Internet Banks Raise Mid-Interest Rate Targets Following Authorities' Warnings

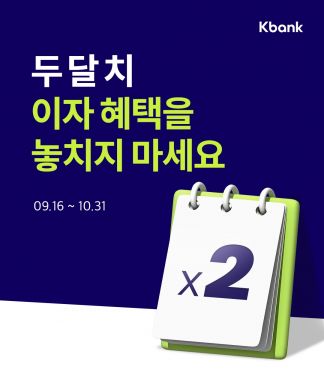

K-Bank Offers "100% Interest for Two Months"

Mainstream Banks, Previously Lukewarm on 'Mid-Interest Rates,' Also Increase Share

Concerns Arise Over Potential Regulatory Targeting as Scale Grows

[Asia Economy Reporter Song Seung-seop] Despite the strong stance on household loans, the ‘mid-interest rate’ loan trend is heating up across all financial sectors, including commercial banks. It is analyzed that the financial authorities’ ‘carrot and stick’ approach?offering incentives or exempting mid-interest loans from lending regulations while threatening sectors with insufficient supply?has been effective. However, concerns coexist that the rapidly increasing mid-interest rate loans might become a target for future regulatory measures.

In Response to Criticism of "Insufficient Mid-Interest Loans"... Internet Banks 'Ultra-Focus' on Mid-Interest Loans

According to the financial industry on the 17th, the sector most aggressively supplying mid-interest rate loans is internet-only banks. KakaoBank has executed 502 billion KRW in unsecured credit loans for mid- to low-credit borrowers over the past three months. Of this, 300.4 billion KRW was disbursed in August alone, an increase of about 160% compared to the previous month. Last month, it also launched new products such as the 'Mid-Credit Plus Loan' and 'Mid-Credit Emergency Loan' for mid-credit borrowers.

K Bank also announced that starting from the 16th, it will refund 100% of two months’ interest to mid-interest loan customers. The target is new credit loan customers with a credit score of 820 or below who apply by the end of next month. Additionally, it plans to improve its Customer Credit Scoring (CSS) model to increase loan opportunities and enhance interest rate benefits.

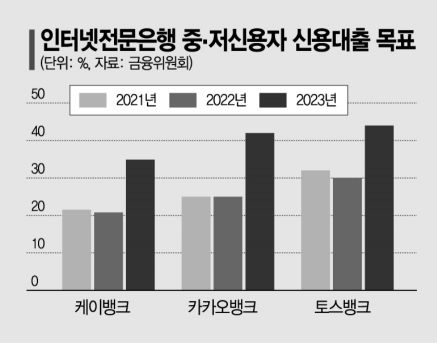

Toss Bank, which is about to launch, has pledged to expand the proportion of mid-interest rate loans to 34.9% this year, higher than KakaoBank and K Bank’s target of around 20%.

Many view the internet banks’ focus on mid-interest loans as a response to the authorities’ ‘stick.’ Internet banks initially declared they would concentrate on products for mid- to low-credit borrowers. However, after launching, they focused on high-credit borrowers, prompting the Financial Services Commission in May to warn that “the proportion of credit loans to mid- and low-credit borrowers is lower than that of commercial banks,” and that “performance will be re-examined, plans reviewed, and gradual expansion will be enforced.”

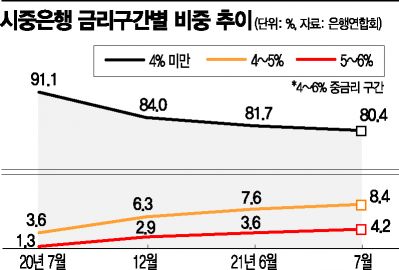

Commercial banks, which maintained high-credit loans even during economic downturns or when risk management was necessary, also appear to be focusing on mid-interest loans. According to the Korea Federation of Banks, the proportion of mid-interest rate credit loans (4?6%) among the four major commercial banks?KB Kookmin, Shinhan, Hana, and Woori?was 12.7% last month, up 1.5 percentage points from 11.2% the previous month. Compared to 9% at the end of last year, it increased by 3.7 percentage points. A year ago, the mid-interest loan proportion of the four banks was only 5.2%. Notably, loans in the 5?6% range expanded more than threefold from 1.3% to 4.25% during this period.

Conversely, the proportion of high-credit loans decreased rapidly. Last month, loans with interest rates below 4% accounted for 80.4%, down 1.3 percentage points from the previous month. In July last year, 91.1% of all credit loans were products for high-credit borrowers with rates below 4%.

This trend was most pronounced at Kookmin Bank. The proportion of credit loans below 4% at Kookmin Bank dropped from 89.5% a year ago to 71.3%, the lowest among the four banks. It was followed by Hana Bank (79.8%), Shinhan Bank (81.4%), and Woori Bank (89.2%). During the same period, Kookmin Bank’s mid-interest loan proportion surged from 7.3% to 20.9%, double that of Shinhan Bank (10.8%), which ranked second. Shinhan Bank showed the steepest increase, rising from 3.5% to 10.8%.

The financial authorities view the surge in household debt as partly due to high-credit borrowers’ ‘debt investment (debt-financed investment).’ At the end of last year, some banks attempted to create loan products for professionals with loan limits up to 2.7 times their annual salary but were blocked by the authorities. Consequently, the financial sector has been reducing loan limits for professional borrowers, who are considered high-income earners. A commercial bank official explained, “Due to increased speculative demand, we had no choice but to uniformly reduce income limits to curb household debt,” adding, “This naturally led to a decrease in loans to high-income borrowers with high salaries.”

Giving Volume Leeway and Considering Incentives... Expanded the Mid-Interest Market

On the other hand, savings banks are supplying aggressive mid-interest products thanks to the financial authorities’ ‘carrot.’ SBI Savings Bank, the industry leader, recently launched the ‘79 Loan,’ a credit loan product offering fixed interest rates from 7.5% to 9.4%, with a maximum loan limit of 100 million KRW. The target borrowers are mid- to low-credit individuals aged over 20 or with a credit score of 670 or higher. ES Savings Bank introduced the ES Needs Loan product with a minimum interest rate of 4.8%, a mid-interest loan product for salaried workers who can provide income verification. The loan limit ranges from 1 million to 100 million KRW.

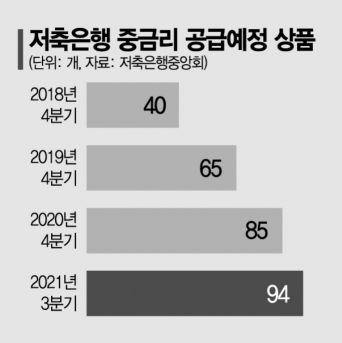

Savings banks must limit household loans to 21.1% growth compared to the end of the year, but mid-interest loans or policy finance loans are allowed a 15.7% increase, which is more generous than the 5.4% allowed for high-interest loans. As long as they meet the lowered mid-interest loan requirement (16%), relatively active lending operations are possible. Incentives such as expanding the business area by up to 150% or awarding extra points in management evaluations based on mid-interest loan performance are also under consideration.

The online lending industry, which completed formal sector registration at the end of August, is promoting mid-credit funding through technology finance. By applying a P2P model, they intend to lend money at mid-interest rates even to ‘thin filers’ (people with insufficient financial history) who are difficult to serve by traditional financial institutions. In fact, most mid-interest loans in the online lending sector are refinancing products for those switching from savings banks or loan companies.

The problem is that as the mid-interest market becomes a battleground, there are concerns it could become a target for financial authorities’ regulations. Loan products that were previously exempt from regulations for real demand borrowers and low-income groups may now be subject to management depending on debt levels. A typical example is mid-interest loans from savings banks, which were once excluded from total volume regulations but later included. A financial industry official said, “We thought jeonse (long-term deposit) loans would be free from regulations, but now there are talks that they might not be,” adding, “It’s a policy risk that is difficult to predict when and how tightening will occur.”

Experts point out that uniformly tightening mid-interest loans to achieve debt control goals is inappropriate. Professor Sung Tae-yoon of Yonsei University’s Department of Economics analyzed, “It is problematic to block loans after confirming that the borrower has real demand,” and added, “If income and credit are deemed appropriate, loans should be provided accordingly.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}