Identical Functions, Identical Regulations at Issue

Big Tech: "Services Provided Are Different"

Card Companies: "Exclusion from Regulation Is Unfair"

[Asia Economy Reporter Ki Ha-young] With the financial authorities' regulatory moves targeting big tech (large information and communication companies), the dispute over fee rates between big tech and card companies is reigniting. The core issue is 'same function, same regulation.' Card companies view big tech as providing the same payment functions in the simple payment market, but big tech argues that the services offered are different, making direct comparison unreasonable.

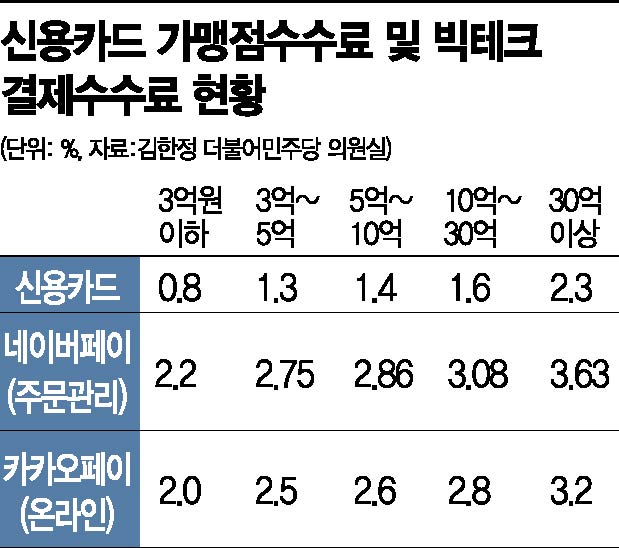

According to the office of Kim Han-jung, a member of the National Assembly's Political Affairs Committee from the Democratic Party of Korea, as of the end of last month, the merchant fees for card companies' preferred merchants with annual sales of 3 billion KRW or less range from 0.8% to 1.6%, whereas big tech payment fees range from 2.0% to 3.08%. In particular, for small business owners with annual sales of 300 million KRW or less, credit card fees are 0.8%, while Naver Pay's order-based payment fee is 2.2%, nearly three times higher.

In response to concerns about fairness between credit card and big tech fees, Naver Financial, which operates Naver Pay, rebutted that the comparison is not equivalent. They claim that the actual fee rate, excluding fees paid to credit card companies and order management fees, is only 0.2% to 0.3%.

Naver Financial explained, "The fees consist of merchant fees paid to credit card companies and fees related to the role of payment gateway (PG) companies, which bear risks such as losses from defaults by low-credit online shopping malls." They added, "Order-based payment fees include not only PG functions but also various services such as sales management including shipping, exchanges, and returns, delivery tracking, fast settlement support, and fraud detection system (FDS)." In other words, since order management-type Naver Pay provides multiple additional services, it is inappropriate to directly compare its fees with credit card fees that only provide payment functions. They also noted that both Naver Pay's payment fees and order management fees are among the lowest in the industry.

However, the card industry points out that while the simple payment market is rapidly growing, big tech companies providing the same payment functions are exempt from regulation. An industry insider said, "Card companies, under the Specialized Credit Finance Business Act, undergo a re-estimation of eligible costs every three years, resulting in losses on fees from small merchants." He added, "Even if big tech's actual fee rate is 0.2% to 0.3%, they are ultimately making a profit." He also explained that services such as settlement support, fraud prevention, and member management, excluding sales management like shipping and exchanges, are already provided by card companies.

Ultimately, the common industry opinion is that the problem lies in big tech companies providing the same services without being subject to fee-related regulations. Another industry official said, "Simple payment companies are subject to the Electronic Financial Transactions Act, which does not mandate fee-related policies." He added, "In the simple payment market, which is growing at double-digit rates annually, it is unfair that companies providing the same payment services are subject to differentiated regulations."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}