Tug of War Over Fee Setting and Rates

Attention on Joint Banking Sector Platform 추진도

[Asia Economy Reporter Kiho Sung] As the government-led refinancing loan (loan switching) platform is about to launch, banks and fintech companies are actively negotiating over fees. There is a significant disagreement between the two sides regarding the fee imposition method and calculation, making it difficult to resolve the conflict.

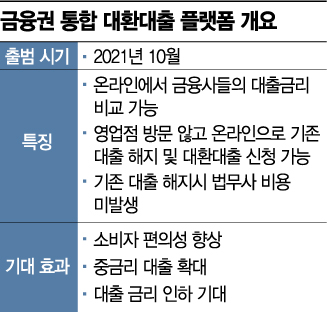

According to the financial sector on the 28th, the government is accelerating the establishment of a ‘loan switching system’ in October, coinciding with the upcoming reduction of the legal maximum interest rate (from 24% to 20% per annum) next month and the launch of the MyData (personal credit information management) service in August. This system will connect the payment network of the Korea Financial Telecommunications & Clearings Institute, which is commonly used by financial companies, and provide the service to individuals. However, the service launch is expected to face challenges due to significant differences in opinions on fee setting among participating parties.

The government’s goal is to make it easy to switch “all household loans.” Therefore, if fees involved in refinancing loans can be reduced, the saved resources can be poured into lowering loan interest rates. If competitiveness in loan interest rates is achieved, it becomes easier to gain leadership in the loan market where all financial companies participate.

Financial companies providing loans are demanding information usage fees from fintech firms. While the actual loan and customer information provision are handled by financial companies, fintech firms receive intermediary fees from refinancing loans. On the other hand, fintech companies argue that “the owner of customer information is the customer” and that “it is not appropriate for financial companies to charge fees based on customer information.”

Opinions also differ on the effect of lowering interest rates through information usage fees. Financial companies believe that reducing intermediary fees can lead to lower interest rates. Fintech firms oppose this view, arguing that if information usage fees are imposed, the costs will naturally be passed on to customers, undermining the original intent of interest rate reduction through active refinancing loans.

The fee rate between financial companies and the platform providers facilitating loan switching is also a contentious issue. Frequent loan transfers could increase the intermediary fees for platform providers. Currently, a proposal to set the fee at less than half of the existing rate (1.6?2.0% of the loan amount) is being seriously considered. Prepayment penalties are also a major topic of discussion. If financial companies set high prepayment penalty rates, switching loans itself becomes difficult. There are opinions that prepayment penalty rates should be set at an appropriate level to activate the service.

Recently, the ‘joint platform by banks’ initiative promoted by the banking sector has also sparked controversy. Commercial banks, fearing dependence on fintech once the refinancing loan platform launches, have submitted their review opinions on ‘joint operation of the platform by banks’ to financial authorities.

A financial sector official said, “If the refinancing loan service becomes active, even a 0.01% fee rate will amount to a large sum,” adding, “Therefore, even the smallest details are bound to be highly sensitive.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}