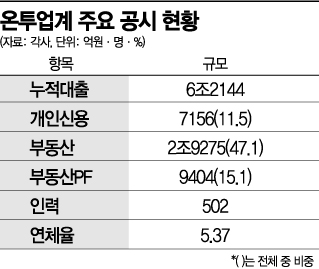

On-to-Use Industry's Cumulative Loan Volume of 6.2144 Trillion KRW in July-August

Real Estate Products Account for 47%... High-Risk PF Also Reaches 15%

Personal Credit Only 11%, Undermining the Purpose of Inclusive Innovation Finance

Beware of No Disclosures or Advertisements Claiming '0% Delinquency Rate'

The online investment-linked finance (OnTu industry), which emerged under the banner of innovative finance, has been found to be heavily focused on risky real estate project financing (PF). This has led to criticism that the original purpose of providing funds to middle- and low-credit borrowers who have difficulty borrowing money has been undermined. Some companies have high delinquency rates and poor disclosures, requiring investors to exercise special caution.

According to recent disclosures from various OnTu companies on the 6th, the cumulative loan volume in the OnTu industry for July and August reached 6.2144 trillion KRW. This is the initial performance report of 28 companies that completed registration by the deadline (August 26) set by financial authorities.

Most of the loans handled were products secured by real estate or betting on price increases. Real estate loan products accounted for 2.9275 trillion KRW, representing 47.1%. This contrasts sharply with personal credit loan products, which amounted to only 715.6 billion KRW, or 11.5%.

Real estate PF loans, classified as high-risk products, accounted for 940.4 billion KRW, or 15.1%, exceeding personal credit loans. Considering that domestic banks, recently criticized for increasing PF loans, handled about 5.4% of household credit loans as PF last year, this is quite significant. One registered OnTu company, WeFunding, structured 76.5% of its total loans solely as PF. Earnest Fund also reached 44.7%, with small-scale PF cases showing a delinquency rate of 80%. Large OnTu companies such as PeopleFund, WinkStone Partners, and Hello Fintech also have PF proportions exceeding 10-20%.

PF refers to lending based on real estate projects. It does not consider the credit of the real estate development company and has little or no collateral to recover in case of default. Since funds are raised based on future cash flows as repayment sources, it is considered the riskiest product even within the financial sector. Delinquencies or total losses can easily occur even during real estate booms.

Risk of Loss if Investing Recklessly... "Carefully Review Disclosures"

Accordingly, commercial banks hire experts who have long handled related products to verify PF. They also prepare separate countermeasures to offset losses depending on risks such as project delays, bond recovery, default, and legal issues. However, except for a few large companies, the entire OnTu industry has fewer than 30 employees. Some companies with only 12 employees have handled PF loans exceeding 9 billion KRW.

Current laws require OnTu companies to meet stringent physical and personnel conditions but do not apply specifically to individual products. This means related products can be handled without PF experts. An OnTu industry insider advised, "PF has high returns, making it easy to invest impulsively. Even if the product looks good, you should check the company's disclosures and first verify whether there are PF experts among the employees."

Some companies still have poor disclosures according to OnTu industry regulations. Even more than a week after registration, some companies have not disclosed key financial status citing site maintenance notices. Among them, some advertise guaranteed high returns or a 0% delinquency rate on their websites, requiring special caution. New companies may not have delinquencies due to short loan periods, but risks still exist.

A financial authority official warned, "When investing in P2P, verify whether the company is registered and be aware that principal guarantees are not provided. Companies offering excessive rewards and high returns are more likely to engage in mis-selling and handle poor-quality loans."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}