If Worried About Income Gaps After Retirement and Want Higher Initial Payments, Choose 'Initial Increase Type'

If Concerned About Future Purchasing Power Due to Inflation, Opt for 'Regular Increase Type' Every 3 Years

Korea Housing Finance C

[Asia Economy Yeongnam Reporting Headquarters Reporter Kim Yong-woo] A new housing pension product that allows subscribers to design their pension receipt method according to their own living conditions is being introduced. Existing fixed-amount subscribers can also switch to the new product.

This enables retirees who are worried about an immediate income gap after retirement or those who are more burdened by future inflation to choose a retirement pension that suits their individual circumstances.

The Housing Finance Corporation (HF) announced on the 28th that it will launch a new product on August 2nd that allows housing pension subscribers to select their pension receipt method based on their economic activities and financial situation to prepare for a more stable retirement life.

The housing pension is a financial product guaranteed by the government that allows individuals to receive a fixed monthly amount like a lifelong pension by providing their home as collateral and obtaining a loan from a financial institution.

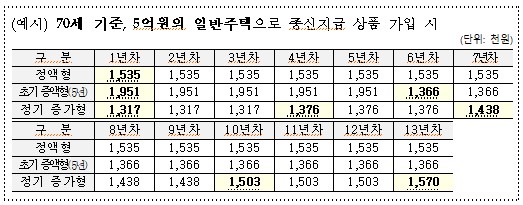

HF Corporation will maintain the popular fixed-amount type while introducing an ‘initial increased type,’ which allows subscribers to choose an initial period of 3, 5, 7, or 10 years during which they receive a higher amount, and a ‘regular increase type,’ which periodically raises the pension amount to compensate for purchasing power decline due to inflation.

The initial increased type provides a higher pension amount than the fixed-amount type for a certain initial period, with the subscriber able to select the increase period from 3, 5, 7, or 10 years according to their situation.

For example, a 60-year-old homeowner with a house valued at 500 million KRW who subscribes to the 5-year initial increased type product will receive about 1,362,000 KRW monthly, approximately 28% more than the fixed-amount type (1,061,000 KRW) for five years.

From the sixth year onward, they will receive a reduced amount at about 70% of the initial receipt (953,000 KRW) for life. The initial increased type is useful when an income gap occurs after retirement until receiving other pensions such as the National Pension, or when elderly subscribers expect additional expenses like medical costs.

The ‘regular increase type’ is a method where the pension amount increases by 4.5% every three years after the initial pension receipt.

A 60-year-old homeowner with a house valued at 500 million KRW who subscribes to this type will start with a lower initial amount of 878,000 KRW compared to the fixed-amount type (1,061,000 KRW), but from age 75, they will receive 1,094,000 KRW, which is higher than the fixed-amount type, and at age 90, they can receive 1,363,000 KRW.

Therefore, the regular increase type is useful for those concerned about purchasing power decline due to inflation after subscribing to the housing pension or who want to prepare for increased living expenses such as medical costs.

President Choi Jun-woo said, “The launch of two new types of housing pensions has expanded subscribers’ choices,” and added, “We will continue to listen to the public and improve the system.”

An HF Corporation official stated, “There is no difference in the pension loan limit by payment type, and the monthly amount varies according to the pension receipt schedule, so it is important to accurately understand one’s economic situation when making a choice.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}