Bank of Korea 'Financial Institutions Loan Behavior Survey Results'

[Asia Economy Reporter Eunbyeol Kim] Concerns over the rapidly increasing household debt continue, and with regulatory authorities tightening supervision, it is expected to become more difficult to obtain household loans from banks in the third quarter of this year.

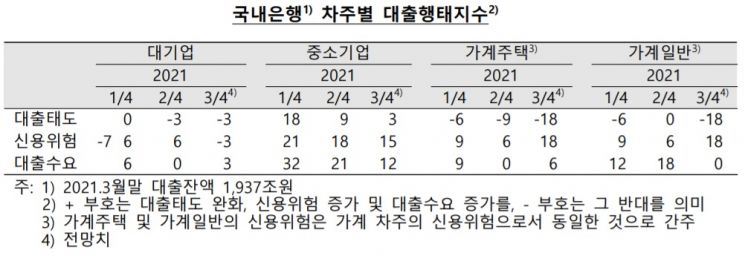

According to the "Financial Institution Lending Behavior Survey Results" announced by the Bank of Korea on the 12th, lending attitudes of domestic banks are expected to tighten mainly for household loans in the third quarter of this year. The comprehensive lending attitude index of domestic banks is projected to be -3 (forecast) in the third quarter, indicating a tightening compared to 7 in the second quarter. By borrower type, large corporations recorded -3, small and medium enterprises (SMEs) 3, household mortgage loans and general household loans each recorded -18.

The Lending Behavior Survey is a questionnaire survey conducted among credit officers of domestic financial institutions. A plus (+) indicates easing of lending attitudes, increased credit risk, or increased loan demand, while a minus (-) indicates the opposite. A strengthened lending attitude means that loan screening will become stricter than before.

Notably, lending attitudes for household mortgage and general household loans have significantly tightened by borrower type. The household mortgage lending attitude index, which tightened to -9 in the second quarter, is expected to tighten sharply to -18 in the third quarter. The general household lending attitude index is also expected to tighten from 0 to -18 during the same period.

A Bank of Korea official stated, "Lending attitudes toward households are expected to tighten significantly compared to the previous quarter for both household mortgage and general household loans due to the increased need for credit risk management and strengthened household loan regulations." Regulatory authorities announced the "Household Debt Management Plan" at the end of April, which includes expanded application of the Debt Service Ratio (DSR) on a borrower basis and strengthened Loan-to-Value (LTV) regulations on non-housing collateral loans.

For SMEs, the easing degree is expected to weaken as financial support measures for small business owners and small corporations come to an end. The SME lending attitude index dropped from 9 to 3.

The credit risk index by borrower type was evaluated as -3 for large corporations, 15 for SMEs, and 18 for households. The comprehensive credit risk index, weighted by loan amounts of corporations and households, rose to 18, up from 10 in the second quarter.

The Bank of Korea stated, "During the third quarter, corporate credit risk is expected to decrease for large corporations but continue to increase for SMEs." This is because large corporations’ profitability improves due to export increases amid global economic recovery, reducing credit risk, while SMEs continue to be affected by COVID-19. Regarding household credit risk, it was noted, "Concerns over delayed income improvement among vulnerable borrowers and the possibility of increased debt repayment burdens due to rising loan interest rates are expected to raise credit risk compared to the previous quarter."

During the third quarter, corporate loan demand is expected to increase for both large corporations and SMEs as the impact of COVID-19 persists. Household loan demand is expected to slightly increase for housing funds due to the continued rise in housing and jeonse prices, but demand for general funds is projected to remain flat as the increase is significantly restrained by strengthened DSR regulations.

Lending attitudes of non-bank financial institutions are also expected to tighten across all sectors. Lending attitude indices are expected to strengthen for mutual savings banks (-12), credit card companies (-13), mutual finance cooperatives (-22), and life insurance (-5). The Bank of Korea stated, "Lending attitudes are expected to tighten due to regulatory authorities’ lending regulations and credit soundness management."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}