China's Market Share Expected to Reach 71% by 2025... Korean Companies Threatened in OLED Market as Well

[Asia Economy Reporter Jeong Hyunjin] As the production capacity (capability) of the global display industry expands significantly, concerns about oversupply are growing. With China pouring in aggressive investments, it is expanding its presence not only in the LCD panel market but also in the OLED panel market, threatening Korean display companies such as LG Display and Samsung Display.

On the 17th, display market research firm DSCC forecasted in a recent report that the display production capacity of major countries including Korea, China, Taiwan, and Singapore will increase by 13% this year and 10% next year, with next year's production capacity expected to exceed 300 million square meters in terms of area. The compound annual growth rate (CAGR) from 2020 to 2025 was also revised upward from the initially expected 6.1% in June to 7.4%. The global display industry's production capacity had already surged with double-digit growth rates during 2018-2019.

The problem is that as display supply is increasing faster than expected, downward pressure on prices is occurring. LCD panel prices have already peaked in June-July and are showing a declining trend. TV demand due to COVID-19 is also decreasing, and related display sales are expected to decline. Another market research firm, TrendForce, reported, "Some display manufacturers have begun evaluating whether to adjust production capacity in the fourth quarter of this year, as they believe the supply-demand imbalance in the TV panel market will not resolve on its own."

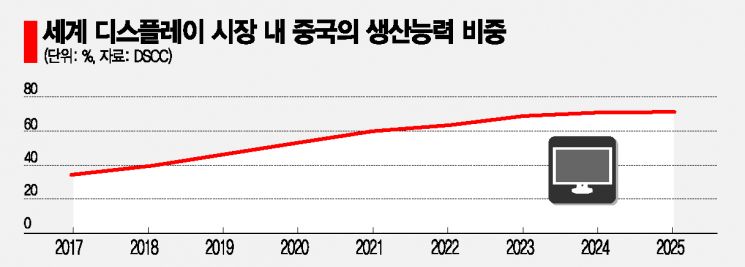

It is also a point of caution for domestic companies that China is leading the recent expansion of production capacity in the display industry. DSCC projected that China's share of display production capacity will expand from 53% last year to 71% by 2025. China BOE, which expanded its footprint in the LCD panel market where domestic companies had strengths, overtook LG Display in 2019 to become the industry leader, and recently has been rapidly increasing investments in OLED panels, thereby expanding its production capacity itself.

On the other hand, DSCC expects Korea's production capacity share to decrease from 19% last year to 8% by 2025. LG Display maintained the top position in total display production capacity until 2018 but ranked second in 2019, and is projected to fall to third next year, fourth in 2023, and fifth in 2024, with its share declining in terms of production capacity. China CSOT was mentioned as the company expected to surpass LG Display's production capacity next year.

In the OLED market, LG Display and Samsung Display currently hold an advantage over Chinese companies, but China's rapid growth is posing a threat. Looking at total OLED production capacity, Samsung Display is expected to lead from 2016 to 2020, and LG Display from 2021 to 2025. However, in terms of CAGR from 2020 to 2025, Samsung Display and LG Display are estimated at 12% and 19%, respectively, while China BOE and CSOT are estimated at 25% and 52%, respectively, indicating that Chinese companies will significantly surpass Korean companies, according to DSCC.

TrendForce stated, "As the TV panel market has recently started to show weakness, the industry must be alert to whether Chinese display manufacturers will abandon their previous strategy of maximizing production capacity and shift to measures aimed at maintaining overall market health."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}