Unreasonably High Dividend Rates at Some Investment Firms

Attention on Disclosure of 6 Hidden Investors

[Asia Economy Reporters Kangwook Cho, Dongpyo Kim] The political battle over the controversy surrounding preferential treatment in the Seongnam Daejang District development project, which Gyeonggi Province Governor Lee Jae-myung promoted during his tenure as mayor of Seongnam, is intensifying. The issue began when a private developer holding a 1% stake in the development project promoted by Seongnam City gained enormous profits worth hundreds of billions of won. This article summarizes the process and nature of the mega development project worth over 1 trillion won, its differences from existing projects, the preferential treatment in private contracts, and the disclosure of investors, which are the current points of contention.

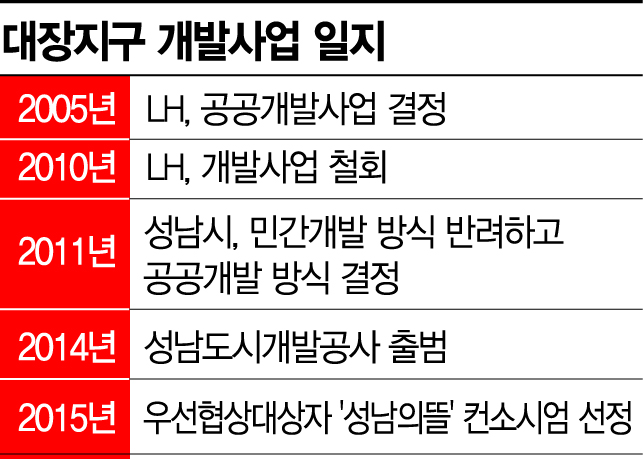

◇ Public Development or Private Development = The Daejang District development project is an urban development project worth 1.15 trillion won to develop approximately 924,467 square meters (about 278,000 pyeong) in the Daejang-dong area of Bundang-gu, Seongnam. In 2005, the project shifted from a public development method by LH (Korea Land and Housing Corporation) to private development, but after Lee Jae-myung was re-elected as mayor of Seongnam in 2014, the project was switched back to public development. However, Lee decided to promote the development through a special purpose company (SPC) called ‘Seongnam Utddeul,’ jointly established by Seongnam Urban Development Corporation and private developers, rather than a method fully managed by the public sector.

According to industry sources, it is not uncommon for the project entity to form a consortium-type developer through public bidding for urban development projects. This is because if the development project fails due to unsold units, the public sector must bear all the risks. Although Seongnam Urban Development Corporation declared a moratorium graduation in 2013, industry analysts believe that due to realistic financial conditions, it was difficult for the corporation to implement the project alone, so they chose private participation.

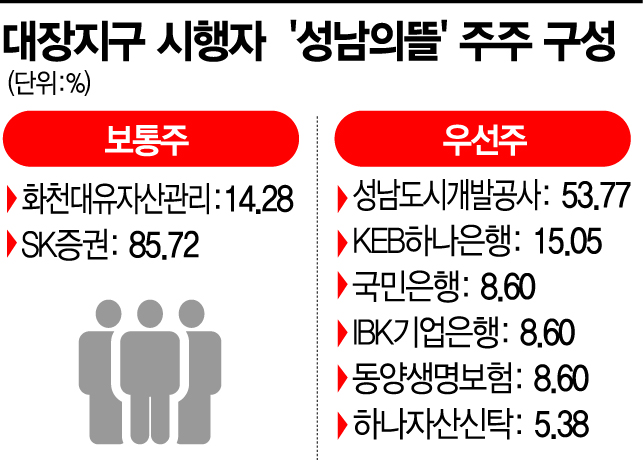

Seongnam Urban Development Corporation only set the condition of guaranteeing a minimum net profit of 500 billion won, and the actual project entity was the private developers participating in the consortium. Therefore, this project was classified as private development and was not subject to the price ceiling on pre-sale prices. As a result, the non-application of the price ceiling and the booming real estate market allowed Hwacheon Daeyu, which held a 1% stake in Seongnam Utddeul, to earn profits exceeding 1000% relative to its equity capital.

◇ Differences from Existing Urban Development Project Structures = The most notable feature of the Daejang District development project is that the public sector participated in private development to recover development profits. A ‘pre-determined profit confirmation method’ was used to guarantee profits generated from the project in advance, which is uncommon in typical urban development projects.

Experts have evaluated this development method as unusual. One developer said, "In development projects, large profits arise from acquiring land at low prices, then increasing land value through zoning changes, and reselling it," adding, "Therefore, the approval process is quite challenging."

He added, "In the case of the Daejang-dong development, it seems that Seongnam Urban Development Corporation participated in the project finance vehicle (PFV), which allowed them to fundamentally exclude such approval risks." He also said, "If pre-determined profits and dividends were agreed upon through contracts, it is difficult to raise issues, but some of the dividend rates reported by the media for certain investors are at an unreasonable level."

◇ Was the Private Contract for Hwacheon Daeyu’s 5 Plots Preferential Treatment? = Hwacheon Daeyu secured five plots (four apartment complexes and one row house), totaling 150,109 square meters, out of 15 zones divided from the land developed by Seongnam Utddeul, the main developer of the Daejang District, in 2017. Hwacheon Daeyu acquired these construction sites through private contracts rather than competitive bidding.

However, Seongnam Urban Development Corporation responded that the private contract itself is not preferential treatment. When Seongnam Utddeul signed a business agreement with Seongnam Urban Development Corporation in March 2015, it included a clause stating that this was compensation for Hwacheon Daeyu’s capital contribution and risk-sharing. A Seongnam Urban Development Corporation official explained, "According to the Urban Development Act, investors can directly implement apartment projects on some plots," adding, "Hwacheon Daeyu is the same, and the five plots were supplied as direct use by investors, which is based on the business agreement."

◇ Is Disclosure of the Six Hidden Investors Possible? = The most focused issue is whether the six hidden investors can be disclosed. SK Securities, which received a total dividend of 404 billion won over three years along with Hwacheon Daeyu, is a specific money trust consisting of seven people: Mr. A, who owns 100% of Hwacheon Daeyu’s shares, and six investors he recruited. This trust is related to Hwacheon Daeyu’s affiliates (Cheonhwa Dongin 1 to 7).

However, under the Capital Markets Act, these investors cannot be disclosed. Private equity funds operate by recruiting a small number of high-net-worth investors privately, not the general public. The Investment Trust Act limits investors to 100 or fewer, and the Capital Markets and Financial Investment Business Act limits recruitment to fewer than 50. Therefore, revealing the actual owners of Hwacheon Daeyu and Cheonhwa Dongin could itself be a violation of the law.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}