurances can receive loans up to the Loan-to-Value (LTV) ratio, but without insurance, loans are only possible up to the amount excluding small rental deposits.

Woori and Shinhan Banks Have Leeway but Concerns Over Concentration... Loan Thresholds Expected to Rise Further

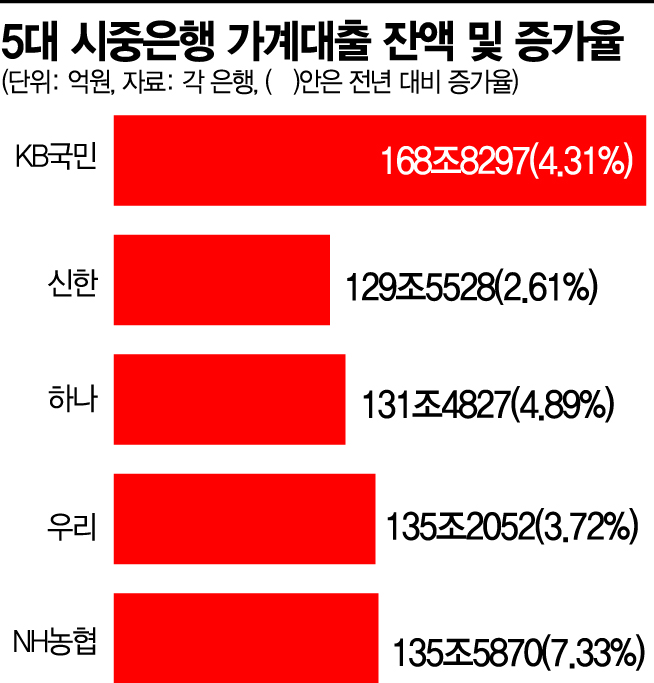

This measure follows NongHyup Bank's loan freeze last month, which caused a balloon effect toward KB Kookmin Bank. As of the 23rd, KB Kookmin Bank's household loan balance was 168.8297 trillion KRW, a 4.31% increase compared to the end of last year. Although it did not exceed the 5-6% growth target set by financial authorities, the rapid pace of increase is problematic. The household loan growth rate at KB Kookmin Bank was only 2.58% at the end of July, then jumped 1 percentage point to 3.62% in one month, and soared to 4.31% as of the 23rd of this month.

As KB Kookmin Bank, which has the largest household loan volume among domestic banks, tightens loans, other banks are preparing for a balloon effect. Hana Bank, with a household loan balance of 131.4827 trillion KRW as of the 23rd, up 4.89% from the end of last year, will temporarily restrict some MCI and MCG loan products starting next month on the 1st.

Woori Bank and Shinhan Bank have household loan balances of 135.2052 trillion KRW and 129.5528 trillion KRW, respectively, showing increases of 3.72% and 2.61% compared to the end of last year, indicating some leeway, but they are closely monitoring potential concentration effects.

A bank official said, "With the financial authorities' strong intention to manage household loans, the loan thresholds at banks will become even higher," adding, "Loan demand is expected to surge next month due to the marriage and moving seasons, which is worrisome." In fact, October is the month with the highest household loan demand annually. According to the Financial Supervisory Service, the average monthly household loan increase from 2015 to 2020 was highest in October at 10.8 trillion KRW.

"Total Volume Management Extended Beyond Next Year... High-Intensity Measures to Continue and Be Implemented Gradually"

Despite the expected loan cliff for real demand borrowers, financial authorities have no plans to revise the household loan total volume growth target. A financial authority official emphasized, "There are no plans to adjust the household loan total volume target," and added, "We will monitor the household loan growth trend and prepare additional measures."

On the same day, Financial Services Commission Chairman Ko Seung-beom stated at a meeting with economic and financial market experts, "We will extend the timeline for managing total household debt beyond next year and continue to implement high-intensity measures continuously and gradually until the effects of the measures become apparent."

Chairman Ko explained, "The most important criterion in loan decisions should be whether the borrower can handle the loan and repay it stably even if circumstances change in the future," and added, "The core of the household debt measures to be announced by the government in October will focus on enhancing the effectiveness of repayment ability assessments."

The financial authorities are considering additional household debt management measures, including advancing the schedule for phased implementation of the Debt Service Ratio (DSR) regulation by borrower and strengthening DSR regulations on the secondary financial sector. Measures to restrict securities firms' margin loans are also being discussed. The announcement is expected shortly after the National Assembly audit.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}