FOMC Members Agree on the Need for Base Rate Hike

[Asia Economy Reporter Kwangho Lee] As early as this month, the Bank of Korea is likely to raise the base interest rate, which is expected to deal a heavy blow to companies and households still struggling from COVID-19. In particular, it is anticipated that a wave of bankruptcies among zombie companies (with interest coverage ratios below 100%) that survive on debt will be inevitable. Concerns are also rising that the financial market will face aftershocks as interest pressure intensifies, especially on borrowers who have leveraged all their assets (Yeongkkeul) or invested with borrowed money (Debt Investment).

According to the minutes of the 14th Monetary Policy Committee meeting in 2021, published on the Bank of Korea’s website on the 4th, six out of seven committee members, including Governor Lee Ju-yeol, agreed on the necessity of raising the base interest rate, while one member suggested postponing the decision until after sufficient COVID-19 vaccinations have been administered.

Committee member Ko Seung-beom argued, "We should focus on financial stability concerns such as the collapse of asset price bubbles built on debt investment rather than the real economy, and raise the base interest rate by 0.25 percentage points to 0.75%." Other committee members also agreed on the need to raise rates in the near future.

Concerns Over Wave of Bankruptcies Due to Principal and Interest Repayment Burden on Companies

As the Bank of Korea’s decision to raise the base interest rate becomes more tangible, a megaton-scale aftershock is expected to hit companies and households. With the COVID-19 financial support measures (principal repayment extensions and interest payment deferrals) scheduled to end in September, an increase in the base interest rate will exacerbate the burden of principal and interest repayments, potentially leading to a wave of bankruptcies and financial sector insolvencies.

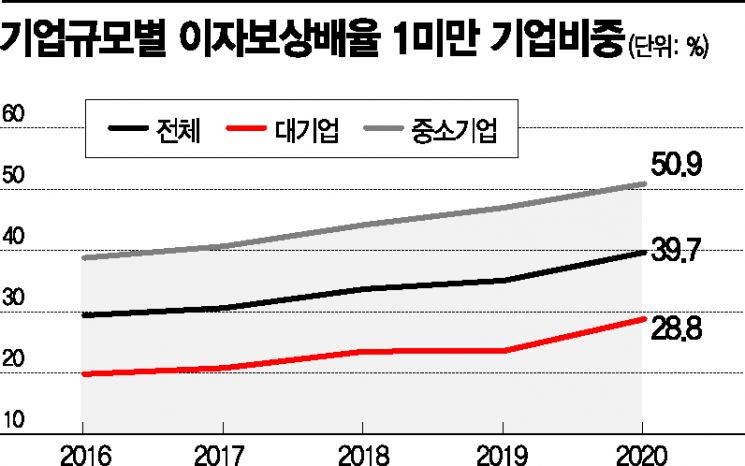

In fact, as loans to small and medium-sized enterprises (SMEs) surge, signs of insolvency become more evident. As of the first quarter of this year, SME loans reached 1,193.4 trillion won, up 16.4% from a year earlier. Among 2,520 companies that disclosed financial statements last year, 39.7% had an interest coverage ratio below 1, up 2.7 percentage points from 37.0% in 2019. This means that 4 out of 10 domestic companies last year were struggling so severely that they could not even cover their interest expenses. The situation for SMEs is particularly severe. During the same period, the interest coverage ratio for SMEs rose from 47.0% to 50.9%, indicating that more than half are unable to cover their interest payments.

Households Worry About Interest Burden from Yeongkkeul and Debt Investment... Income and Consumption Decline

Household debt is also a major concern. As of the first quarter, household debt stood at 1,765 trillion won, up 9.5% from a year earlier. When interest rates rise, increased interest payments reduce income and consumption capacity. Those who borrowed from relatively high-interest sources such as secondary financial institutions and loan companies face even greater burdens. According to data submitted by the Bank of Korea to Kim Young-jin, a member of the Democratic Party, a 0.25 percentage point increase in the base interest rate would raise interest burdens on housing-related loans by 1.4 trillion won, and a 0.5 percentage point increase would raise it by 2.7 trillion won.

Moreover, commercial banks are raising loan interest rates and reducing preferential rates. Last month, the interest rates on unsecured loans at the four major commercial banks?KB Kookmin, Shinhan, Hana, and Woori?ranged from 2.59% to 3.65% per annum, up 0.6 percentage points at the lower end compared to a year ago. Mortgage loan rates have also returned to pre-COVID-19 levels at 2.74%. Most Yeongkkeul and debt investment borrowers are in their 20s and 30s, who generally lack repayment capacity. As of the first quarter, household loans from banks to people in their 20s amounted to 43.6 trillion won, up 33.3% from a year earlier, while loans to those in their 30s reached 216 trillion won, up 18.5%.

The proportion of household loans with variable interest rates at commercial banks is also as high as 81.5%, suggesting that the interest burden on borrowers will increase further when rates rise.

Professor Kim Sang-bong of Hansung University’s Department of Economics said, "A rate hike is expected to deliver a significant shock to companies and households," adding, "Above all, the insolvency of marginal companies is likely to surface, potentially triggering a chain of bankruptcies."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}