[Asia Economy Reporter Lee Seon-ae] Amid the sharp rise in stock prices of secondary battery material stocks, an investment strategy analysis has suggested the need to identify additional opportunities in the aluminum foil value chain, which has received relatively low attention until now.

On the 28th, Choi Bo-young, a researcher at Kyobo Securities, stated, "Most secondary battery companies announced surprise earnings in the second quarter of this year, and with the peak season effect for electric vehicles in the second half, strengthened eco-friendly policies, and expectations for expansion into the U.S., a steady trend is expected to continue," adding, "There will be investment opportunities in the relatively overlooked aluminum foil value chain."

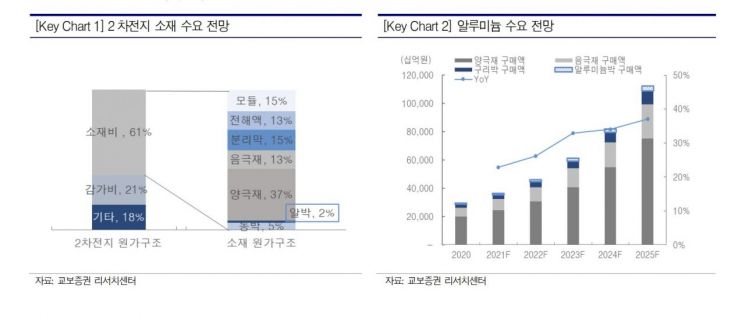

There are five main reasons to focus on the aluminum foil value chain. ① The aluminum foil industry has been undervalued and overlooked due to its low 1.8% proportion in secondary batteries. ② However, as a cathode foil material essential for secondary batteries, it inevitably accompanies the market growth of electric vehicles perfectly. ③ Aluminum prices have been hitting record highs since 2018, and structural price increases are expected to continue due to increased use of eco-friendly materials and a fire incident at an aluminum refining supplier. Therefore, an increase in the ASP of aluminum foil for EVs and an increase in its proportion within secondary batteries from 1.8% to over 2% are anticipated. ④ The number of major companies capable of producing aluminum foil for EVs is limited to six globally, and due to environmental issues, Chinese companies face difficulties in new expansions, so the competitiveness of existing operators is expected to continue. ⑤ Along with the earnings growth of domestic battery companies, the rise in operating profit margin in the second quarter of this year suggests that it is the early stage of earnings growth.

Kyobo Securities has identified the aluminum foil value chain as a timely area of interest and suggested aluminum and DI Dongil as related stocks. ‘Sama Aluminum’ is expected to inevitably expand its business as requests for overseas expansion and capacity increases from customers continue, based on its top domestic aluminum foil product competitiveness, and its price-to-earnings ratio (PER) for 2022?2023 is 16.1 times, indicating potential re-rating as a secondary battery material company. ‘DI Dongil’ is expected to achieve stable growth due to the aluminum foil business prospects and various business values including environmental aspects.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}