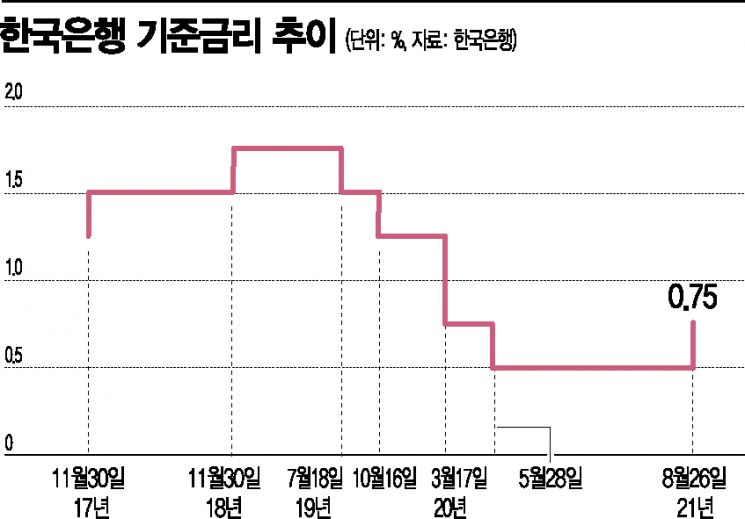

Additional Interest Rate Hike Expected Within the Year

Situation Where Interest Rate Effects Cannot Be Expected

Introduction of New International Accounting Standards Also a Hindrance

[Asia Economy Reporter Oh Hyung-gil] Savings-type insurance policies, which had been benefiting from the prolonged low interest rates and private equity fund scandals, are once again facing neglect.

With additional base rate hikes expected within the year, bank deposit and savings interest rates are also rising, making it difficult to expect relative interest rate advantages. From the insurers' perspective, the new International Financial Reporting Standard (IFRS17) introduced in 2023 recognizes most savings-type insurance as liabilities, so they cannot simply increase subscriptions to these policies.

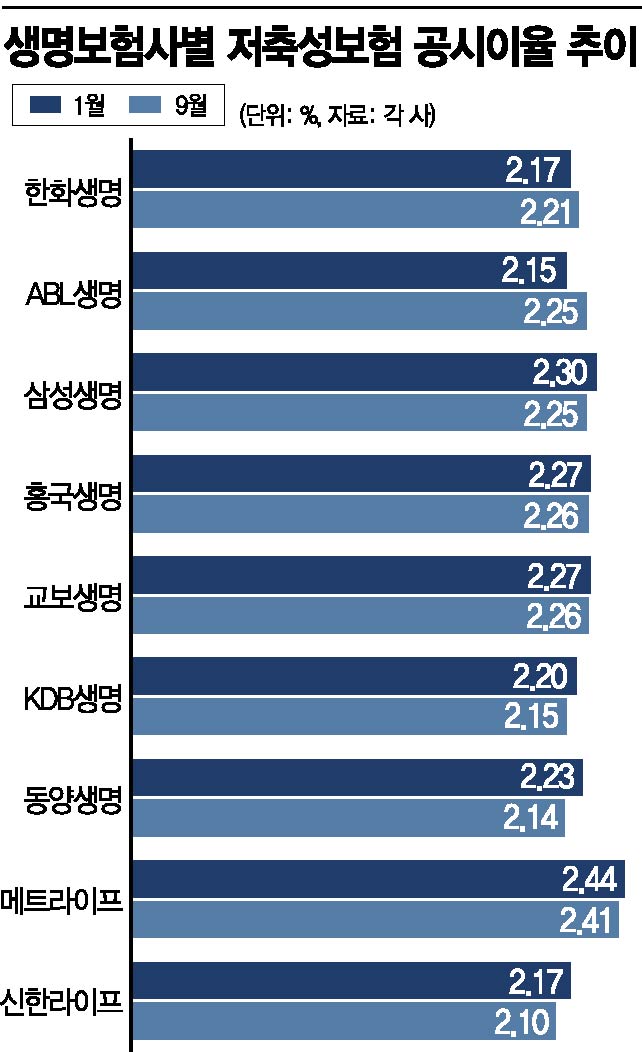

According to the insurance industry on the 15th, as of September, the disclosed interest rates for savings-type insurance policies from life insurance companies ranged from 2.10% to 2.41%. This marks a decline compared to the 2.17% to 2.44% range at the beginning of the year.

The disclosed interest rate, linked to market interest rates, represents the interest rate paid to customers. Insurers adjust the disclosed interest rate monthly, lowering it when market rates fall to minimize losses. Most of the savings-type insurance products currently sold are interest rate-linked; when the disclosed interest rate drops, the maturity refund decreases accordingly, potentially leading to losses for policyholders.

Among insurers, MetLife Life Insurance had the highest rate at 2.41%. Kyobo Life and Heungkuk Life recorded 2.26% each, while Samsung Life and ABL Life each had 2.25%. Shinhan Life was relatively lower at 2.10% compared to other life insurers.

With savings banks recently offering fixed deposits in the 2% range, the trend of rising interest rates for bank deposit and savings products is expected to continue. According to the Korea Federation of Savings Banks, as of September, the average interest rate for one-year fixed deposits at domestic savings banks was 2.18% per annum, up 0.28 percentage points from the end of last year. This is 1.08 percentage points higher than the average one-year fixed deposit rate of 1.10% in the banking sector as of July.

Internet-only banks are also raising interest rates. Toss Bank, the third domestic internet-only bank launching early next month, is currently accepting pre-registrations for demand deposit accounts that pay 2% annual interest with no restrictions on subscription period. Kakao Bank also raised its basic interest rates for new deposit and savings accounts by 0.3 to 0.4 percentage points starting from the 9th.

If the interest rate gap between savings-type insurance and deposit/savings products narrows further, it is expected to negatively impact the previously strong sales of savings-type insurance.

In the first half of this year, new contract amounts for savings-type insurance at life insurers surged by a remarkable 34.0% to 21.2089 trillion KRW compared to 15.8253 trillion KRW in the same period last year. In contrast, new contract amounts for protection-type insurance decreased by 4.4%, from 140.9221 trillion KRW to 134.6129 trillion KRW during the same period, showing a clear difference. Considering that savings-type insurance excludes business expenses unlike deposits and savings, this could also lead to policy cancellations.

Insurers are also in a difficult position to actively promote savings-type insurance sales. IFRS17 fundamentally changes the insurance liability evaluation method from the current cost basis to fair value, requiring future insurance payments to be discounted to present value using current interest rates.

Savings-type insurance, which guarantees future insurance payments, becomes a factor that increases liability burdens rather than profits. For this reason, insurers have been pursuing a strategy of reducing savings-type insurance sales while increasing protection-type insurance.

A life insurance industry official said, "Even if deposit and savings interest rates rise, the advantages of savings-type insurance remain, such as the ability to save at a high interest rate over a long period and the compound interest effect on the interest," but added, "However, if policyholders have earned returns above the principal, some may surrender early depending on the yield."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}